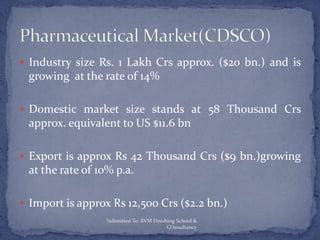

The document discusses the evolution of the Indian pharmaceutical industry over five phases from 1950 to 2010. It describes the industry's size, major players, exports, and relationship to GDP. The industry has grown from being dominated by foreign companies to becoming a major domestic and international player. It faces strengths in areas like manufacturing but weaknesses in research and development. Opportunities for growth include increased exports and partnerships with multinational companies. Threats include pressure from patent regulations and drug price controls. The industry is projected to continue strong growth and become a $20 billion market by 2015.

![National Policy [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/nationalpolicyautosaved-230104073215-bbe74e20-thumbnail.jpg?width=640&height=640&fit=bounds)