Downloaded 722 times

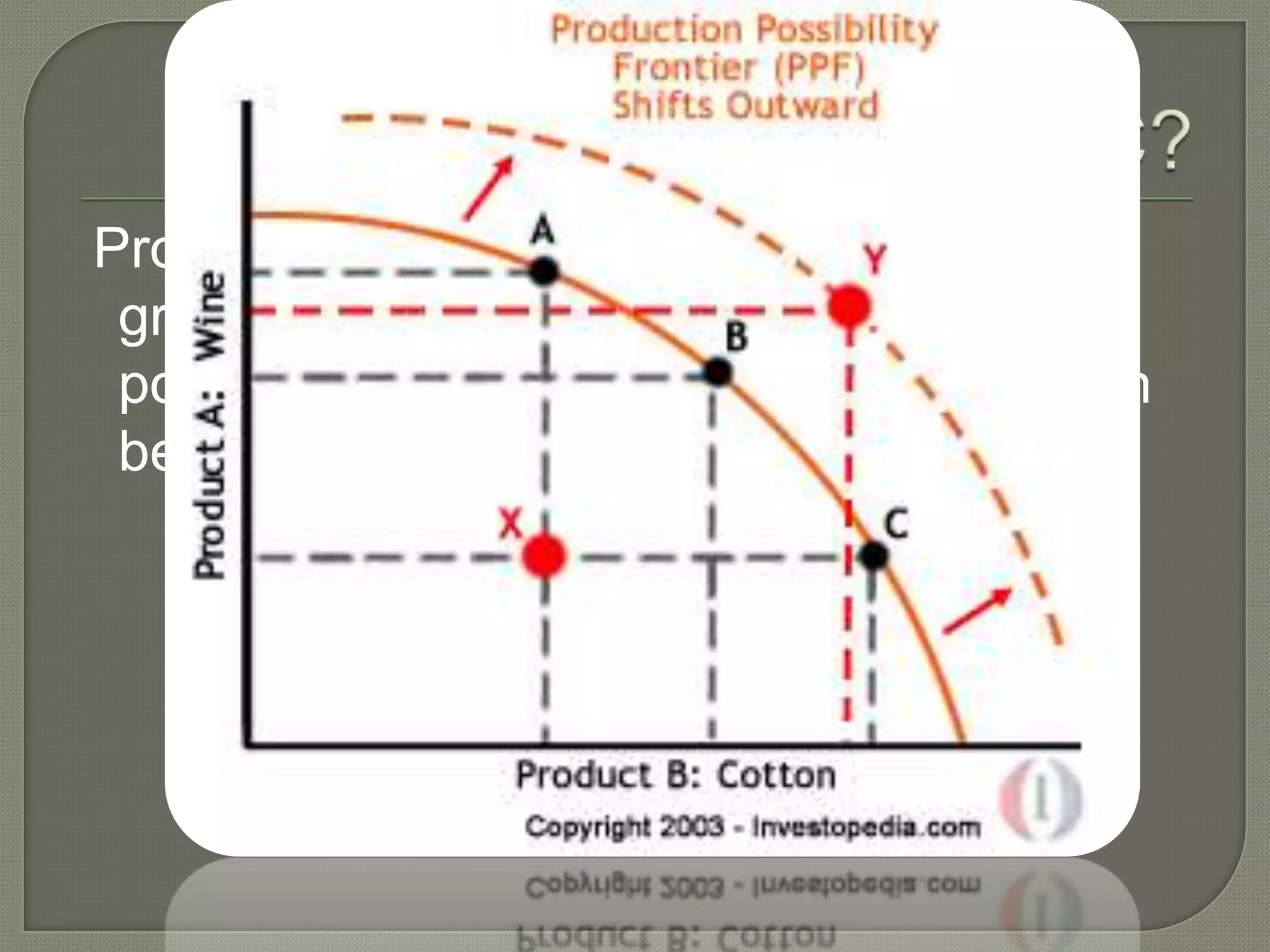

1. Opportunity cost refers to the cost of a decision in terms of the best alternative given up. It is the forgone benefit of the next best alternative when a choice is made. 2. When making choices, whether as consumers, workers, producers, or the government, one must consider opportunity costs and select the option that provides the highest benefit given limited resources. 3. A production possibility curve (PPC) illustrates the maximum quantities of two goods an economy can produce with given resources and technology, and shows the opportunity cost of producing one good in terms of forgone production of the other.

Opportunity Cost involves making choices due to limited resources and the need to give up alternatives.

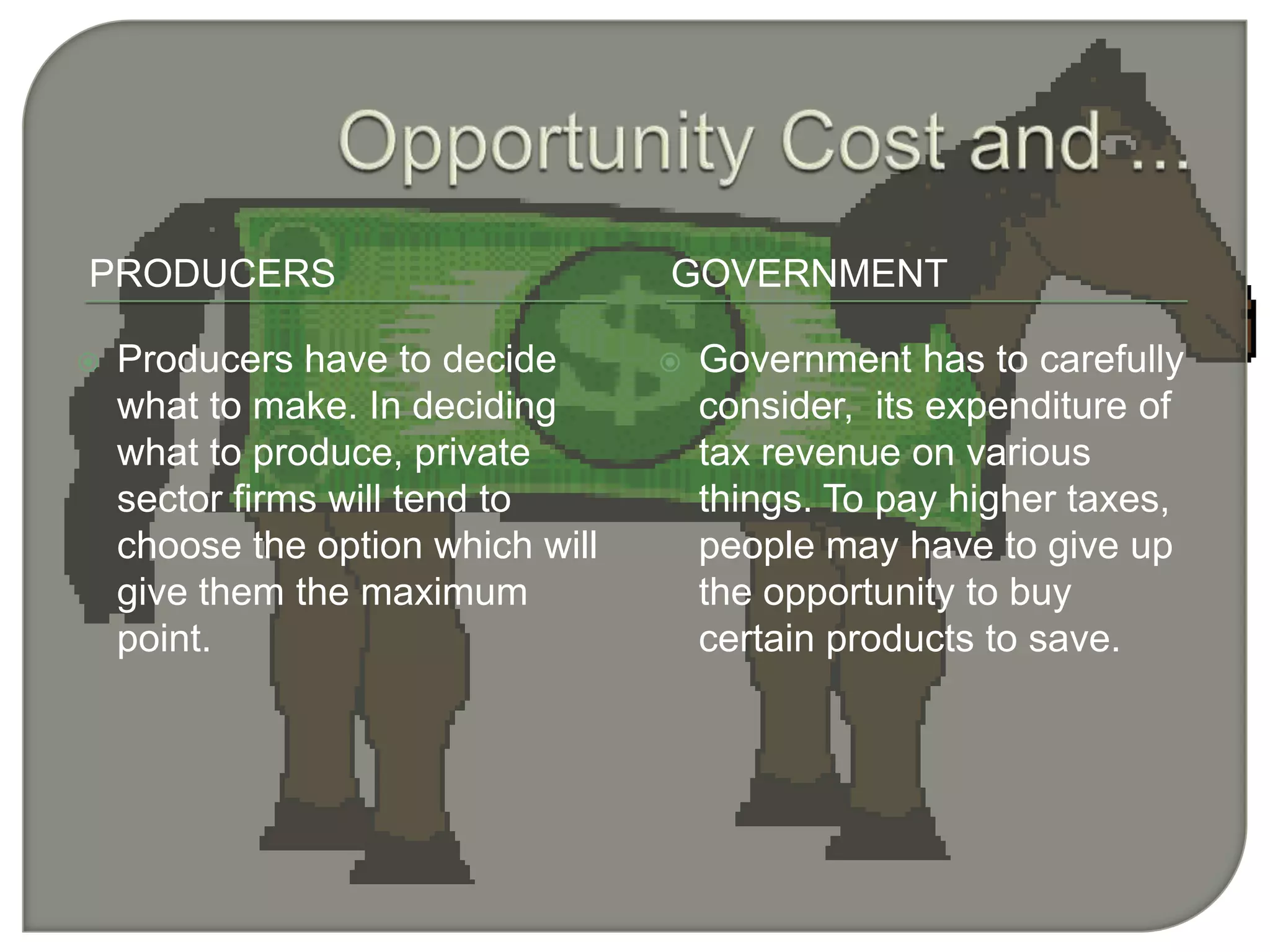

Opportunity Cost applies to consumers and producers, influencing job and production decisions.

Economic goods require resources for production with associated opportunity costs; free goods do not.

A Production Possibility Curve illustrates maximum outputs of two products, demonstrating opportunity costs.

A video segment introducing or explaining Opportunity Cost in depth.