Downloaded 28 times

![All figures in INR million

• Annualized portfolio Return (APR) at

Profit & Loss Account FY 2007 FY 2008 FY 2009 FY 2010

26.5%. [against industry avg. of 28%]

Income

Income from Operations 469 1,133 3,424 7,004

• Operating expense ratio at 5.1%

Other Income 26 141 143 237

[against industry average of 12%]

Total Income 495 1,274 3,567 7,241

Expenditure

Financial expenses 148 417 1,182 2,210 • Provisions and write-offs include a 1%

Personnel expenses 143 233 587 1,144 standard asset charge – higher than

the RBI prescribed norms

Operating and other expenses 67 81 165 362

Depreciation 6 9 26 54

Provisions and write offs 89 75 187 360 • Return on Assets at 7%+ [against

Total Expenditure 453 815 2,147 4,130 industry average of 3.5%]

Profit before tax 43 459 1,420 3,111

Tax 16 189 517 1,075 • Return on Equity at 52% [highest in

Profit after tax 27 270 903 2,036 the industry]

Balance in P & L brought fwd - - 216 939

Amount available for appropriation 27 270 1,119 2,975

• Audited by one of the top-4 Audit firms

Transfer to statutory reserve 6 54 181 407

Balance carried to balance sheet 21 216 939 2,568

Earnings per share • 1USD = 46 INR (approx)

Basic and diluted - Rs.10/ share 3 29 80 152](https://image.slidesharecdn.com/spandanacorporateppt2-111031050101-phpapp01/75/SpN-corporate-PPt-13-2048.jpg)

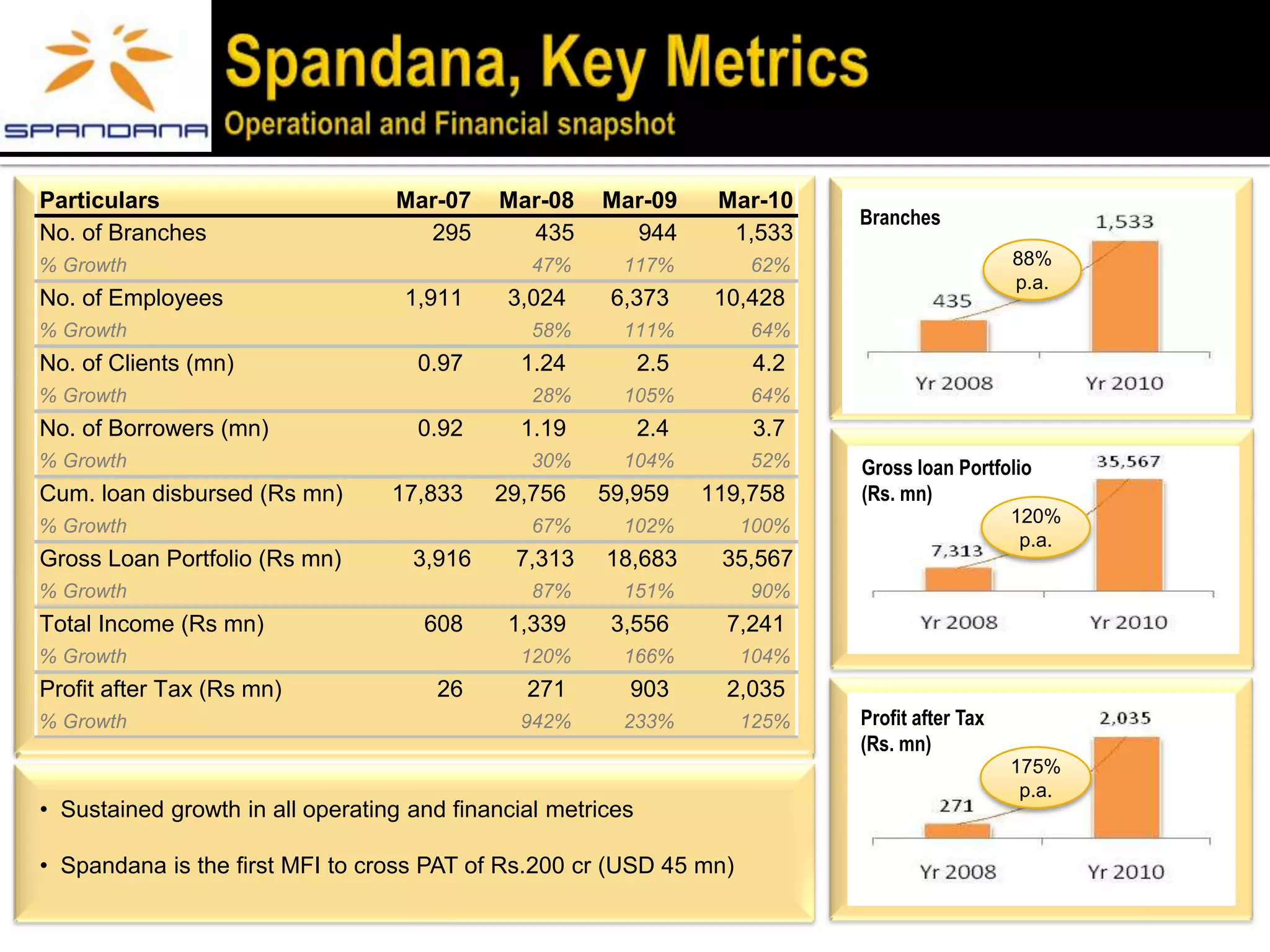

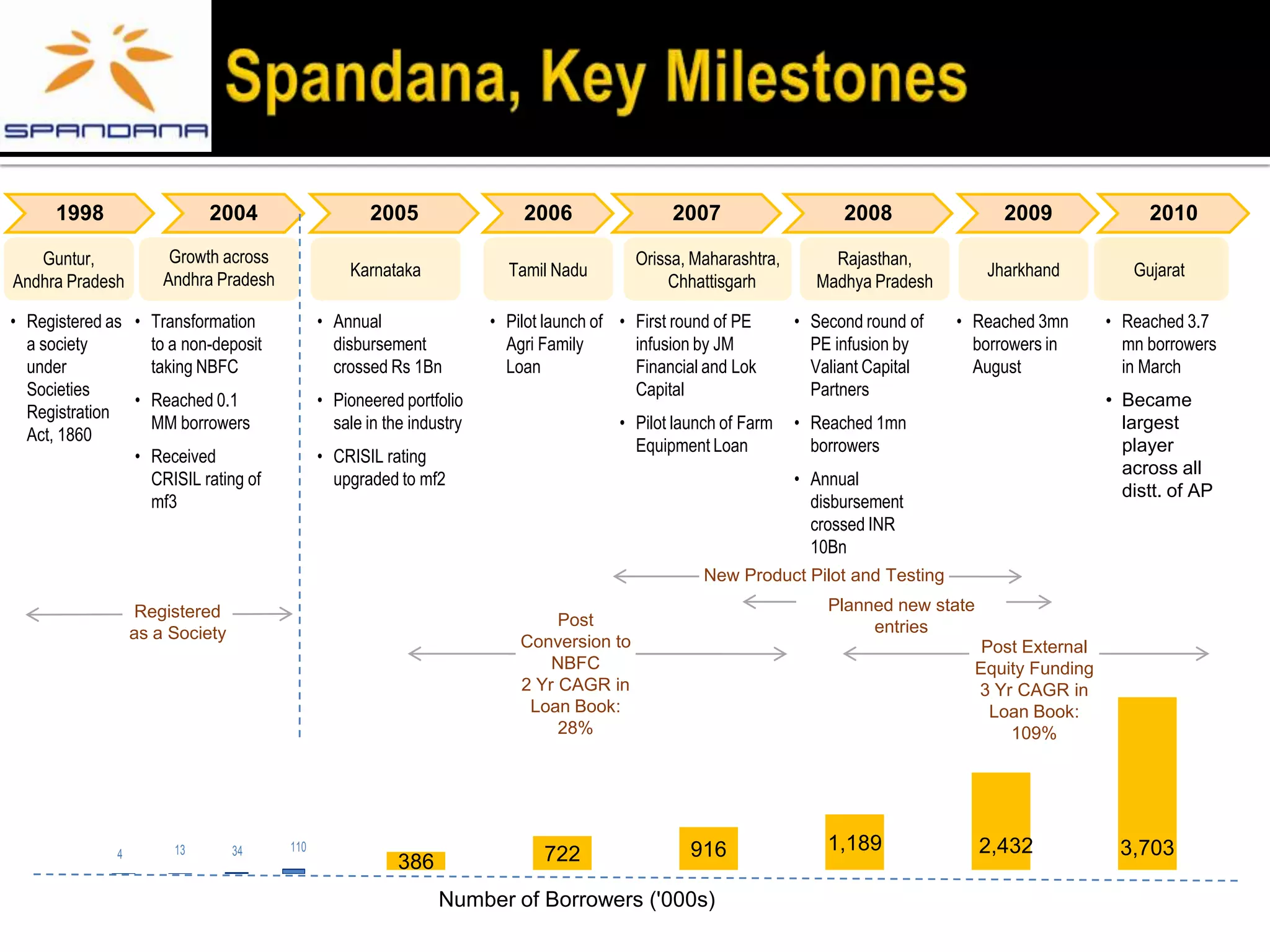

Spandana is one of the largest microfinance institutions in India with over 4.2 million clients served across 1,533 branches. It has demonstrated strong and consistent growth over the past decade across key metrics like number of branches and employees, clients, loan disbursements and portfolio. Spandana's profit after tax has grown at an annual rate of over 175% in the last 10 years. It has established itself as an industry leader in scale and operational efficiency.

![Sentencia cristina carrefour-alfonso_molina[1]](https://cdn.slidesharecdn.com/ss_thumbnails/sentenciacristina-carrefouralfonsomolina1-100531155250-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)