Downloaded 30 times

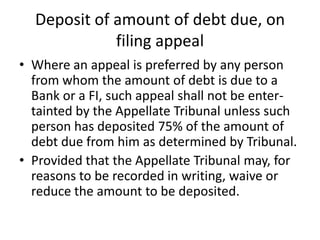

The document discusses the Recovery of Debts Due to Banks and Financial Institutions Act, 1993, which was passed to facilitate the speedy adjudication of matters relating to recovery of debts owed to banks and financial institutions. It established Debt Recovery Tribunals and Debt Recovery Appellate Tribunals across India to handle such cases. The tribunals have similar powers to civil courts and follow procedures to allow banks/FIs to file applications, defendants to respond, and include provisions for appeals, interim orders, and debt recovery. As of now, there are 29 DRTs and 5 DRATs constituted across the country to help banks/FIs recover bad debts efficiently.

![Common Mistakes Attorneys [and Their Clients] Make Drafting and Negotating Co...](https://cdn.slidesharecdn.com/ss_thumbnails/commonmistakesattorneysmake-131107140316-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)