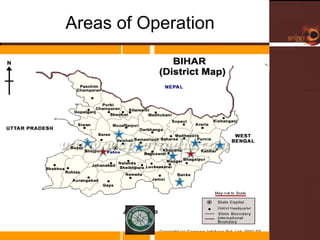

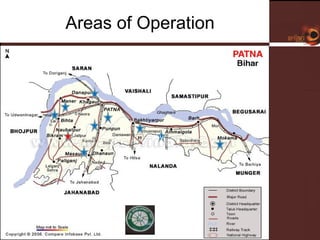

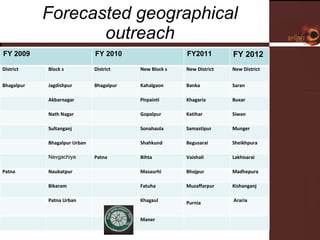

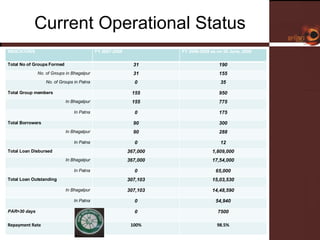

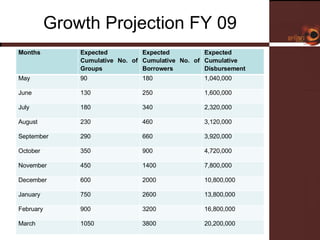

The document summarizes the business plan of Bihar Development Trust, a microfinance startup in Bihar, India. It aims to adapt successful models like Grameen to provide affordable credit and savings services to underserved communities. In its first year of operations, it formed 31 groups with 155 members and disbursed loans totaling $367,000. It plans rapid geographical expansion across Bihar to reach over 6 million potential microfinance clients and create employment and economic opportunities.

![Thank You Organisation Name: Bihar Development Trust Managing Trustee: Ravi Chandra Executive Trustee: Dev Kumar Dubey E mail: [email_address] Phone No: 9470017752, 9431609939](https://image.slidesharecdn.com/samvridhi-1216014470842367-9/85/Samvridhi-33-320.jpg)