Downloaded 42 times

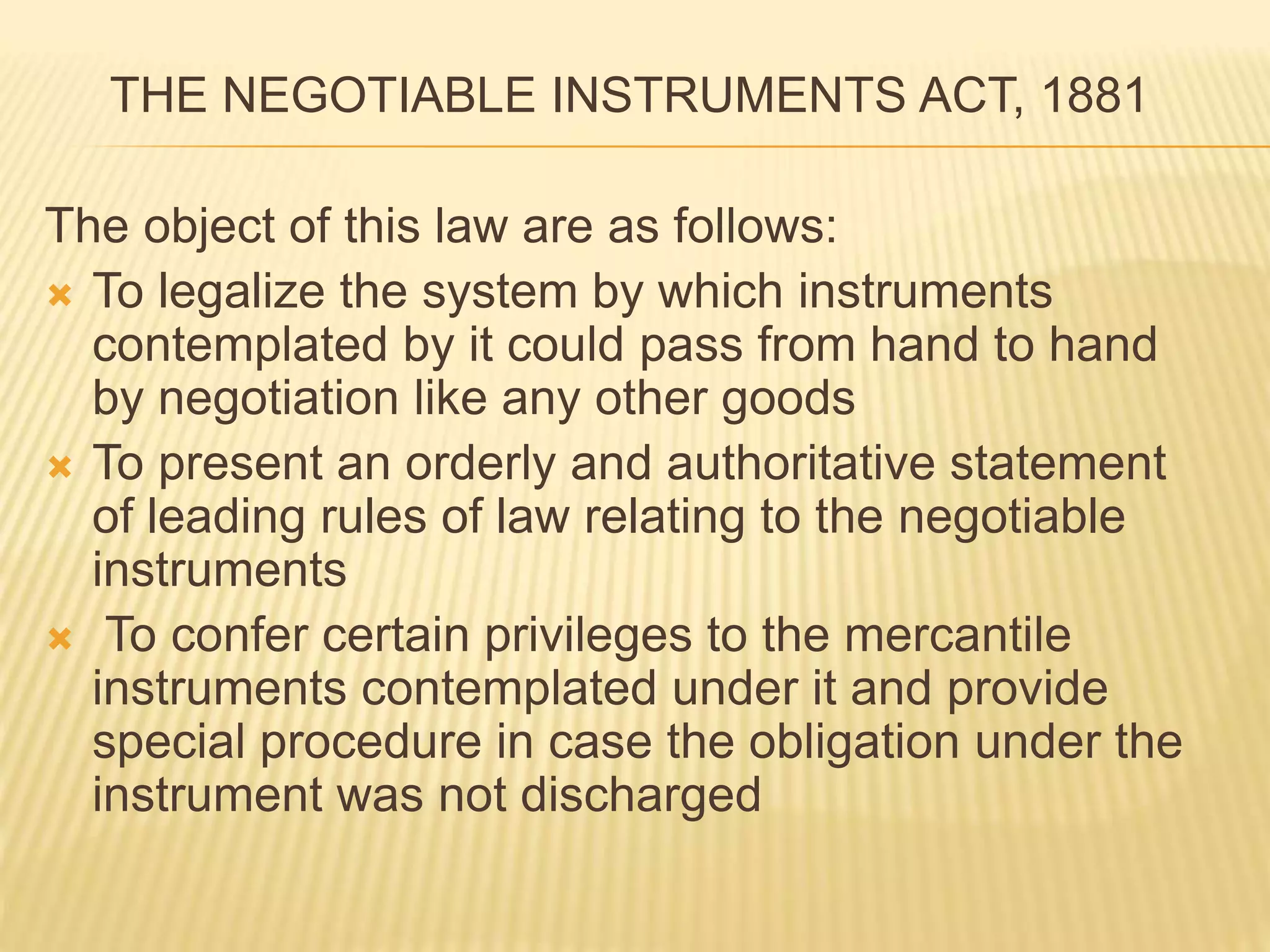

The document discusses several key banking and finance laws in India. It provides an overview of the objectives and importance of studying banking and finance laws in India. It then summarizes some of the major laws administered by the Department of Financial Services, including the Negotiable Instruments Act of 1881, the Reserve Bank of India Act of 1934, the Banking Regulation Act of 1949, the Deposit Insurance and Credit Guarantee Corporation Act of 1961, and the Sick Industrial Companies Act of 1985. The document outlines the purpose and some key aspects of these important banking and finance laws in India.

Introduction to banking and finance laws, their importance, and the regulatory framework in India.

Goals of studying banking and finance laws, including detailed exploration of rules and regulations.

Significance of banking laws in corporate mergers, investments, and startup legal compliance.

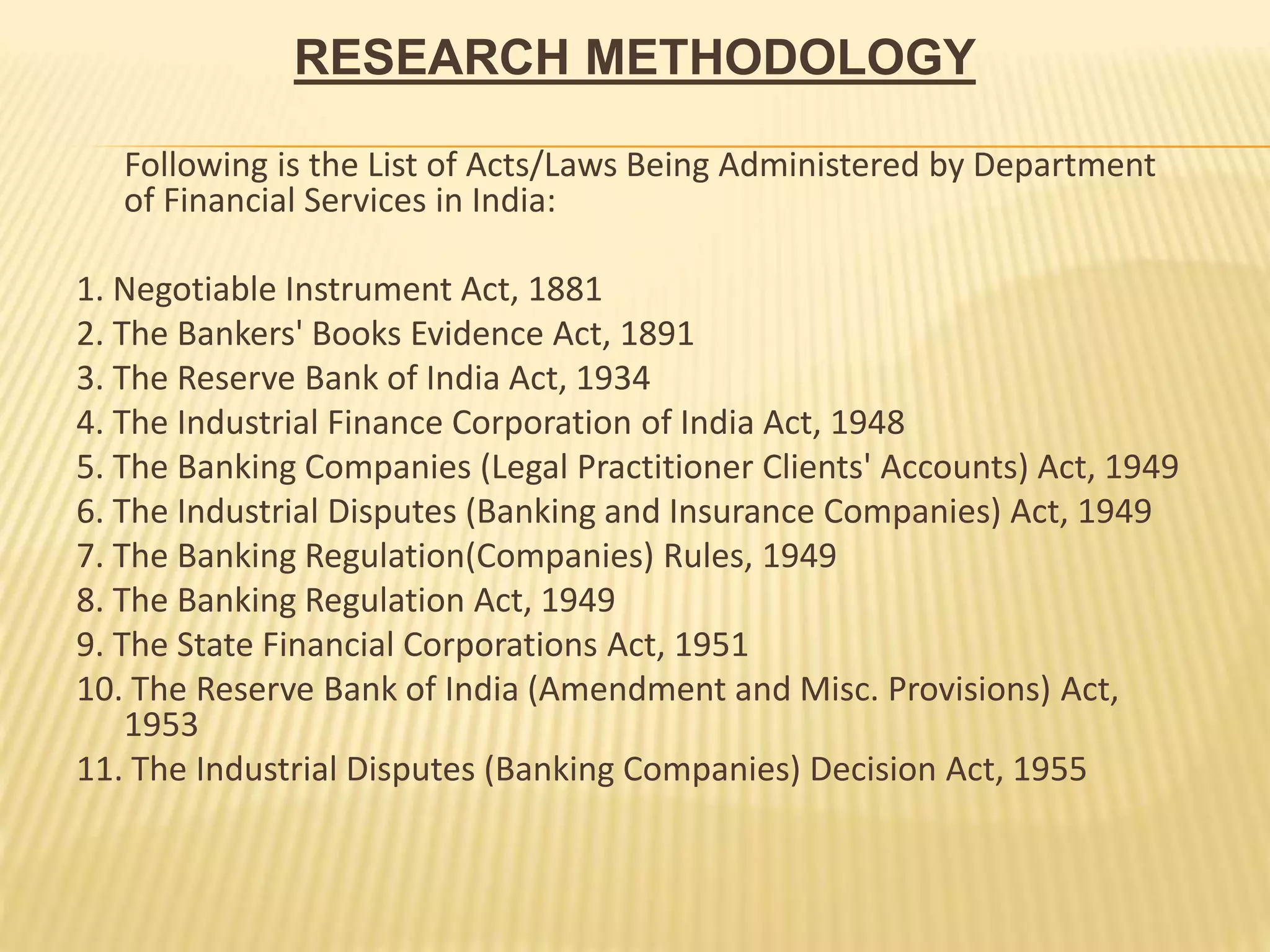

Compilation of important acts administered by the Department of Financial Services in India.

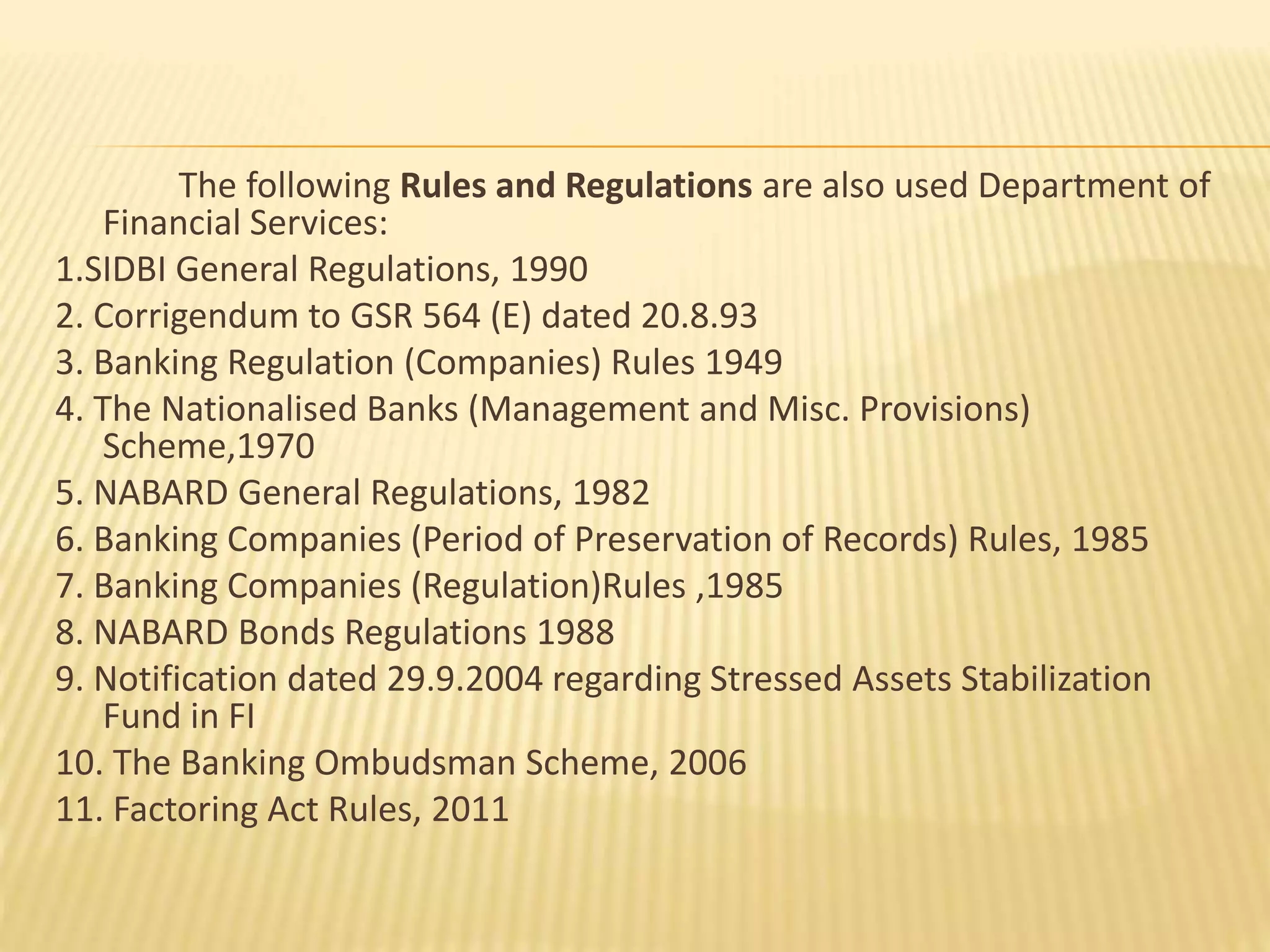

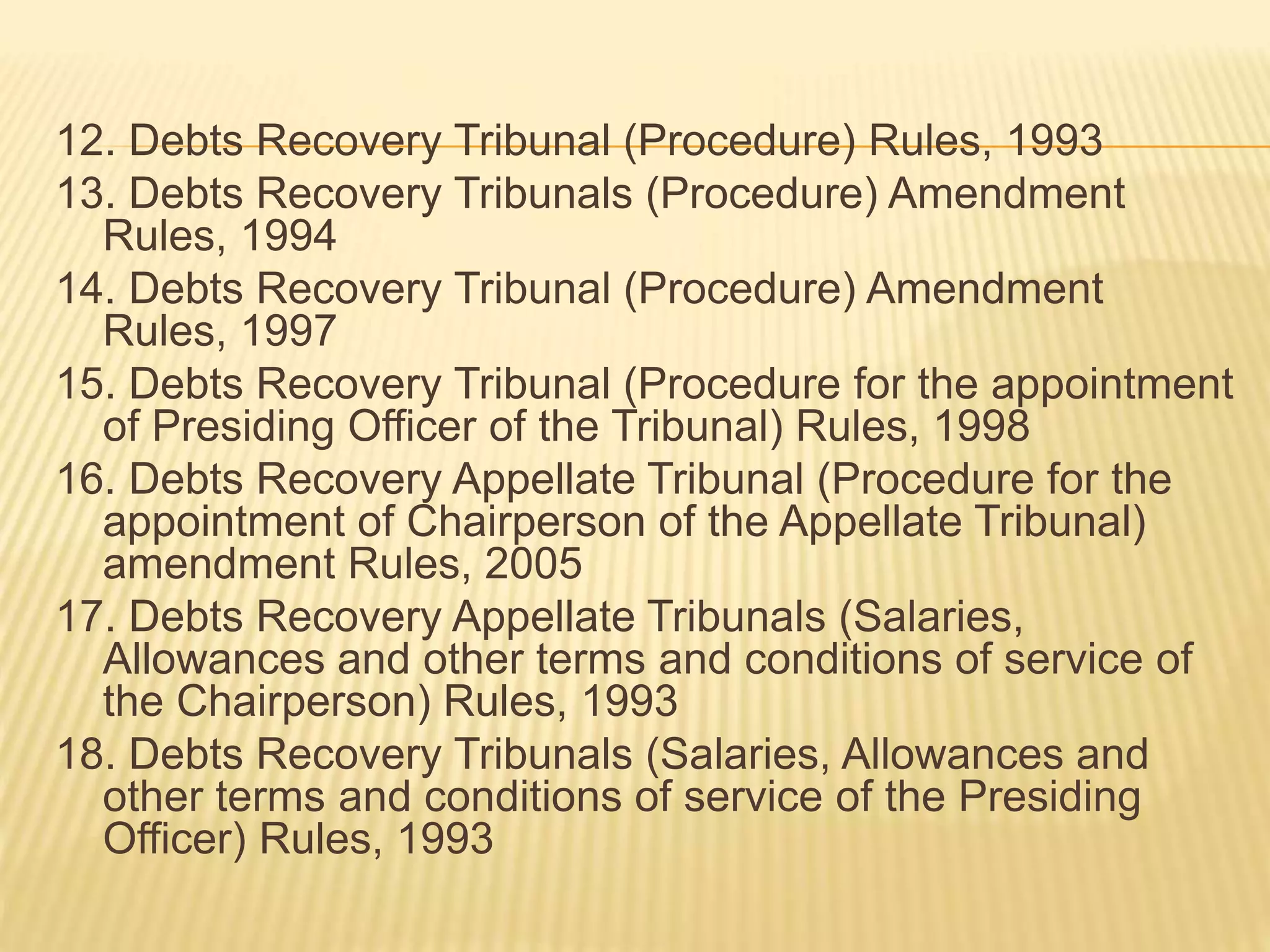

Continued listing of significant laws affecting banking regulation and operations in India.

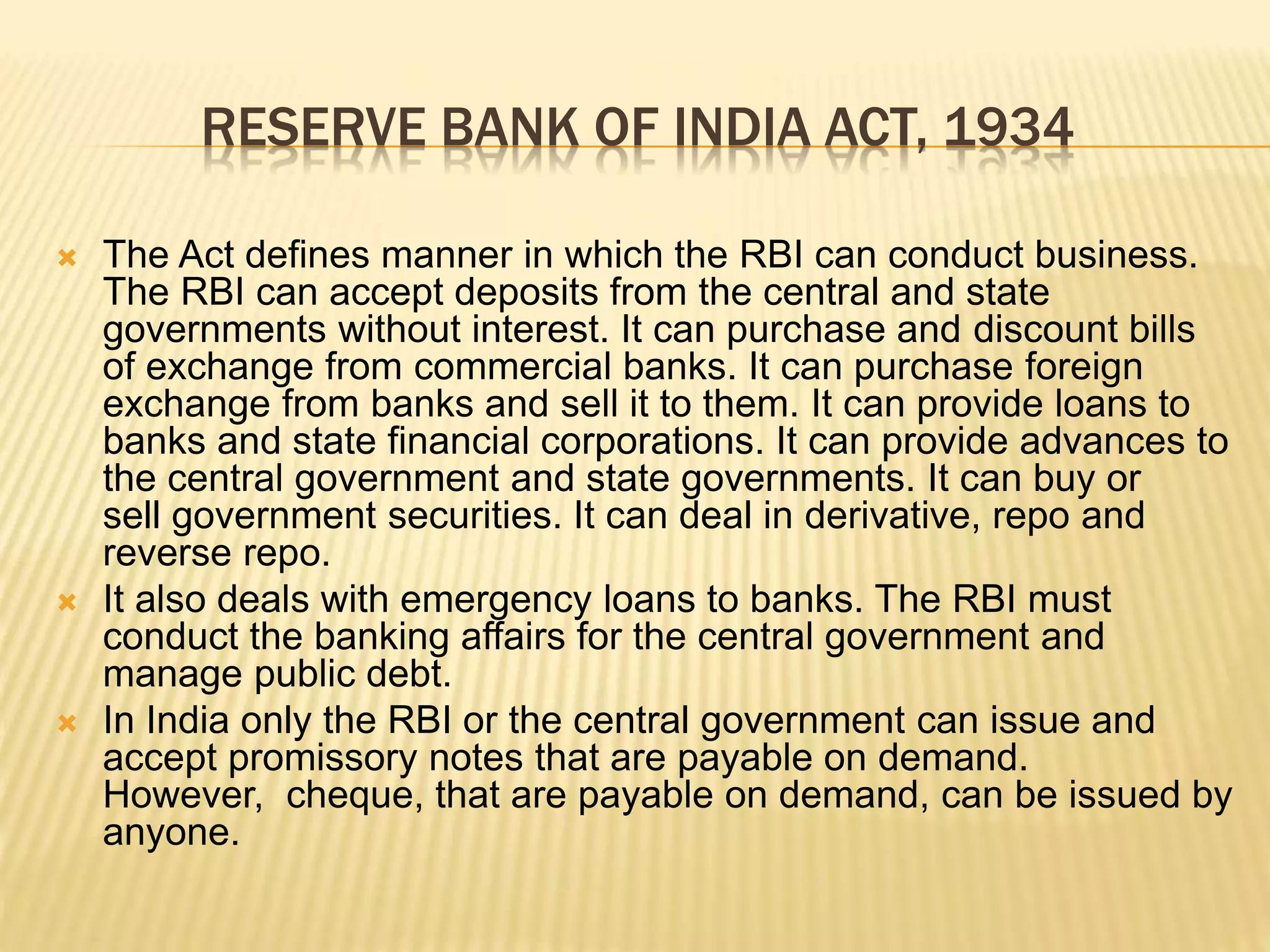

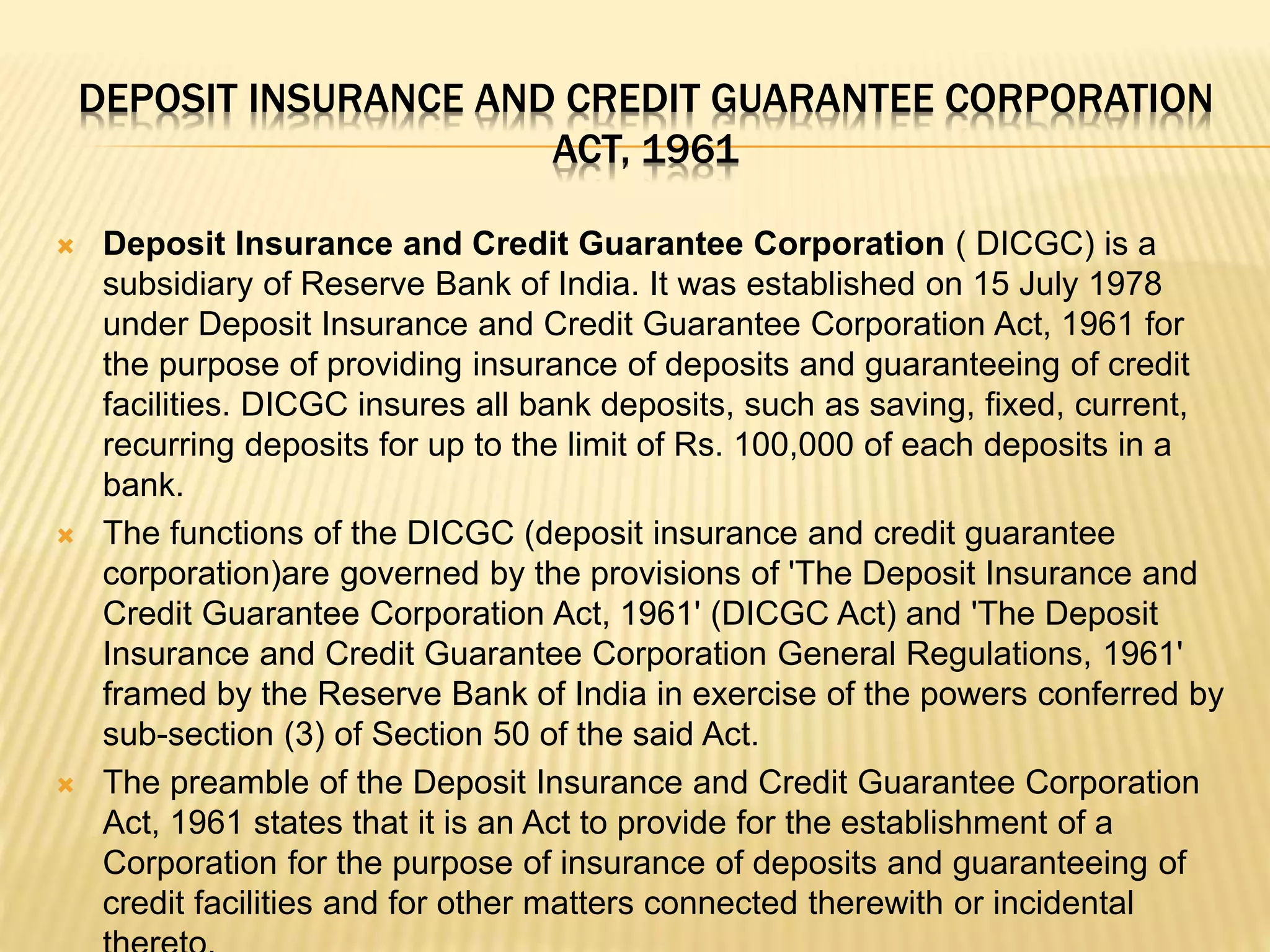

Detailed descriptions of key legislation including Negotiable Instruments Act, RBI Act, and others.

Summary of the importance and implications of studying banking and finance laws in India.

Citing sources used for research and expressing thanks.

![[DSC Europe 25] Marija Vlajkovic & Andrea Radonjanin - Integration of AI tool...](https://cdn.slidesharecdn.com/ss_thumbnails/qf1jrglttoc3bm8s3aop-final-integration-of-ai-tools-251208151905-394f3a6a-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Dragana Ilic - AI for Big Data in Astronomy.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/8palya86qaatvjhva1ms-2-dragana-ilic-ai-ilic-251208151906-652b819c-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Dragan Vucic - Building the Learning Organization - How AI Tr...](https://cdn.slidesharecdn.com/ss_thumbnails/8brigo2sbu6qur6gxrra-7-251205085715-6ae07d24-thumbnail.jpg?width=640&height=640&fit=bounds)