Source of fianace

•Download as PPSX, PDF•

3 likes•4,153 views

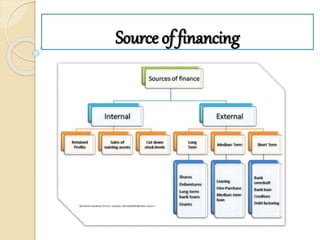

Equity shares represent ownership in a company and are an important source of long-term capital financing. Preference shares have preferential rights to dividends and assets but limited voting rights. Debentures are a form of debt where the company promises to repay the principal along with interest. Other sources of financing discussed include retained earnings, loans from banks and financial institutions, public deposits, trade credit, leasing, factoring, and commercial paper.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Source of fianace

Similar to Source of fianace (20)

More from Karthik Bharadwaj

More from Karthik Bharadwaj (20)

Recently uploaded

Recently uploaded (20)

Source of fianace

- 3. EQUITY SHARES Meaning : Equity shares is the most important sources of raising long term capital by company.Equity shares represent the ownership of company and thus the capital raised by issue of such shares is known as ownership capital or owner’s fund. Equity shares capital is a perquisites to the creation of the company.

- 4. Equity Shares: Equity share holders do not get fixed dividend but are the paid on the basis of earnings of the company. They are referred to as “residual owners” since they receive what is left after all other claims on the company’s income and assets have been settled. They enjoy the reward as well as bear the risk ownership.

- 5. Equity Shares: Their liability, however is limited to the extent of capital contributed by the company. Further through their right to vote these share holders have right to participate in the management of the company

- 6. MERITS Equity shares are suitable for investors who are willing to assume risk for higher returns Payment of the dividend to the equity share holders is not compulsory Equity capital provides credit worthiness to the company and confidence to the prospective loan providers.

- 7. Limitations Investors who want steady income may not prefer equity shares as equity shares get fluctuating returns The cost of equity shares is generally more as compared to the cost of raising funds through other sources.

- 8. Retained Earnings Retained earnings refer to the percentage of net earnings not paid to out as dividends, but retained by the company to be reinvested in its core business or to pay debt. It is recorded under shareholders’ equity on the balance sheet.

- 9. PREFRENCE SHARES Preference shares are those which have preferential right to the payment of dividend during the life-time of the company and a preferential right to the return of capital when the company is wound up.

- 10. TYPES OF PREFERENCE SHARES Cumulative and Non cumulative. Participating and Non Participating. Convertible and Non Convertible. Redeemable and Non Redeemable

- 11. CUMULATIVE AND NON- CUMULATIVE Holders of Cumulative preference shares are entitled to recover the arrears of preference dividend before any dividend is paid on equity shares. In the case of Non- cumulative Preference shares arrears of dividend do not accumulate and hence, if dividend is to be paid to equity shareholder in any year, dividend at a fixed rate for only 1 year will have to be paid to preference shareholder before equity dividend is paid.

- 12. Participating and Non- Participating Participating Preference shareholders are not only entitle to only fixed rate of dividend but have the right to receive any surplus profit which remains after dividend has been paid at a certain rate to equity shareholders. Non-Participating Preference shareholders are entitle to only fixed rate of dividend.

- 13. Convertible and Non- Convertible Holder of Convertible Preference shares enjoy the right to get preference share converted into equity shares according to the terms of issue. Holder of Non Convertible Preference shares do not enjoy any such right.

- 14. Redeemable and Non- Redeemable Redeemable Preference shares are those preference shares whose amount can be returned by the company to their holder within the life time of the company subject to the terms of the issue and fulfillment of certain legal conditions laid down in sec 80 of the companies act. The amount of Non Redeemable Preference shares can be returned only company is wound up.

- 15. BENEFITS Helpful in raising long-term capital for a company. Have first claim on profits and proceeds from the sale of the company’s asset at the time of bankruptcy. Have fixed rate of dividend for fixed number of years. Guaranteed Rate of Return.

- 16. DRAWBACKS Not traded in market like ordinary shares. Not available to retail investors. Not advantageous to investors form the point of view of control & management as preference share do not carry voting rights. Cost of raising preference share capital is higher.

- 17. DEBENTURES “An honest man’s word is as good as his debenture bond”- Miguel

- 18. Debentures are an important instrument for raising long term debt capital. The debenture issued by an company is an acknowledgement that the company has borrowed a certain amount of money, which it promises to repay at a future date. Debenture holders are therefore termed as “Creditors” of the company.

- 19. TYPES OF DEBENTURES On the basis of security:- a. Secured Debentures. b. Unsecured Debentures. Secured Debentures are such which create a charge on the assets of the company, thereby mortgaging the assets of the company. Unsecured Debentures do not carry any charge on the assets of the company.

- 20. On the basis of redemption:- a) Redeemable Debentures. b) Non-redeemable Debentures. These are the debentures which are issued for a fixed period. It can be redeemed by annual drawings or by purchasing from the open market. These are the debentures which are not redeemed in the life time of the company. Such debentures are paid back only when the company goes to liquidation.

- 21. On the basis of records:- a) Registered Debentures. b) Bearer Debentures. Registered debentures are those which are duly recorded in the register of debenture holders maintained by the company. The debentures which are transferable by mere delivery are called bearer debentures.

- 22. On the basis of Convertibility:- a) Convertible Debentures. b) Non-Convertible Debentures. Convertible debentures are those debentures that can be converted into equity shares after the expiry of a specified period. Non- Convertible debentures are those which cannot be converted into equity shares.

- 23. Advantages When the company issues debentures it does not result in the dilution of Ownership as is the case with the issue of equity shares. Interest paid on a debenture is a tax deductible expense and hence company gets the tax benefit. Since debenture holders do not have any voting rights they do not interfere with the working of the organization. Debenture holders payment of interest is fixed and hence firm does not need to share profits with them.

- 24. DISADVANTAGES Payment of interest on debenture is mandatory and when company is making low profits. Nonpayment of interest can even lead to bankruptcy for the firm. Since on maturity they have to be repaid company needs to plan properly and keep funds for same. If company has not maintained enough funds it is a recipe for a disaster. Debentures are bought by large institutional investors and hence at times it may prove to be costly and difficult source of finance for the company.

- 25. Loan from financial institution and loan from bank Meaning : In finance and economics, a financial institution provide financial services for its clients or members. One of the most important financial services provided by financial institution is acting as a financial intermediaries most financial institution regulated by the government

- 26. Functions Financial institution provide service as intermediaries of financial market. majorly they are three types of financial institution 1) Depository institution 2) Contractual institution 3) Investment institution

- 27. 1) Depository institution; Deposit taking institution that and accept and manage deposit and make loans . 2) contractual institution – insurance companies and pension funds etc .. 3) investment institution - investment banks, underwriter , brokerage firm

- 28. Public deposits Public deposits refers to the unsecured deposits invited by companies from the public mainly to finance working capital needs. A company wishing to invite public deposits makes an advertisement in the newspapers. Any member of the public can fill up the prescribed from and deposit the money with the company. The company in return issues a deposit receipt.

- 29. Lease financing Lease financing is one of the important sources of medium - and long-term financing where the owner of an asset gives another person, the right to use that asset against periodical payments. The owner of the asset is known as lessor and the user is called lessee. The periodical payment made by the lessee to the lessor is known as lease rental. Under lease financing, lessee is given the right to use the asset but the ownership lies with the lessor and at the end of the lease contract, the asset is returned to the lessor or an option is given to the lessee either to purchase the asset or to renew the lease agreement.

- 30. What is a trade credit A trade credit is an agreement where a customer can purchase goods on account (without paying cash), paying the suppliers at a later date. Usually when the goods delivered, a trade credit given for a specific number of days -30, 60 or 90. jewelry businesses sometimes extend credit to 180 days or longer. Trade credit is essentially a credit a company gives to another for purchases of goods & services

- 31. Meaning of trade credit Trade credit is an important external source of working capital financing. It is a short term credit extended by suppliers of goods & services in the normal course of business, to a buyer in order to enhance sales. Trade credit arises when a supplier of goods & services allows customers to pay for goods and services at a later date. Cash is not immediately paid & deferral of payment represents a source

- 32. Advantages of trade credit It is easy and automatic sources of short term finance. It reduces the capital requirement. It helps the business focus on core activities. It does not require any negotiation or formal agreement

- 33. Factoring Factoring is a transaction in which a business sells its accounts receivable, or invoices, to a third party commercial financial company, also known as a “factor.” This is done so that the business can receive cash more quickly than it would by waiting 30 to 60 days for a customer payment. Factoring is sometimes called “accounts receivable financing.”

- 34. Factoring in Five Simple Steps 1.You perform a service for your customer. 2.You send your invoice to a factoring company. 3.You receive a cash advance on your invoice from the factoring company. 4.The factoring company collects full payment from your customer. 5.The factoring company pays you the rest of your invoice amount, minus a fee.

- 35. Some other major benefits include: 1.Factoring can be customized and managed so that it provides necessary capital when your company needs it. 2.The financing does not show up on your balance sheet as debt. 3.Factoring is based on the quality of your customers’ credit, not your own credit or business history. 4.Unlike a conventional loan, factoring has no limit to the amount of financing. 5.Factoring aligns well with start-up businesses that need immediate cash flow.

- 36. Here’s a fictional example to illustrate a common factoring situation: ABC Transport is a trucking company that wants to double the size of its fleet over the next two years and serve more clients in the West. The company has just landed a new customer on the West Coast who needs freight shipped from Kansas City to Los Angeles. The customer will pay for the service within 30 days, but that won’t cover the immediate fuel, payroll and maintenance costs of running the route. The owners of ABC Transport have been in this situation before. They feel that the lack of available cash flow has prevented the company from taking on new business. ABC Transport turns to a factoring company, selling the West Coast customer’s invoice in exchange for a 90% advance on the total amount within a day. The influx of cash replenishes the trucking company’s reserves, allowing it to run the Kansas City-Los Angeles route. Factoring also gives ABC Transport the flexibility to take on new customers as well.

- 37. Banks A financial institution that is licensed to deal with money and its substitutes by accepting time and demand deposits, making loans, and investing in securities. The bank generates profits from the difference in the interest rates charged and paid. TYPES OF BANKS Retail Banks Retail banks provide basic banking services to individual consumers Commercial banks Commercial Banks provide financial services to businesses, including credit and debit cards, bank accounts, deposits and loans, and secured and unsecured loans.

- 38. Cooperative banks Cooperative Banks are governed by the provisions of State Cooperative Societies Act and meant essentially for providing cheap credit to their members Investment Banks Investment banks aid companies in acquiring funds and they provide advice for a wide range of transactions Central banks Central banks provide monetary and financial policy

- 39. Commercial paper A short term unsecured negotiable instrument consisting of promissory notes With fixed maturity Generally they are issued by companies as a means of raising short term debt Issued at a discounted face value The issues promises a fixed amount at future date but pledges no assets