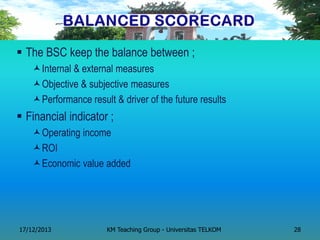

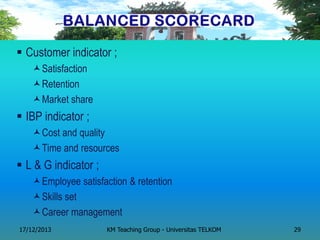

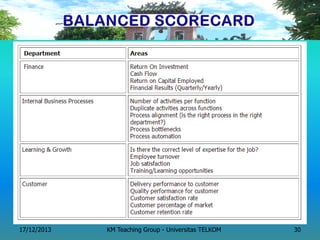

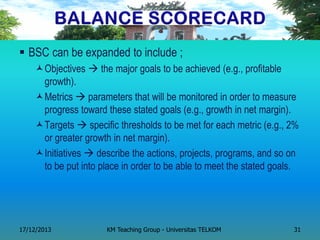

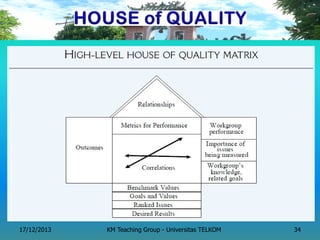

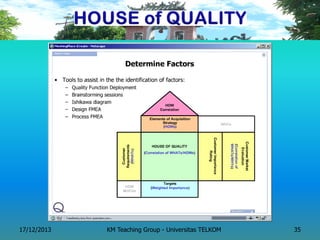

The document discusses various methods for measuring knowledge management (KM), including benchmarking, the balanced scorecard, and the house of quality. It describes benchmarking as comparing an organization's KM processes to those of industry leaders to identify best practices. The balanced scorecard is presented as a framework that translates an organization's strategy into performance indicators across four dimensions: financial, customer, internal processes, and learning and growth. The house of quality is described as a tool to show connections between customer requirements, product/service quality characteristics, and internal business processes.

![[HR601] 003. KM Strategy & Implementation](https://cdn.slidesharecdn.com/ss_thumbnails/003-190422041742-thumbnail.jpg?width=640&height=640&fit=bounds)