Download to read offline

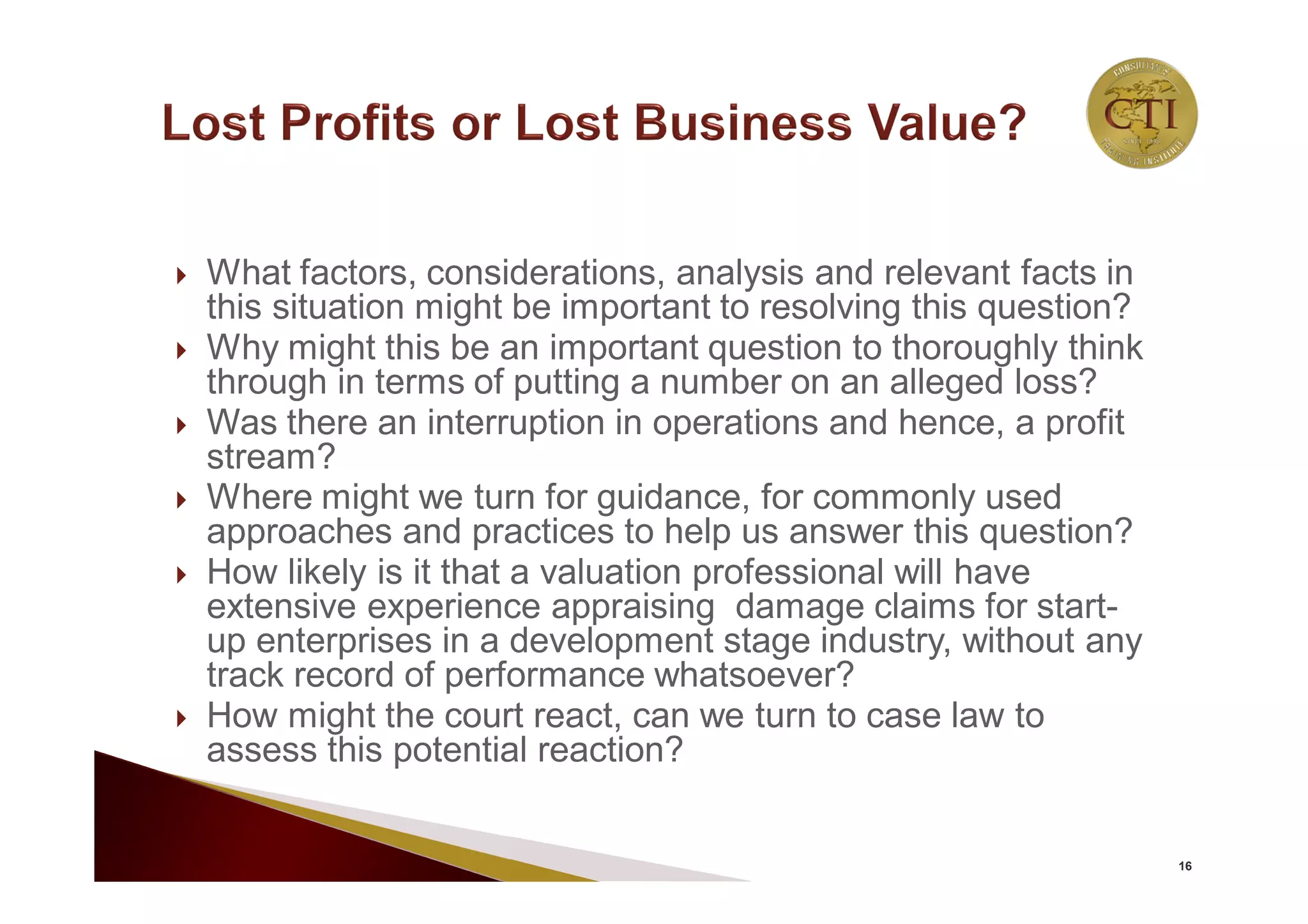

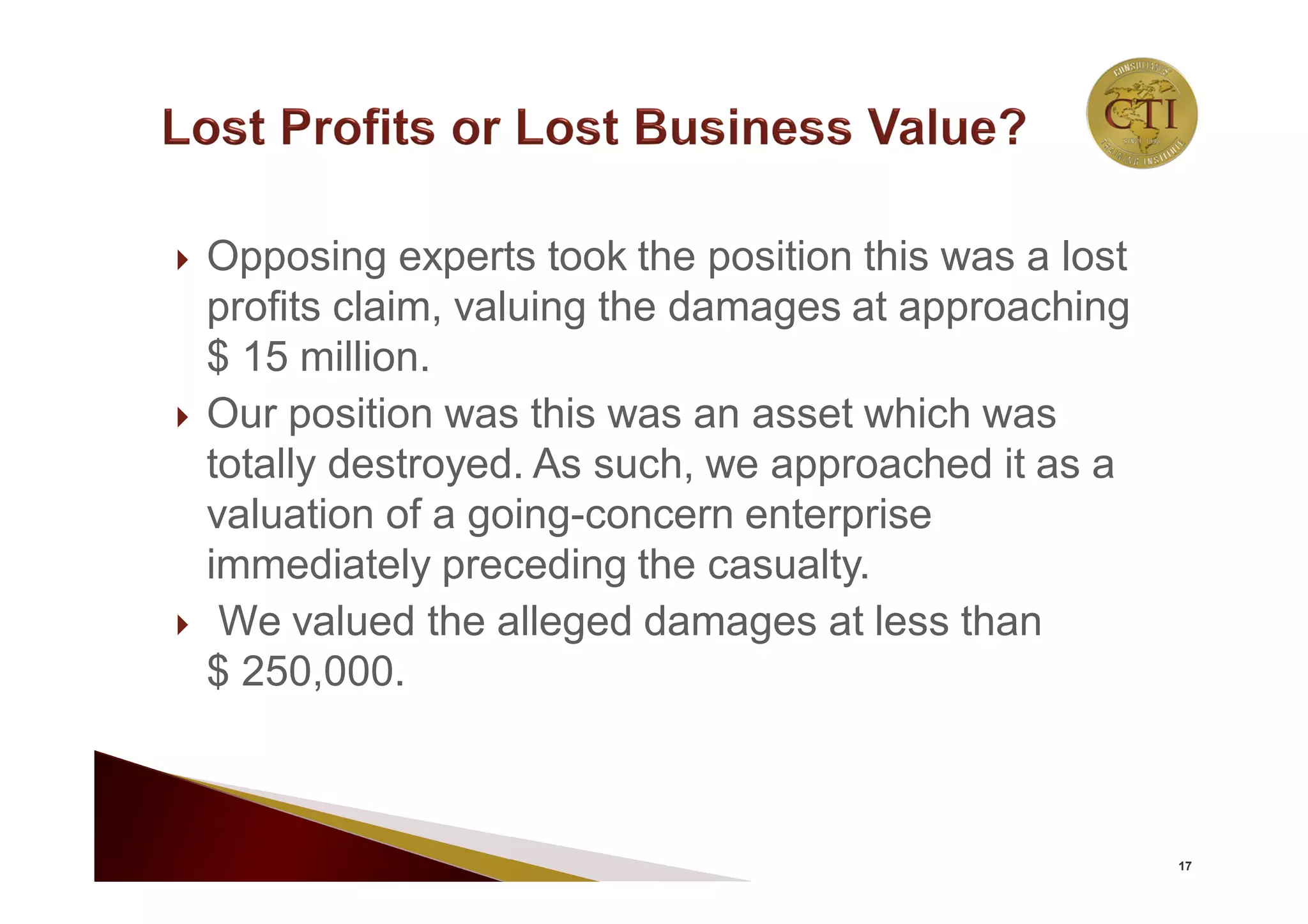

![ In Chapter 13 of the BVR Guide, it states that, “…[I]f a business is

completely destroyed, [then] the proper total measure of damages is

the market value of the business on the date of the loss”.

In some matters, because the loss of future profits extends into

perpetuity, the courts have found that loss of business value is the

proper measure of the loss.

When an entire business is destroyed, the financial expert’s task

remains to determine the business’s lost future cash flow, but the

earnings or cash flows are lost in perpetuity, rather than for a finite

period.

25](https://image.slidesharecdn.com/65318c23-ee6a-4d7e-9dc2-8acba0808626-161209195152/75/T-Wayne-Valuing-a-Dream-Working-File-25-2048.jpg)

This document contains a disclaimer for information presented about valuing lost profits for a start-up company. It notes that the information is intended for general purposes only and should not be considered legal, accounting, or professional advice. It also states that the authors disclaim any liability for loss or risk resulting from the use of the information provided. The material may not be applicable to all circumstances and readers should consult qualified professionals for their specific needs.