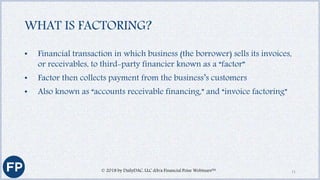

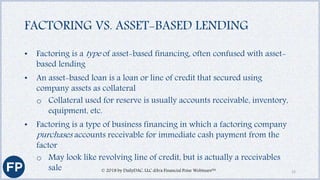

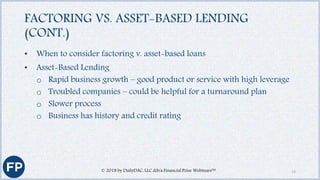

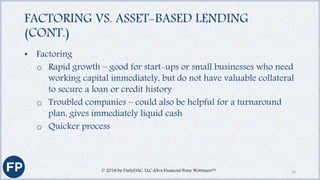

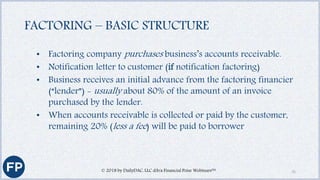

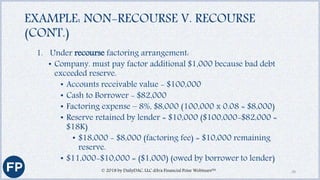

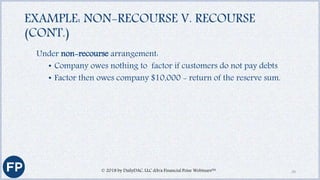

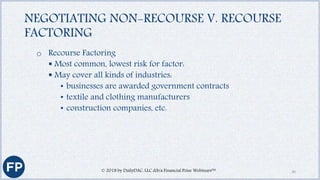

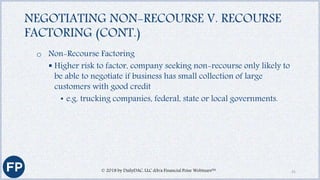

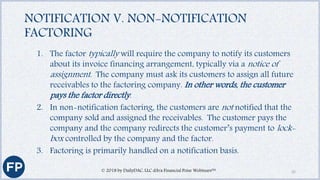

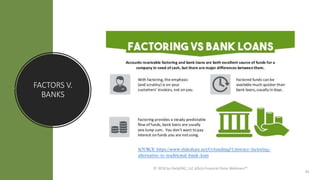

The document discusses the New York Institute of Credit's educational offerings for various professionals and outlines a webinar series focused on factoring and business financing options. It explains the process of factoring, contrasting it with asset-based lending, and describes benefits and challenges of both approaches. The series aims to provide accessible information for business owners, investors, and professionals through engaging discussions.