Download to read offline

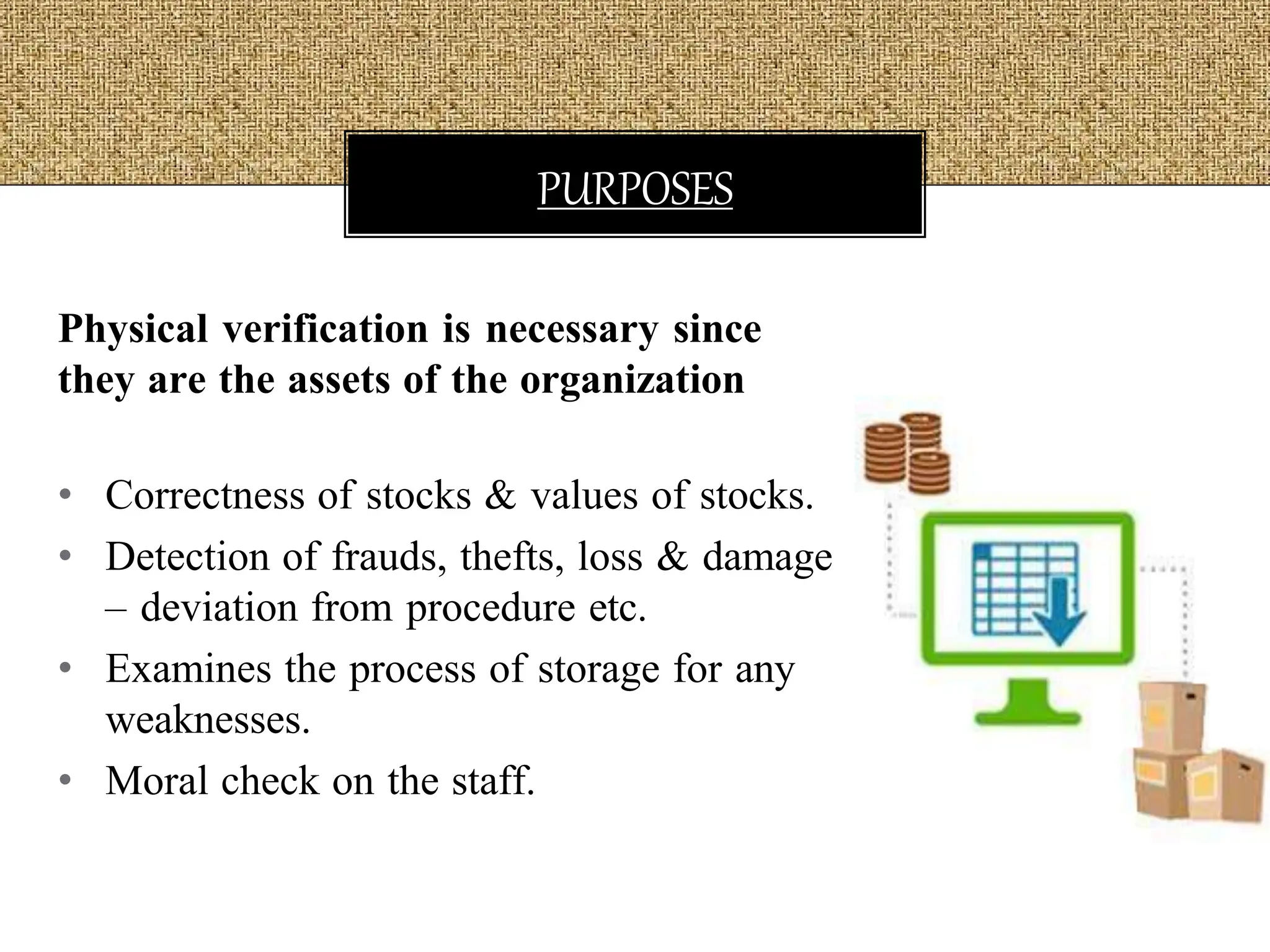

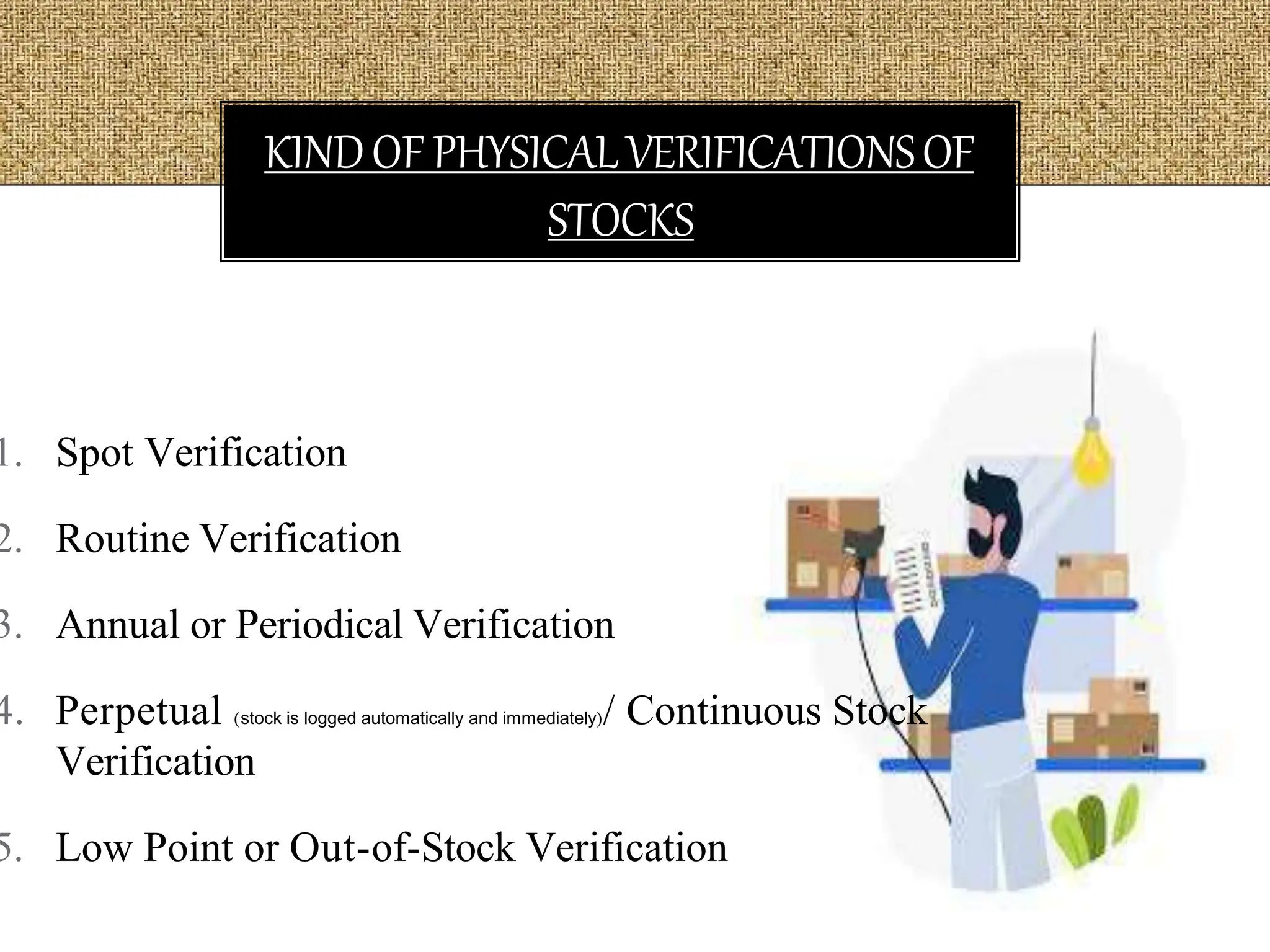

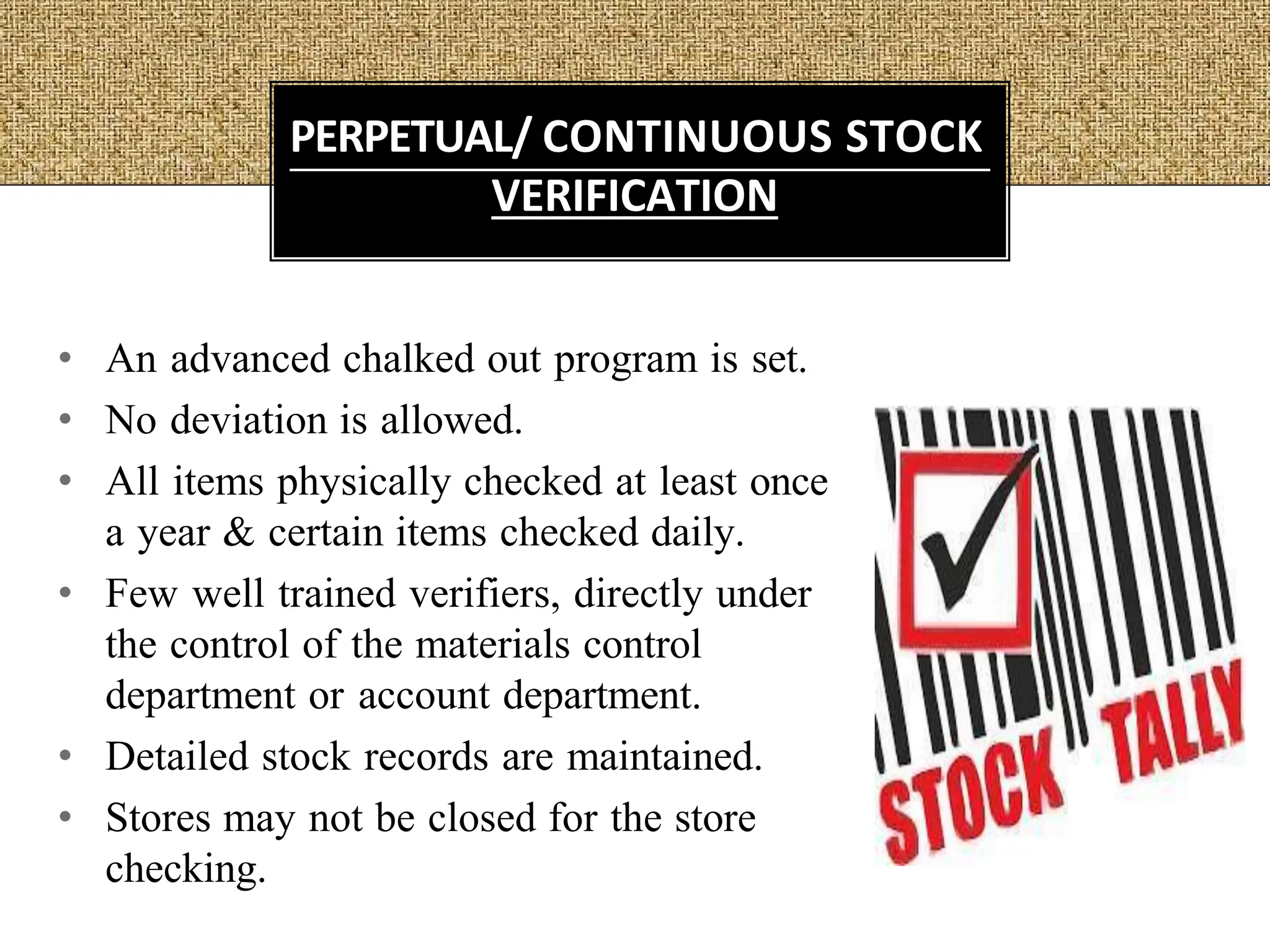

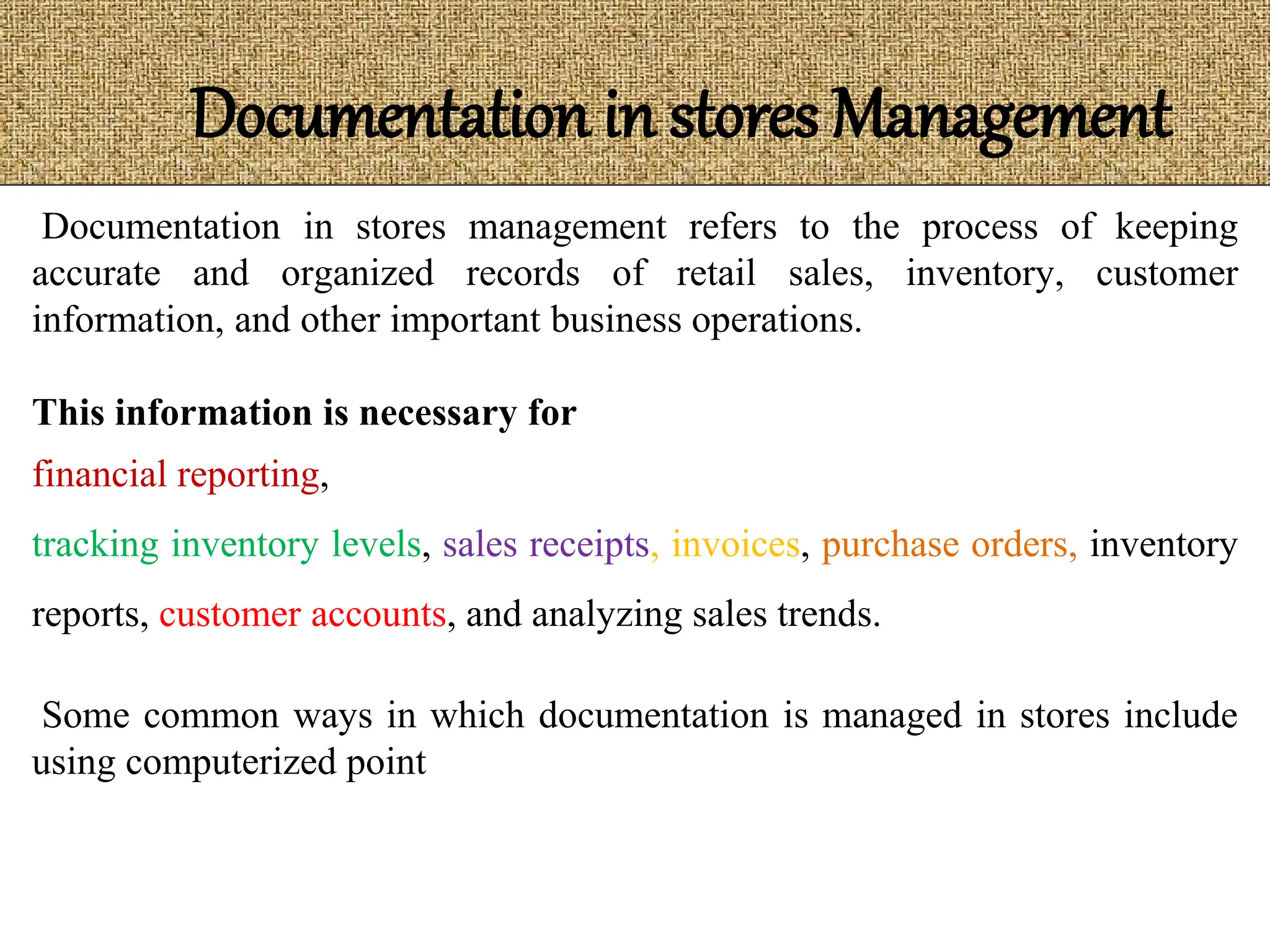

Stores management refers to overseeing the daily operations of retail businesses, including inventory management, staff management, financial management, and customer service. Effective stores management systems and procedures can help stores optimize operations, improve efficiency and accuracy, and increase profits. Key aspects of stores management systems include periodic physical inventory counts to verify stock levels, tracking different types of material losses, properly disposing of surplus inventory, and maintaining comprehensive documentation of business operations and data.