Download to read offline

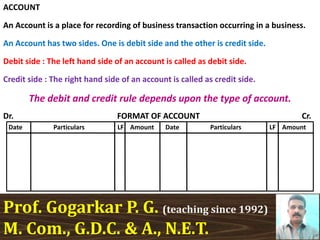

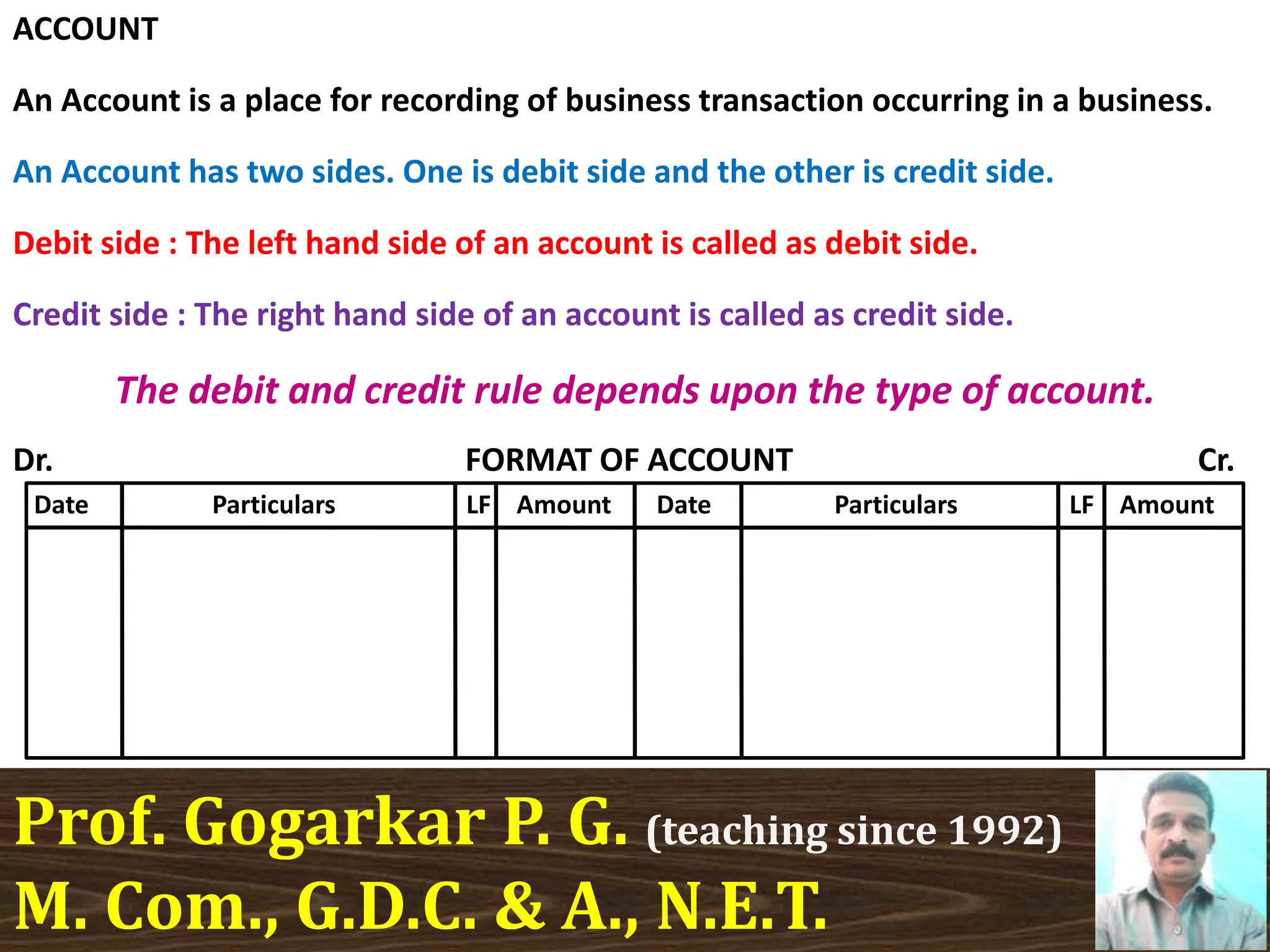

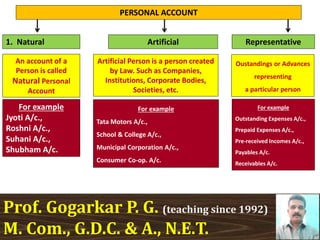

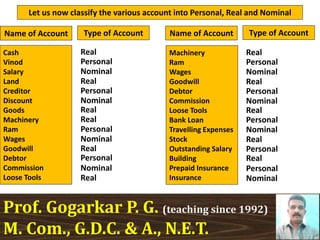

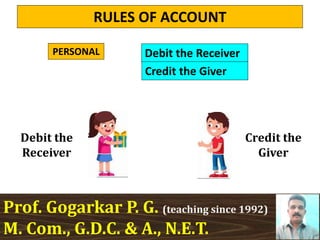

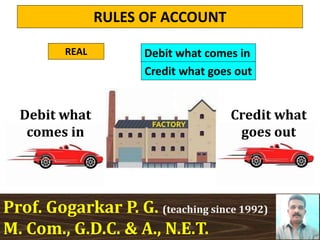

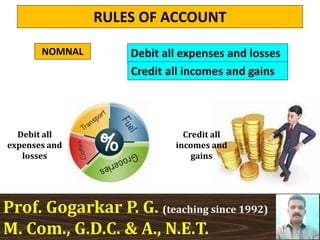

An account is used to record business transactions and has two sides: a debit side and a credit side. The type of account, whether personal, real, or nominal, determines which side a transaction is recorded on based on set rules. Personal accounts follow the rule that the receiver of an item or money is debited and the giver is credited. Real accounts debit what comes in and credit what goes out. Nominal accounts debit expenses and losses and credit incomes and gains.