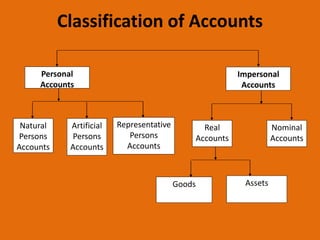

The document outlines three types of accounts in accounting - personal, real, and nominal accounts - and provides rules for debiting and crediting transactions to each. Personal accounts debit the receiver and credit the giver. Real accounts debit assets entering the business and credit assets leaving. Nominal accounts debit expenses and losses, and credit incomes and profits. The document also includes a classification of different types of accounts and contact information.