Download as PDF, PPTX

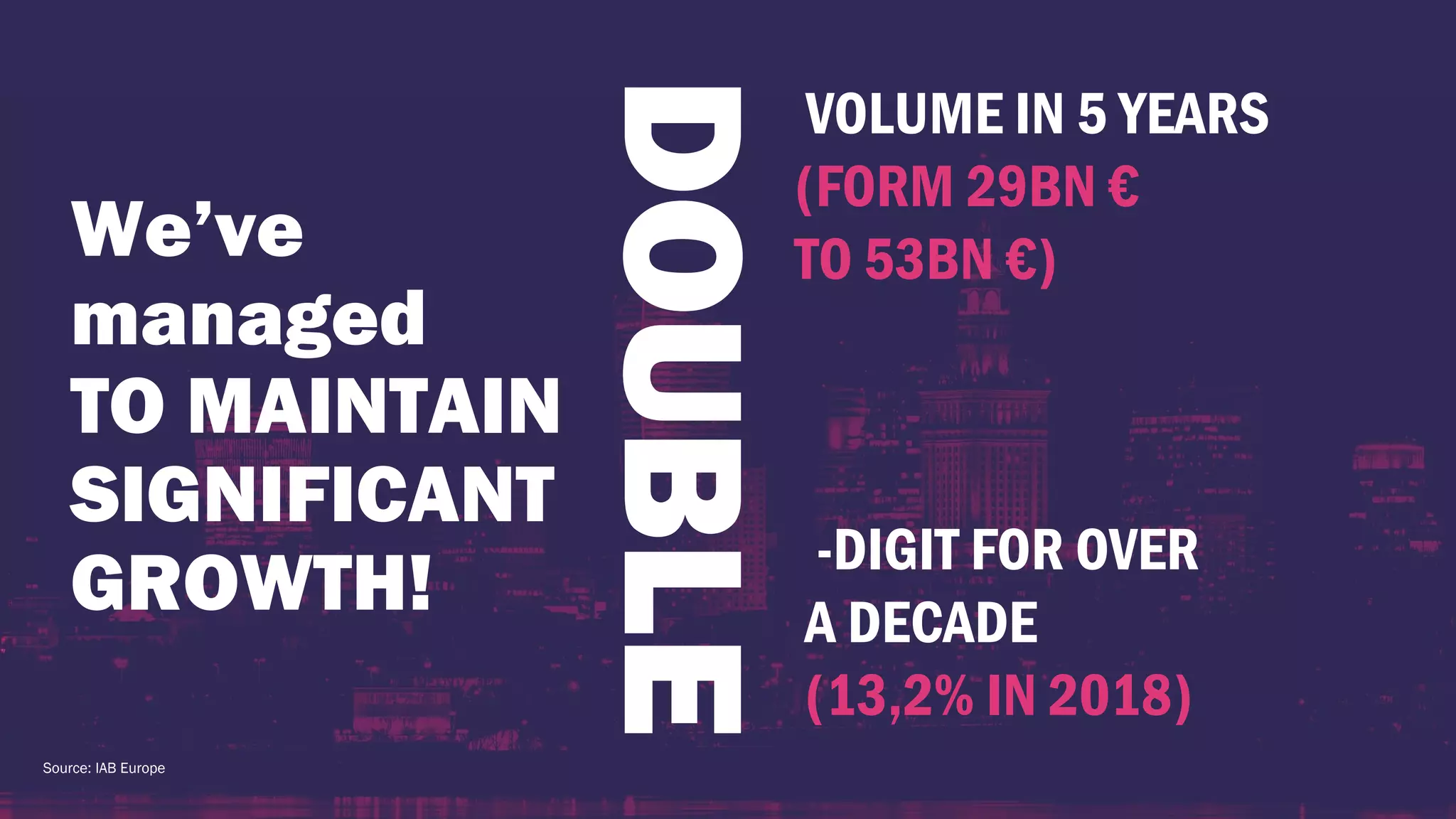

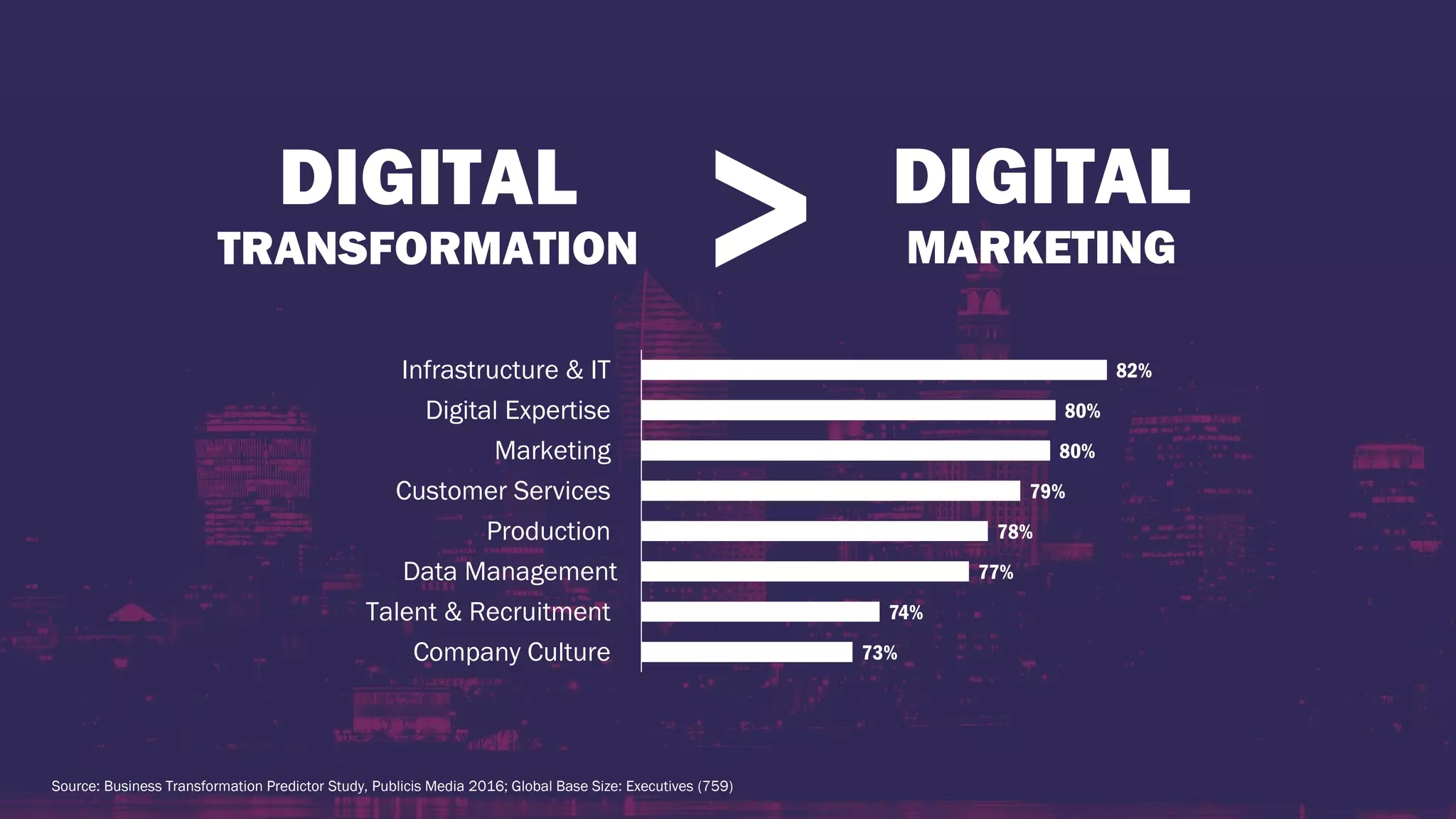

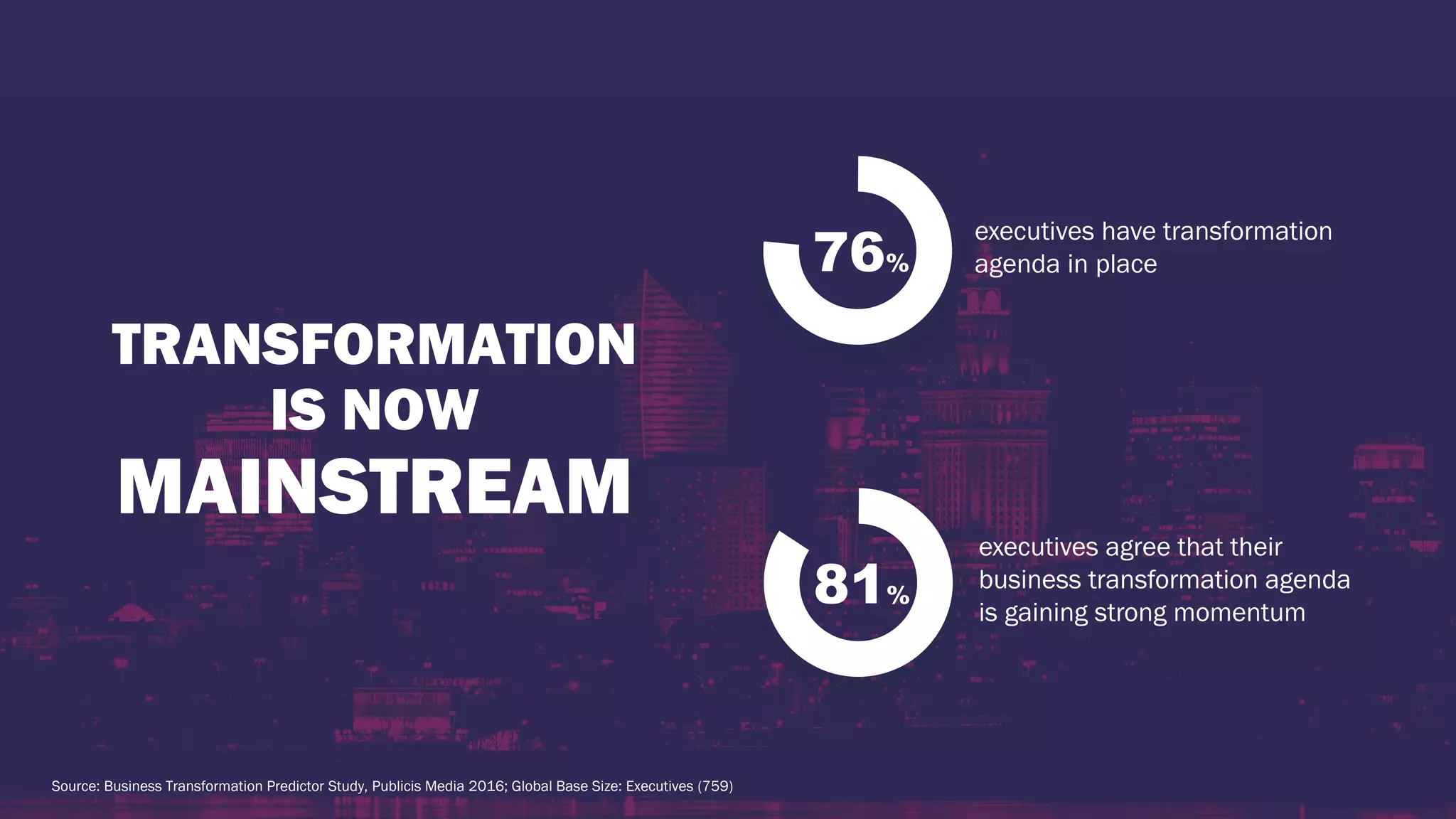

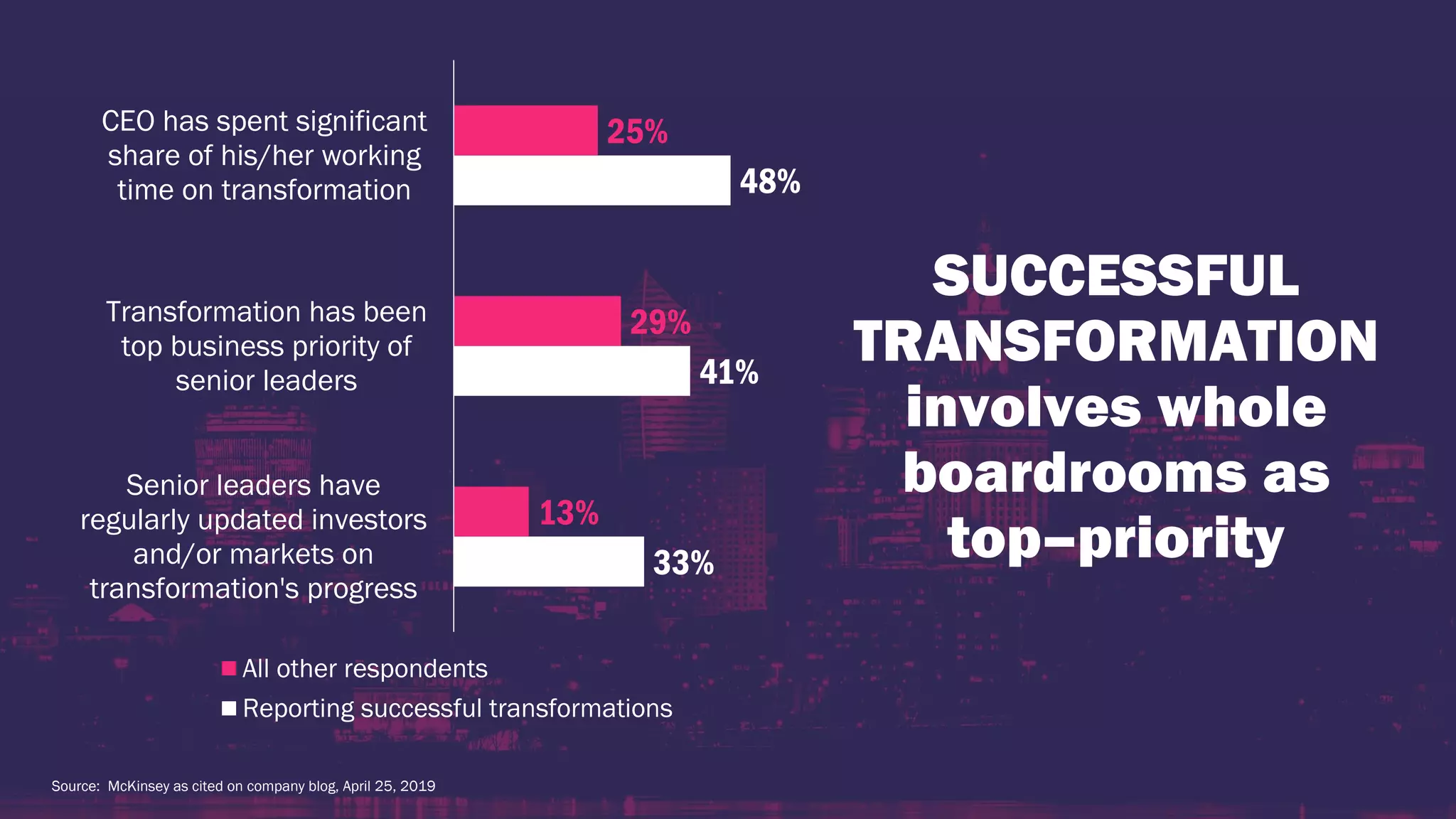

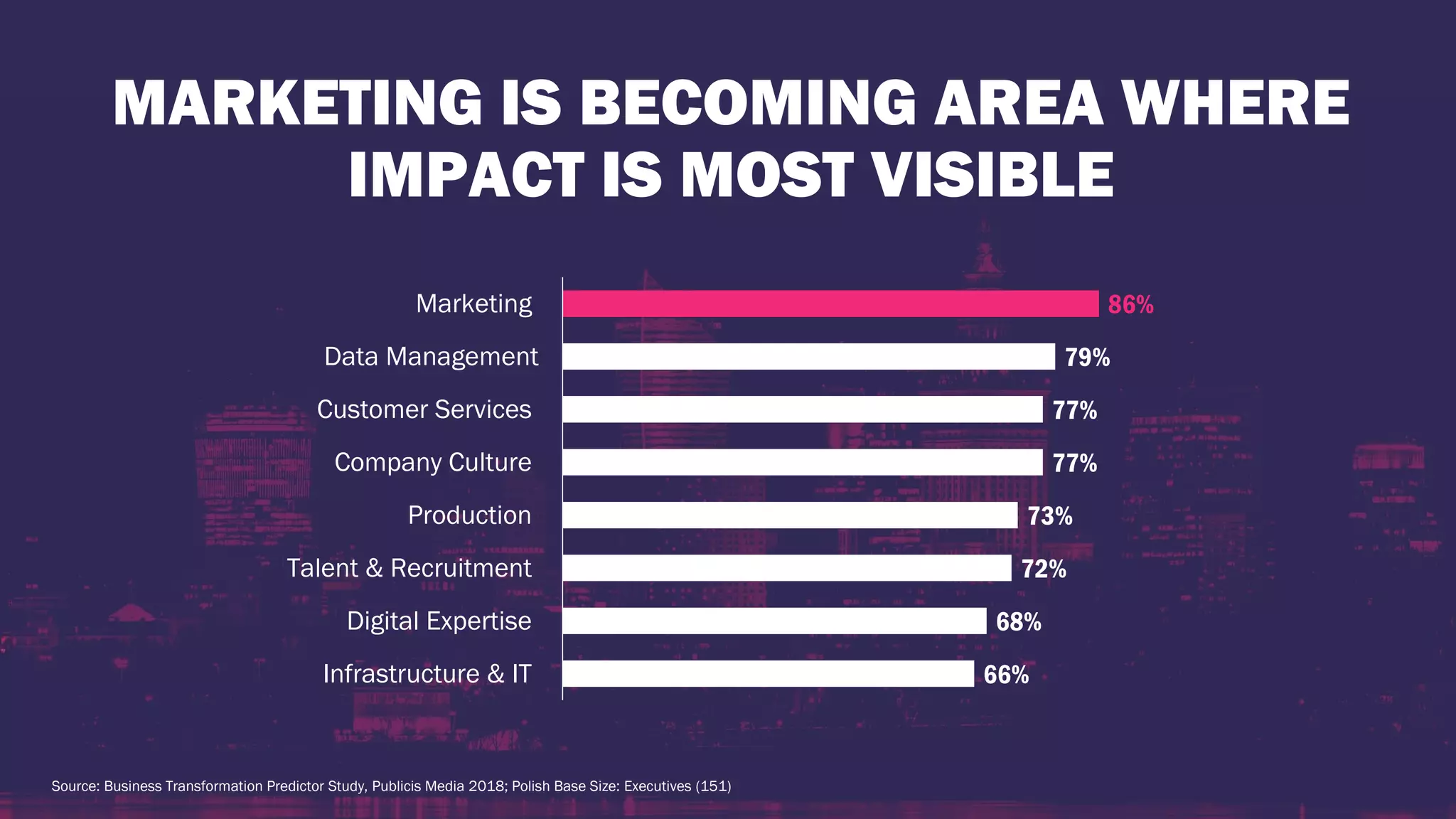

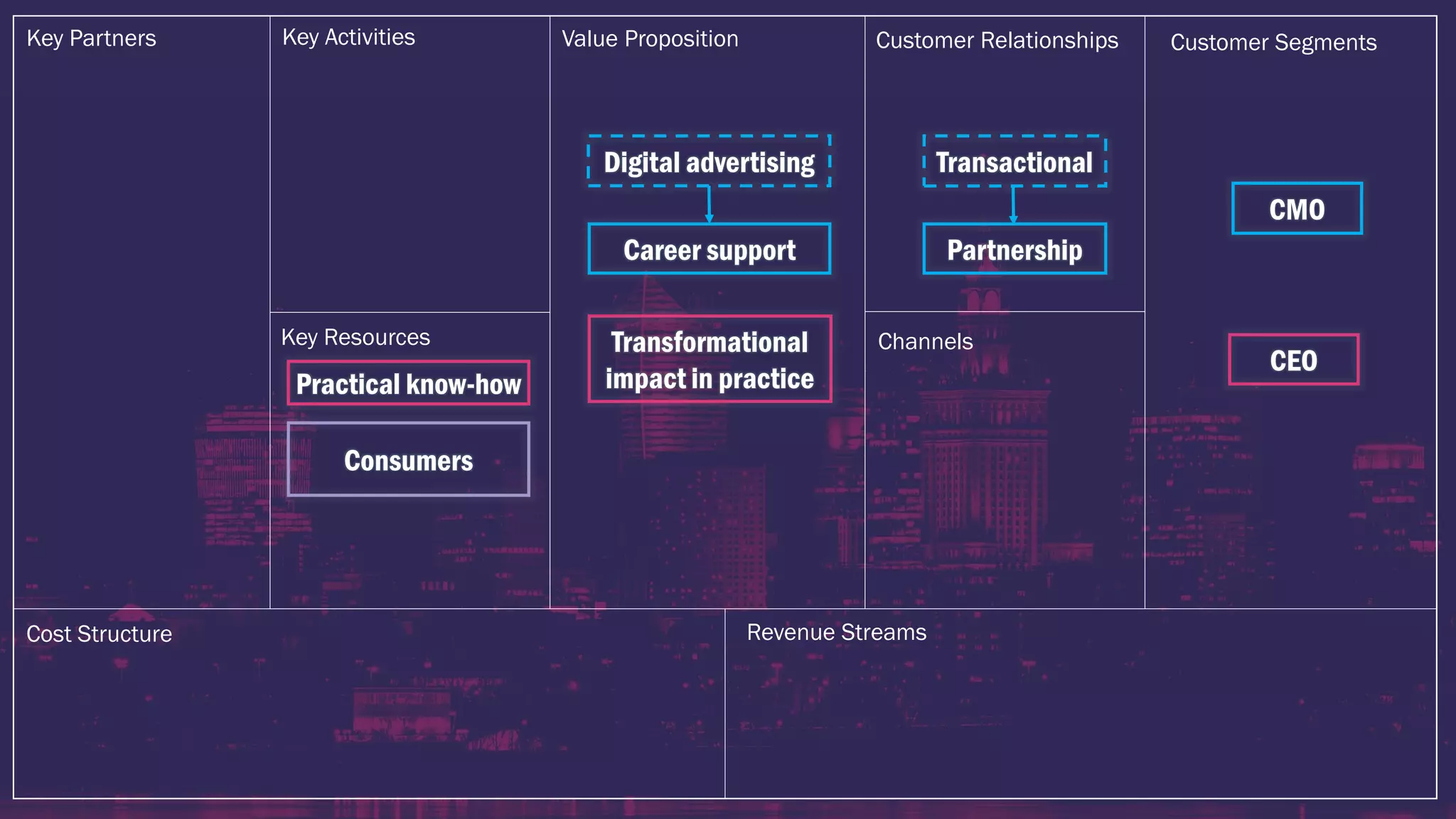

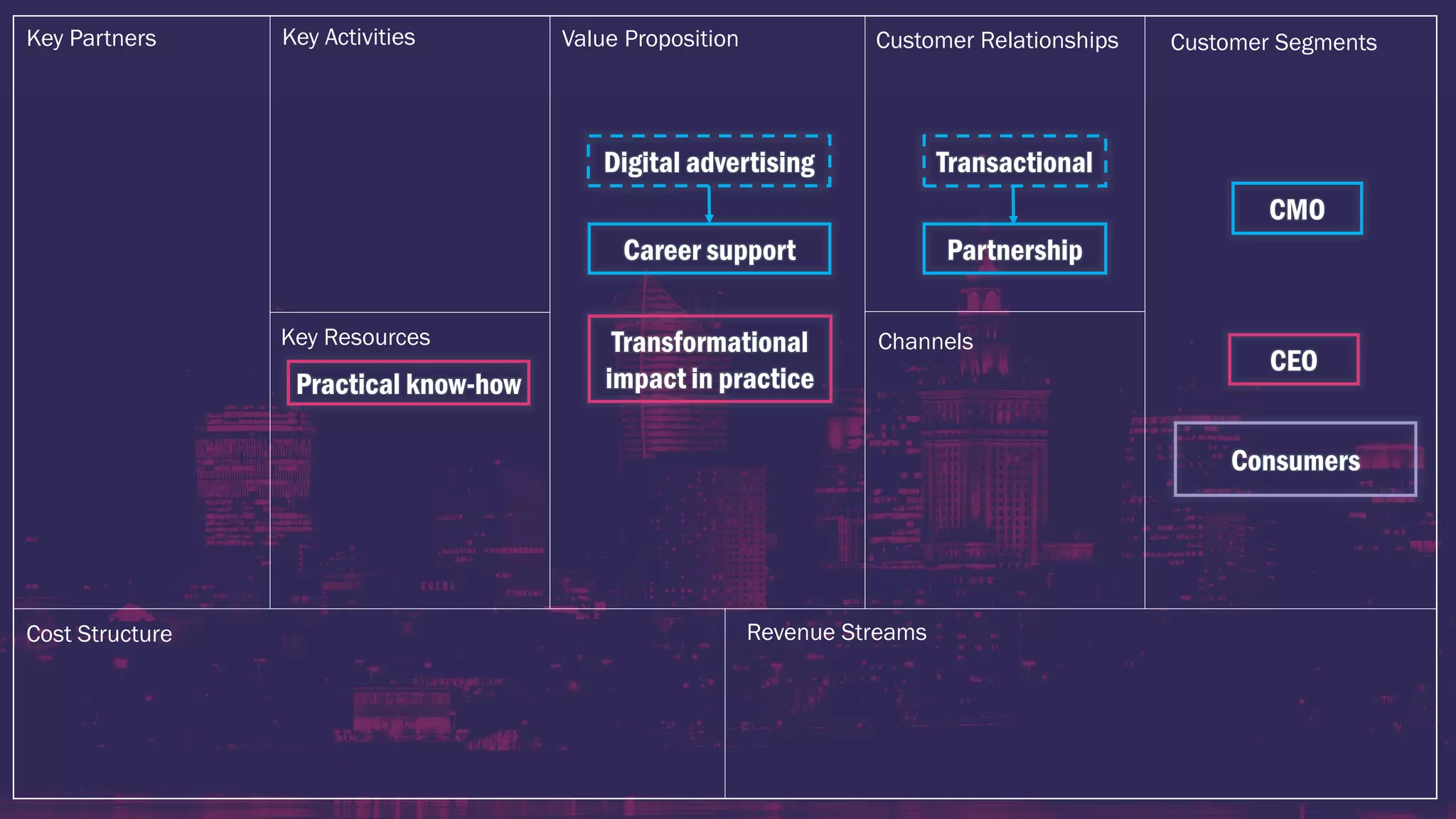

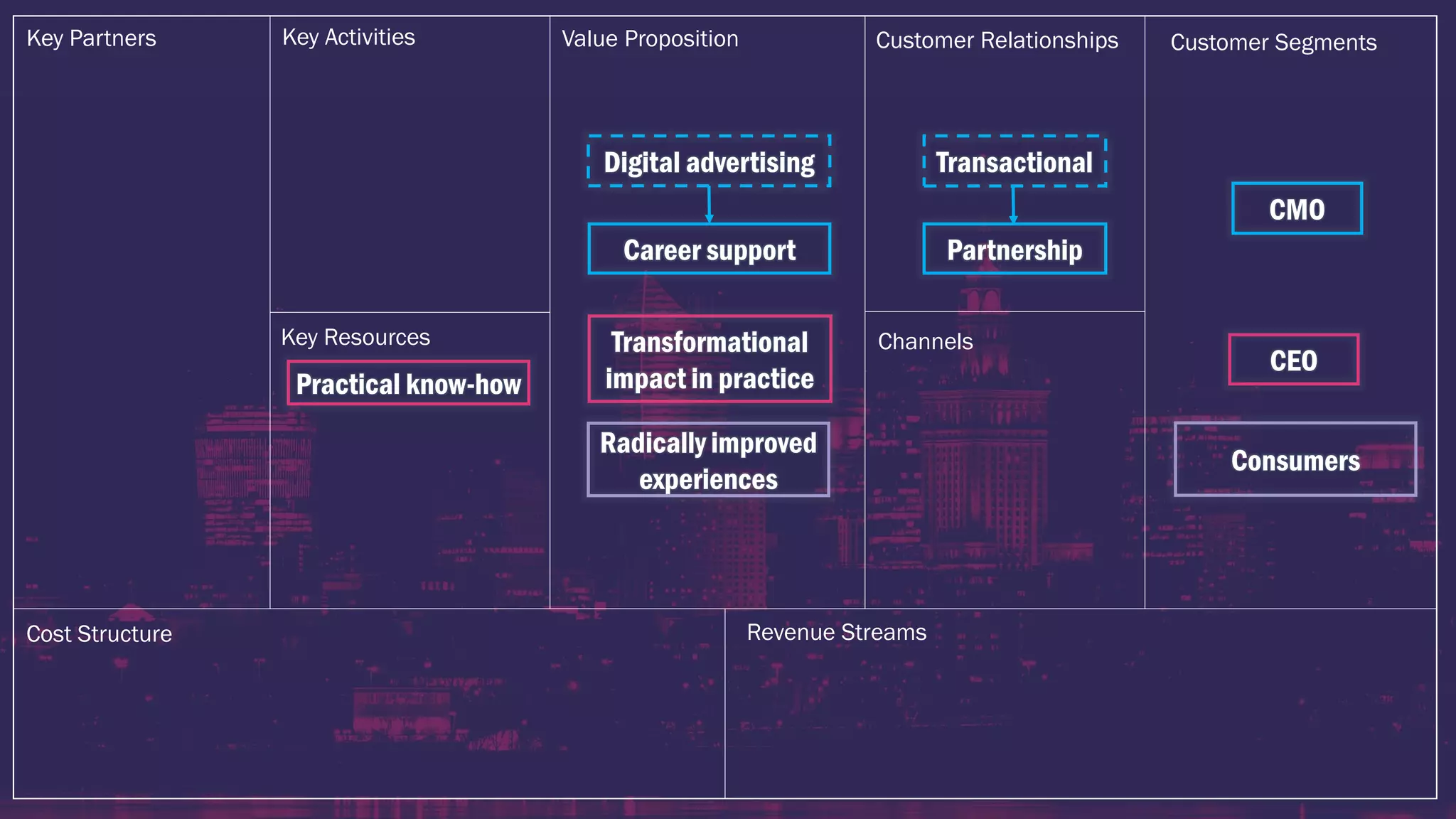

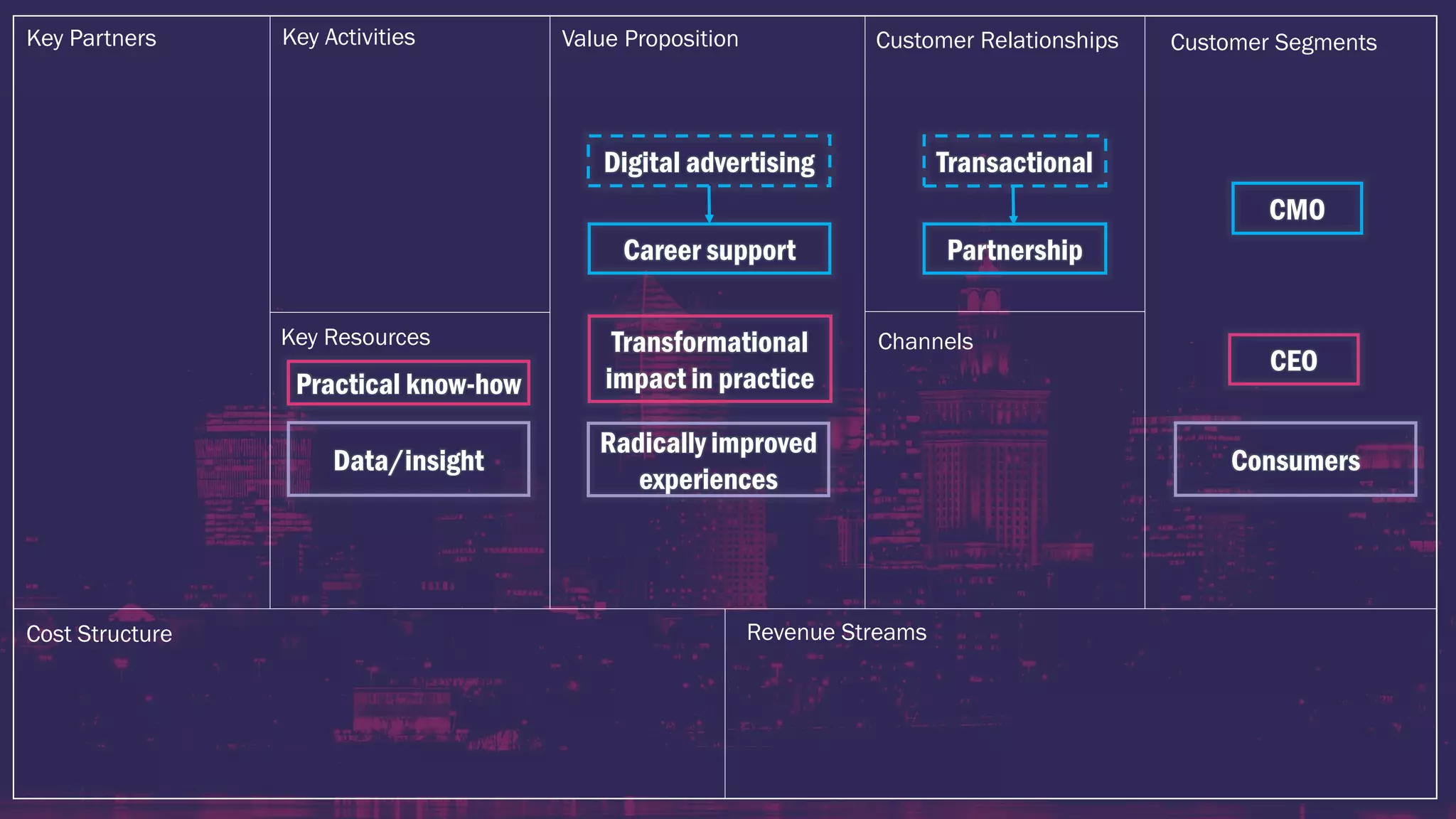

The document discusses the significant impact of digital transformation on business, highlighting a substantial growth in the digital market over the past few years. It emphasizes the importance of executive commitment to transformation and the role of marketing in driving innovation. The analysis also points to a changing competitive landscape, with technology integration and data management as key components of successful transformation strategies.

![[En] Accenture 2013-2014 survey on CMOs and digital transformation - Adobe So...](https://cdn.slidesharecdn.com/ss_thumbnails/accenture-cmo-insights-2014-pdf-140719002815-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)