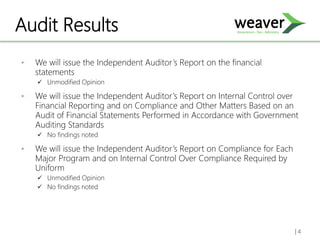

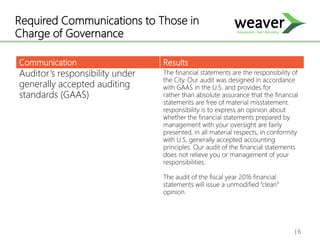

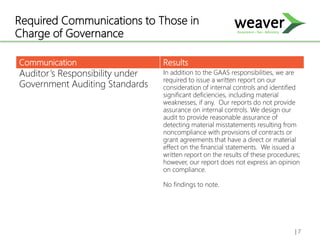

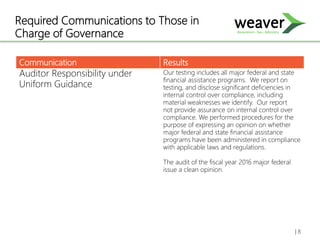

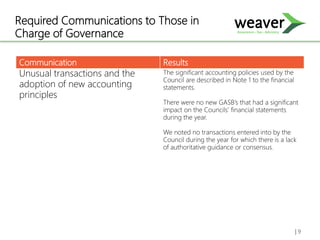

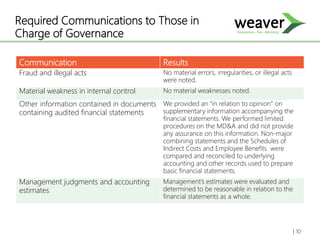

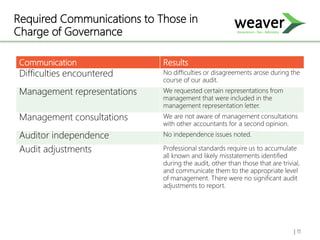

The audit of the City of Killeen's financial statements for the year ended September 30, 2016 resulted in unmodified opinions and no findings. The auditors found no issues with internal controls over financial reporting, compliance with laws and regulations, or compliance with requirements for major federal programs. Management's estimates and judgments were deemed reasonable. The auditors encountered no difficulties during the audit and had no independence issues.

![EC Treasurer Report by Kenny Huang [APRICOT 2015]](https://cdn.slidesharecdn.com/ss_thumbnails/amm-treasurerslides-150305181657-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)