Downloaded 19 times

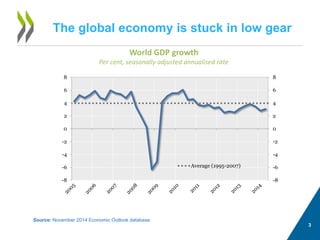

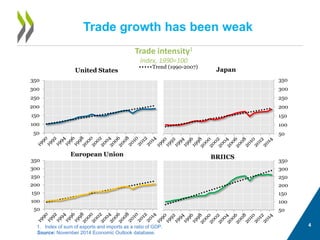

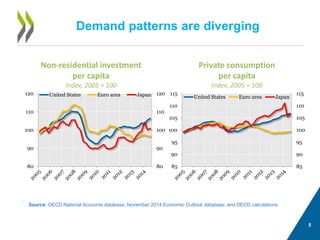

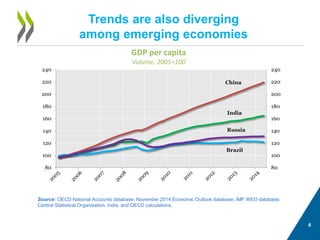

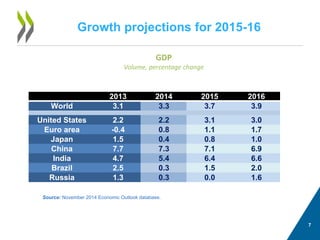

The document summarizes the OECD Economic Outlook report. It finds that: 1) The global economy is growing slowly, with world GDP growth below historical averages and weak trade growth. 2) Growth projections vary across countries, with the US expected to accelerate but remain below trend, while China and India are projected to experience slower growth than in recent years. 3) Risks to the outlook are on the downside and include high debt levels in advanced economies and potential slowing of potential growth rates.