Download to read offline

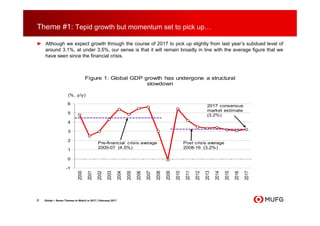

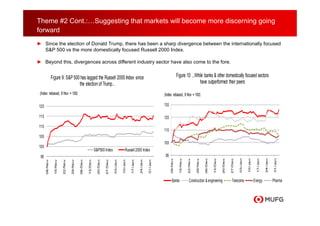

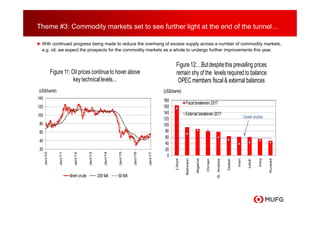

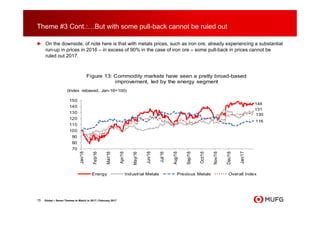

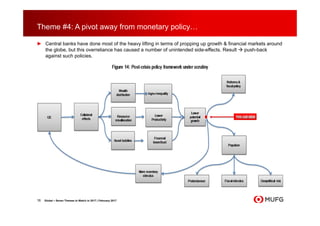

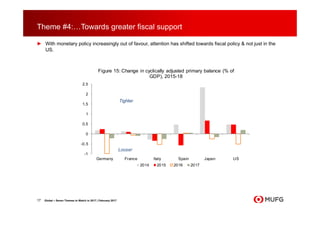

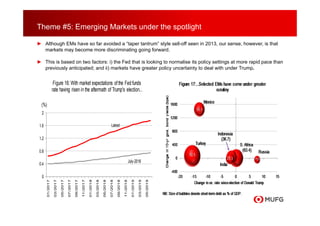

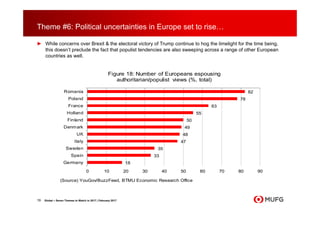

This document provides a summary of seven themes to watch in global markets in 2017 according to Bank of Tokyo-Mitsubishi UFJ. The themes are: 1) tepid global growth expected to pick up slightly, 2) markets will remain influenced by policies and actions of US President Donald Trump, 3) commodity markets are expected to continue recovering from oversupply, 4) a shift from monetary to fiscal policy support, 5) emerging markets will face more scrutiny, 6) political uncertainties in Europe are expected to rise, and 7) banks are anticipated to perform well. The document outlines factors and risks underlying each theme.