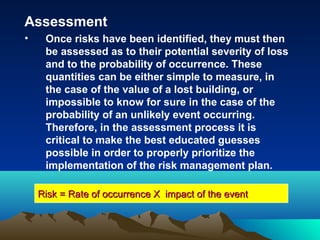

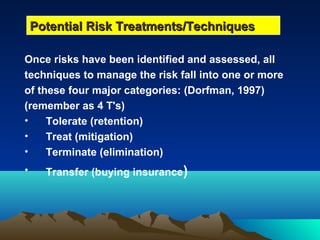

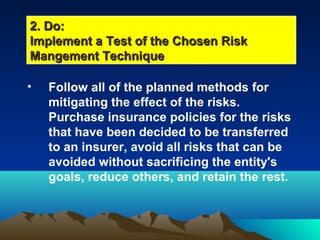

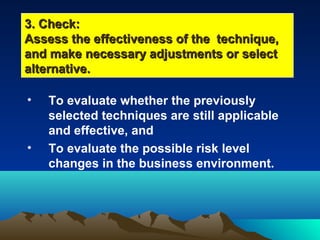

This document defines key concepts in risk management including risk, risk analysis, risk assessment, risk communication, and risk management. It explains that risk management involves identifying potential risks, assessing their likelihood and impact, selecting techniques to address them such as tolerating, treating, transferring or terminating risks, then implementing and continually improving the risk management process using a plan-do-check-act framework. Common risk management strategies are outlined along with limitations of the approach.