Download as PDF, PPTX

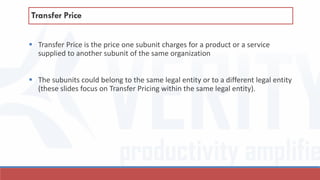

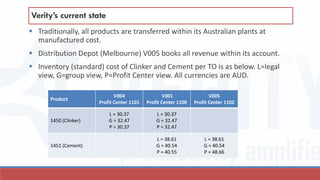

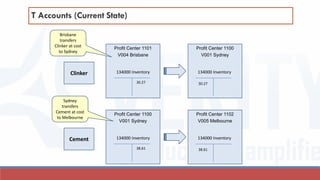

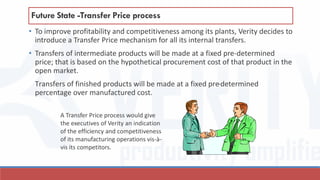

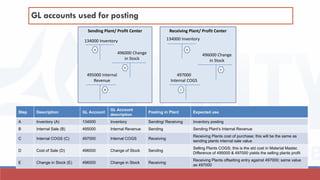

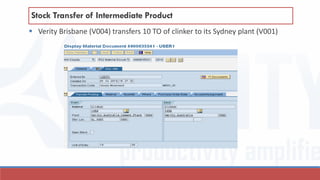

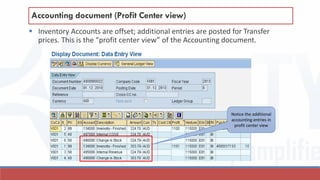

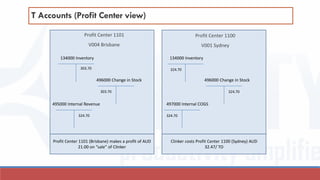

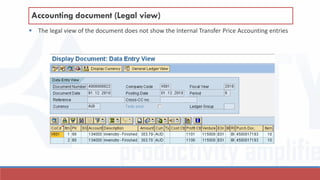

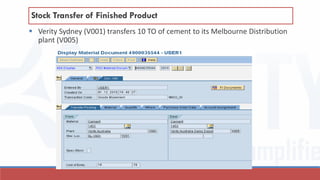

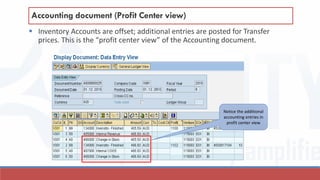

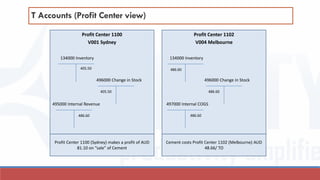

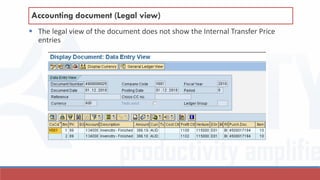

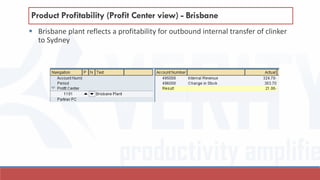

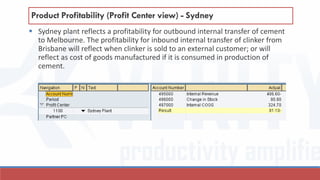

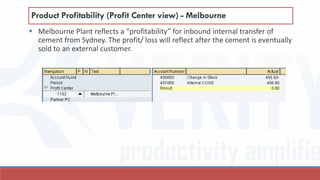

Verity Cement uses SAP Material Ledger to implement intra-company transfer pricing between its manufacturing plant in Brisbane, plant in Sydney, and distribution center in Melbourne. Previously, transfers were done at cost without reflecting individual profitability. The new system uses negotiated transfer prices based on market costs for intermediate goods and a margin over standard cost for finished goods. This allows each subunit to measure independent profitability and improve competitiveness through the profit center view in SAP.