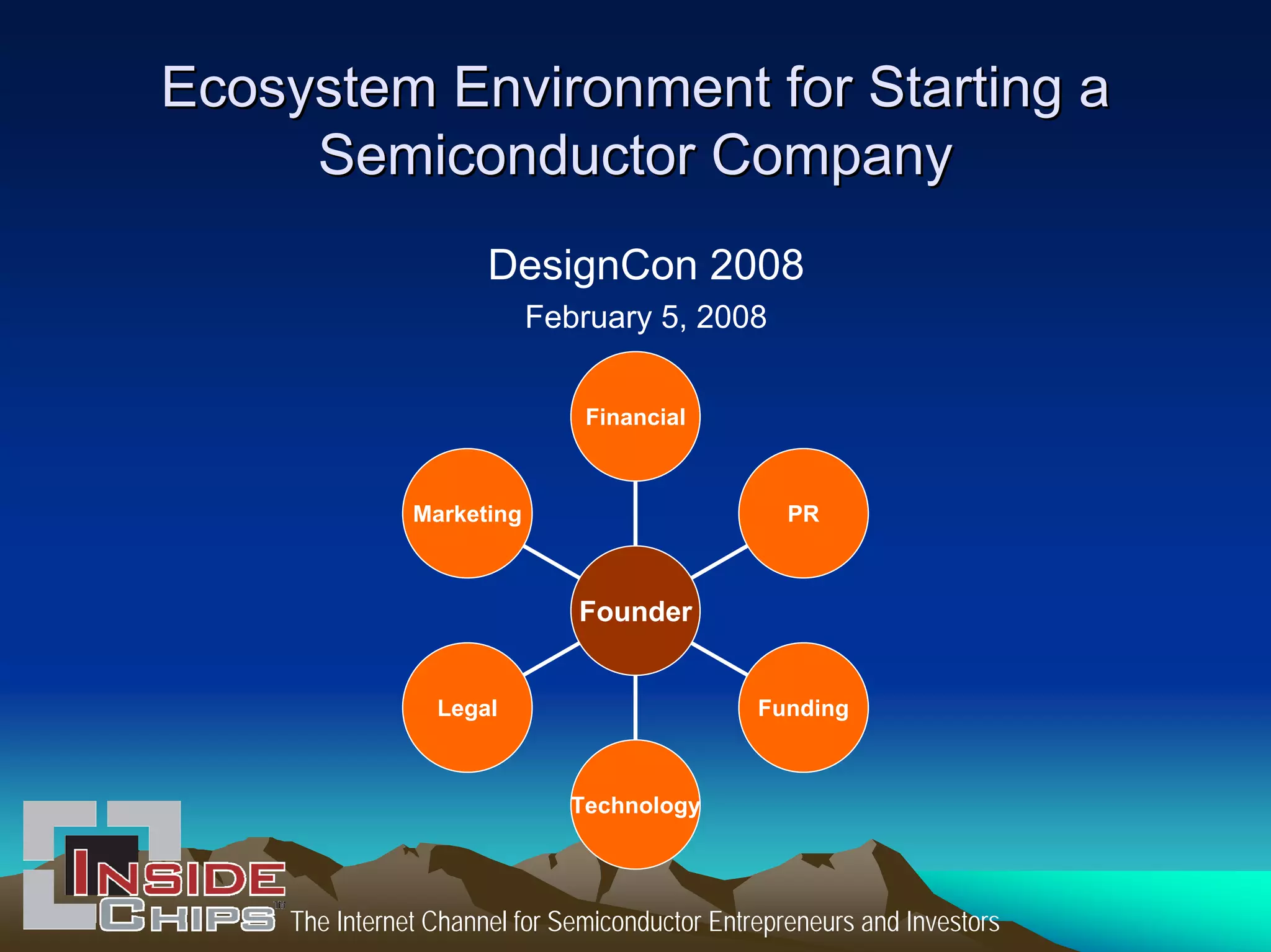

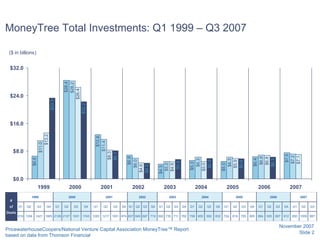

The document outlines the essential components of an ecosystem for launching a semiconductor company, including legal, technology, marketing, financial, and public relations aspects. It emphasizes the importance of founder experience, careful equity management, and the need for experienced advisors. Additionally, it highlights potential pitfalls and considerations for startups, such as IP ownership and sales strategies, supported by statistical insights on venture capital investments in the semiconductor industry.