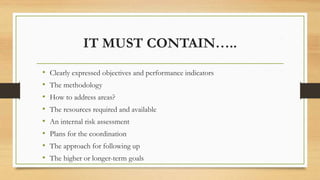

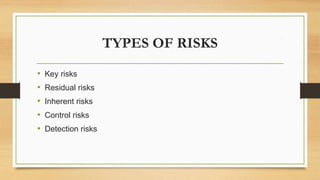

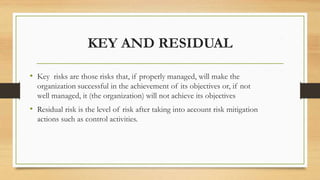

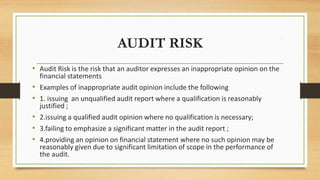

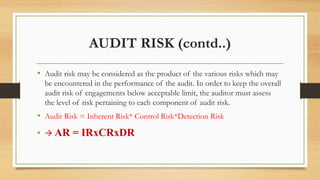

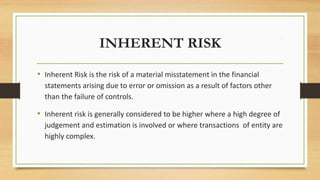

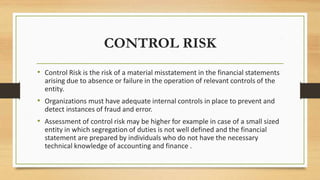

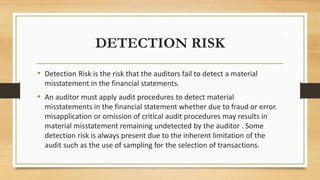

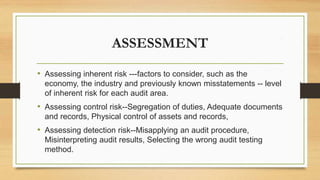

This document discusses risk-based audit approaches. It defines key risks as those that could impact an organization achieving its objectives if not properly managed. It also defines inherent, control, and detection risks. The document outlines the basic conceptual framework for risk-based audit planning, which involves determining the audit universe, identifying risks, assessing risks, developing risk-based audit plans, and presenting results. It provides examples of risk factors and types of risks that should be considered in audit risk assessment.

![IDENTIFYING RISKS AND ASSESSING THEIR IMPACT

AND PROBABILITY [SCORING]

Criteria for assessing impact

• Financial impact.

• Impact on reputation.

• Regulatory impact

• Impact on mission/achievement of objectives/operations.

• Impact on people](https://image.slidesharecdn.com/0210-risk-based-audit-approach-new-20211020142926-240212040806-86a6e7fd/85/0210-RISK-BASED-AUDIT-APPROACH-new-20211020142926-ppt-10-320.jpg)