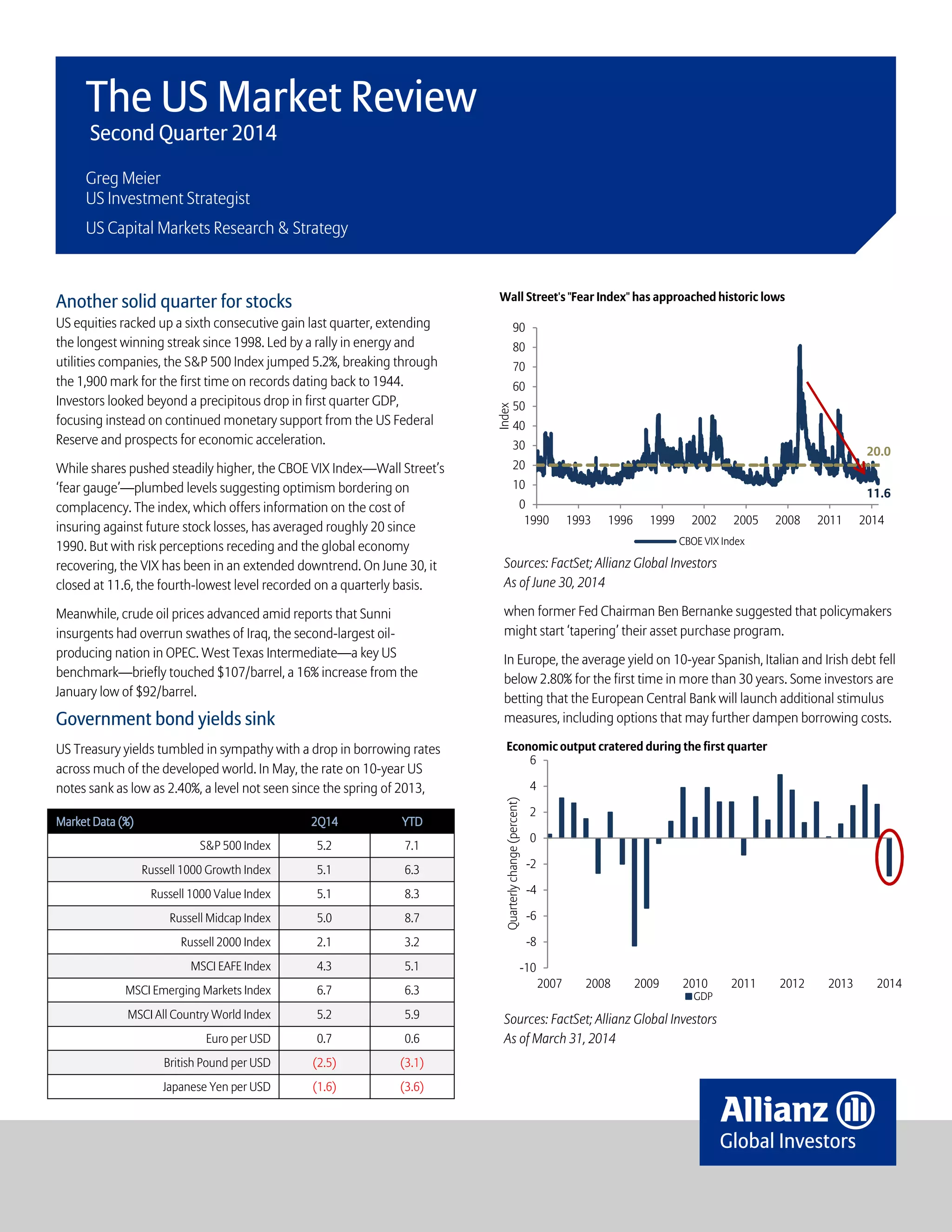

US stocks gained for a sixth consecutive quarter, with the S&P 500 rising 5.2% to break 1900 for the first time. Investors looked past a sharp drop in first quarter GDP, focusing on continued Fed support and an expected economic acceleration. Treasury yields fell globally on expectations of further central bank stimulus in Europe. Corporate earnings are forecast to grow through the rest of 2014 after a weak start, supporting the outlook for stocks.