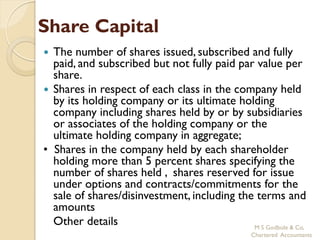

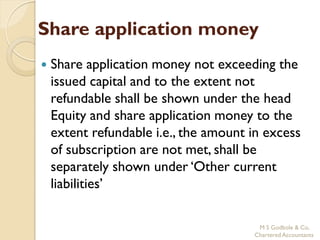

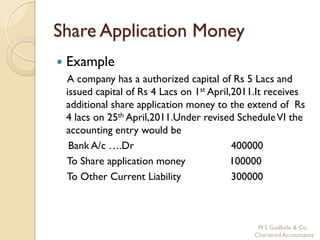

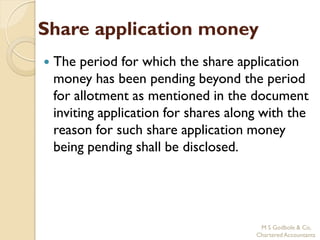

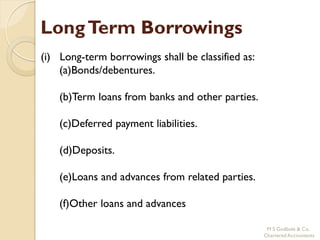

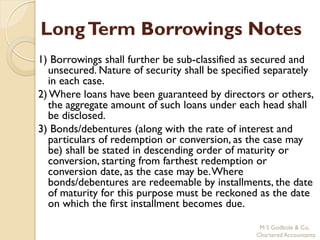

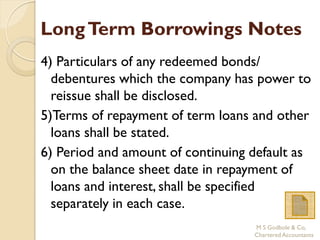

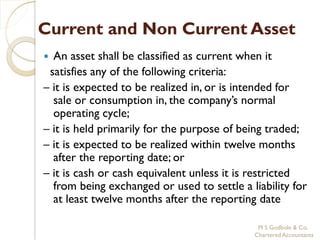

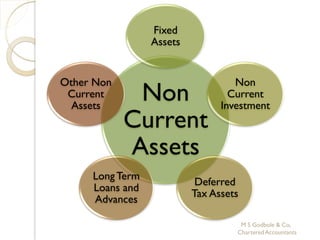

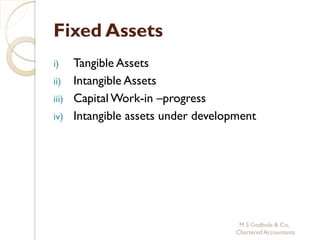

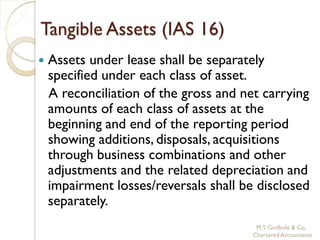

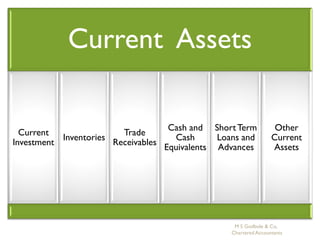

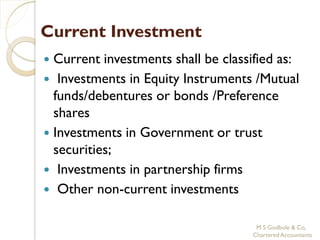

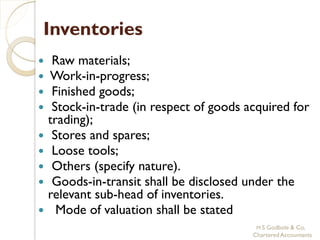

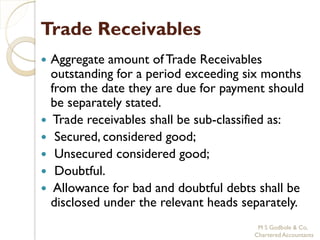

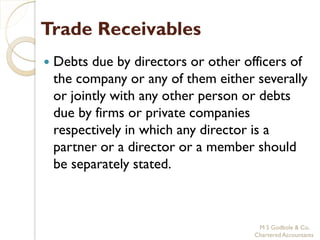

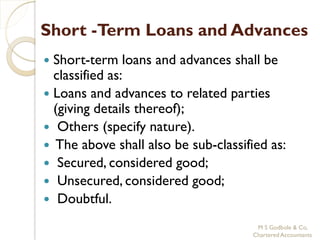

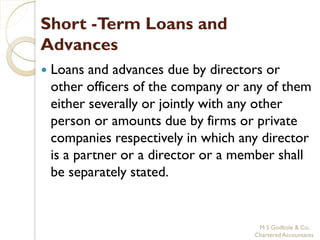

This document provides guidance on preparing the balance sheet format according to the Companies Act, 1956 and Schedule VI. It discusses the key components of the balance sheet including share capital, reserves and surpluses, non-current liabilities, current liabilities, non-current assets, current assets, and notes on the classification and presentation of items. The document also provides accounting treatments and disclosure requirements for items like share capital, borrowings, investments, provisions, taxation etc. according to Indian accounting standards.