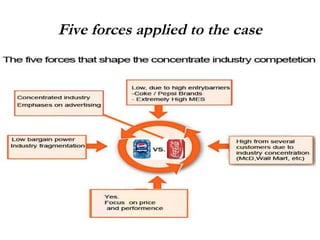

The document analyzes the soft drink concentrate producers industry and bottlers industry using Porter's five forces framework. It finds that the concentrate producers industry experiences high profitability due to industry concentration among Coke and Pepsi, strong brand awareness and identity, and low threat of substitutes. In contrast, the bottlers industry has high fragmentation, price wars due to customer bargaining power, and extremely low profitability. Overall, the concentrate producers industry is seen as more attractive due to the extreme differences in profitability and higher entry barriers compared to the bottlers industry.