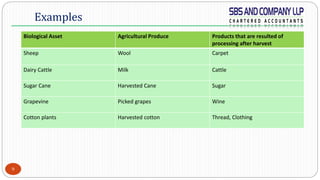

This document provides an overview of IND AS 41 - Agriculture. It discusses the objective, scope, key definitions, recognition, measurement and disclosure requirements of the standard. The standard relates to accounting for agricultural activity, including biological assets and agricultural produce. It requires biological assets and agricultural produce to be measured at fair value less costs to sell, except when fair value cannot be measured reliably. The document provides examples of biological assets and the resulting agricultural produce, and outlines the recognition criteria and disclosures required by the standard.