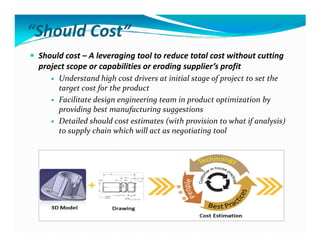

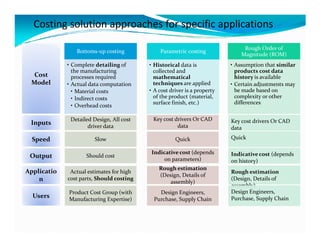

This document discusses the need for product costing solutions and Vedant Resources and Infrastructure Development's should costing services. It notes that product costs account for 70% of revenue and are key to profit but detailed cost breakdowns are unknown in the concept stage. The challenges include engineers being unfamiliar with manufacturing processes and limited cost data during development. Vedant provides should costing, tear down analysis, local sourcing support, and cost estimation to help understand cost drivers, optimize design for cost, and aid in supplier negotiations. Their approaches include bottom-up, parametric, and rough order of magnitude cost modeling at different levels of detail and speed.