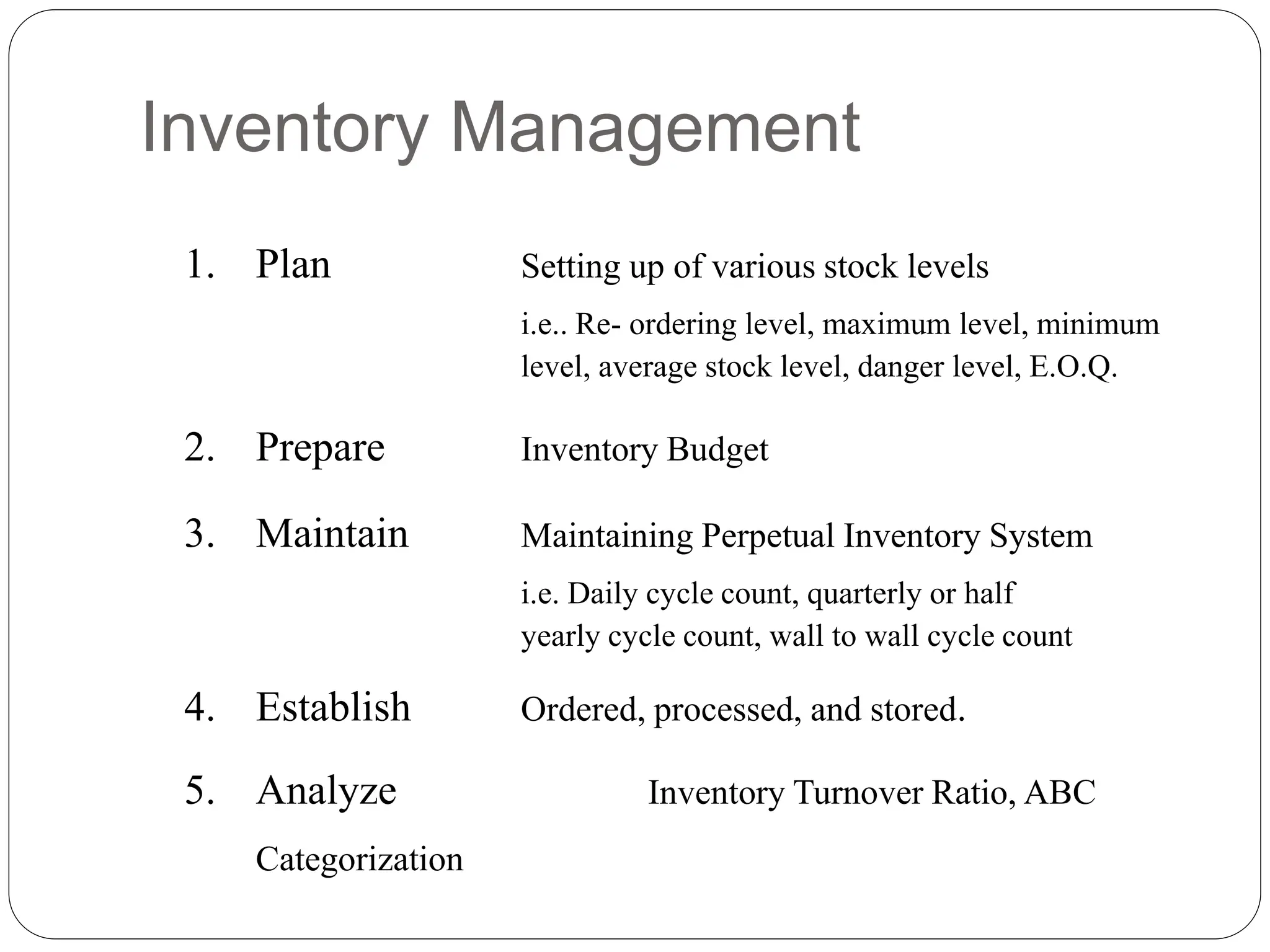

The document discusses inventory management and control techniques. It covers topics like setting stock levels, inventory budgeting, perpetual inventory systems, ABC analysis, economic order quantity (EOQ) modeling, and quantity discounts. ABC analysis involves categorizing inventory items into A, B, and C categories based on their value and accounting for 80%, 15-20%, and 5-10% of total spending, respectively. EOQ modeling determines the optimal order quantity to minimize total inventory costs based on factors like demand, ordering costs, and holding costs. Quantity discounts provide pricing incentives for purchasing higher volumes.

![Application of EOQ

Current Policy EOQ Policy

Q = 200 Units EOQ = 97 Units

T.C = [Annual H.C] + [Annual S.C] T.C = [Annual H.C] + [Annual S.C]

T.C = [Avg. Cycle Inv. X Unit Holding Cost] + [No. Orders / Yr x Ordering Cost]

T.C = (200/2)(20) + (3,120/200)(30) T.C = (97/2)(20) + (3,120/97)(30)

T.C = 2000 + 468 T.C = 970 + 965

T.C = $2468 T.C = $1,935

What is the total annual cost of the current policy (Q = 200), and

how does it compare with the cost by using the EOQ?](https://image.slidesharecdn.com/topic4inventorymanagementmodel-231026053403-bcd284b2/75/Topic-4-Inventory-Management-Model-pptx-17-2048.jpg)

![Quantity Discounts Models

1. All units quantity discount

e.g. X amount of discount offer, if order quantity per annum > 2000

2. Incremental units quantity discount. Following is an example;

Total Annual Cost:

Quantity Discount Unit Price

1-999 units 0% $5.00

1000-1999 units 4% $4.80

2000 or more units 5% $4.75

TC = [ (Q/2) x H ] + [ (D/Q) x S ] + [ P x D ]

ANNUAL CARRYING COST ANNUAL ORDERING COST ANNUAL FIXED COST](https://image.slidesharecdn.com/topic4inventorymanagementmodel-231026053403-bcd284b2/75/Topic-4-Inventory-Management-Model-pptx-20-2048.jpg)

![Total Cost:

Example (Cont.)

TC2 = [ (EOQ2/2) x H ] + [ (D/EOQ2) x S ] + [ P x D ]

TC2 = [ (1000/2) x 0.96] + [ (5000/1000) x 49] + [4.80 x 5000]

TC2 = $480 + $245 + $24,000 = $24,725

TC1 = [ (EOQ1/2) x H ] + [ (D/EOQ1) x S ] + [ P x D ]

TC1 = [ (700/2) x 1] + [ (5000/700) x 49 ] + [ 5 x 5000 ]

TC1 = $350 + $350 + $25,000 = $25,700

TC3 = [ (EOQ3/2) x H ] + [ (D/EOQ3) x S ] + [ P x D ]

TC3 = [ (2000/2) x 0.95] + [ (5000/2000) x 49] + [4.75 x 5000]

TC3 = $950 + $122.50 + $23,750 = $24,822.50

TC = [ (Q/2) x H ] + [ (D/Q) x S ] + [ P x D ]](https://image.slidesharecdn.com/topic4inventorymanagementmodel-231026053403-bcd284b2/75/Topic-4-Inventory-Management-Model-pptx-23-2048.jpg)