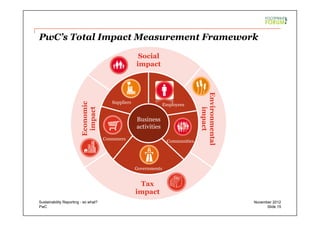

This document summarizes a presentation about sustainability reporting. It discusses why businesses should engage in sustainability reporting to protect and enhance value. Total impact reporting was presented as going beyond traditional reporting to measure environmental, social and economic impacts. Examples were given of companies like Puma and British Land conducting environmental profit and loss accounting and assessing wider socioeconomic impacts. The document emphasizes moving towards reporting on impacts and outcomes over outputs.