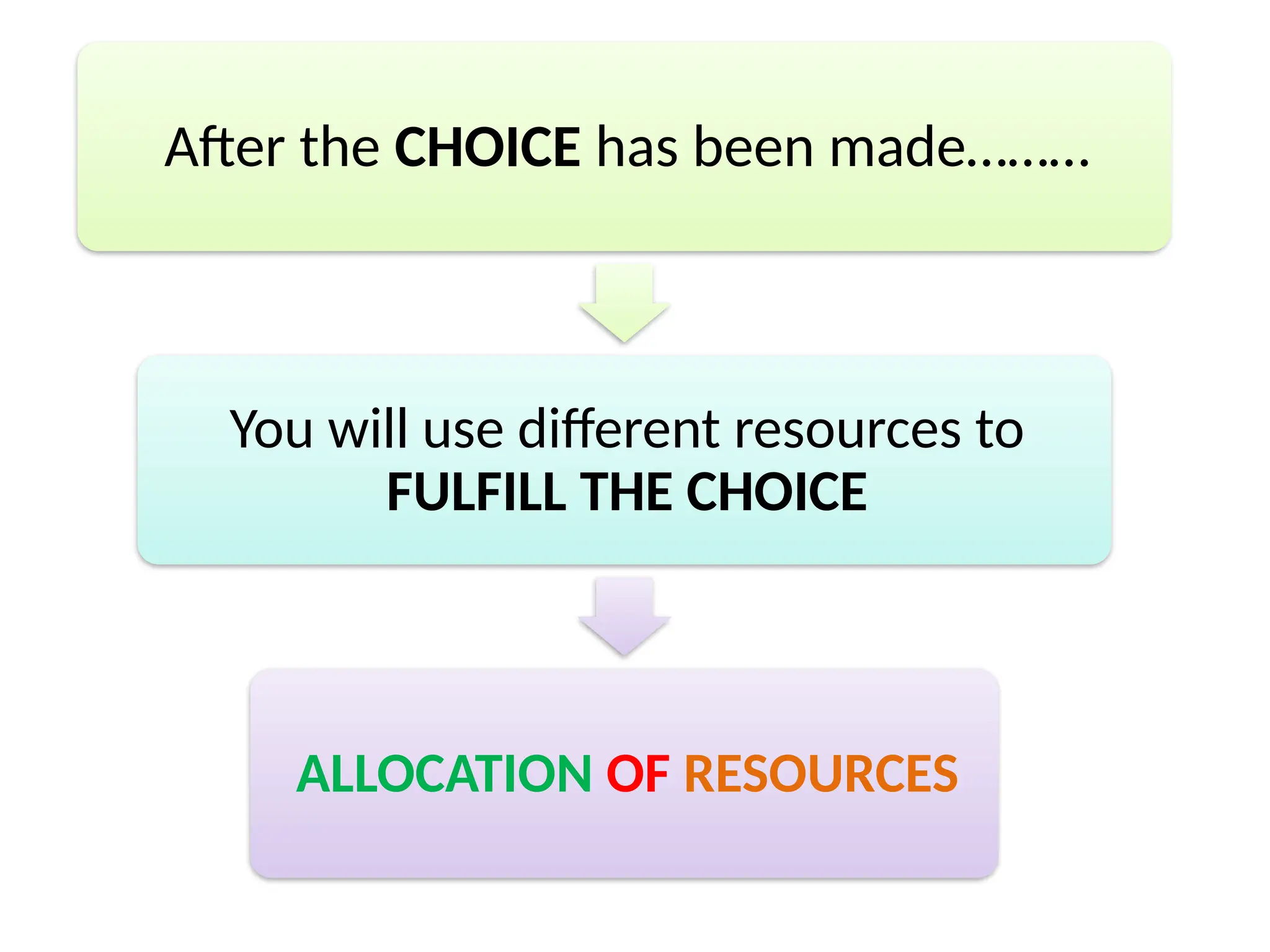

After the CHOICEhas been made………

You will use different resources to

FULFILL THE CHOICE

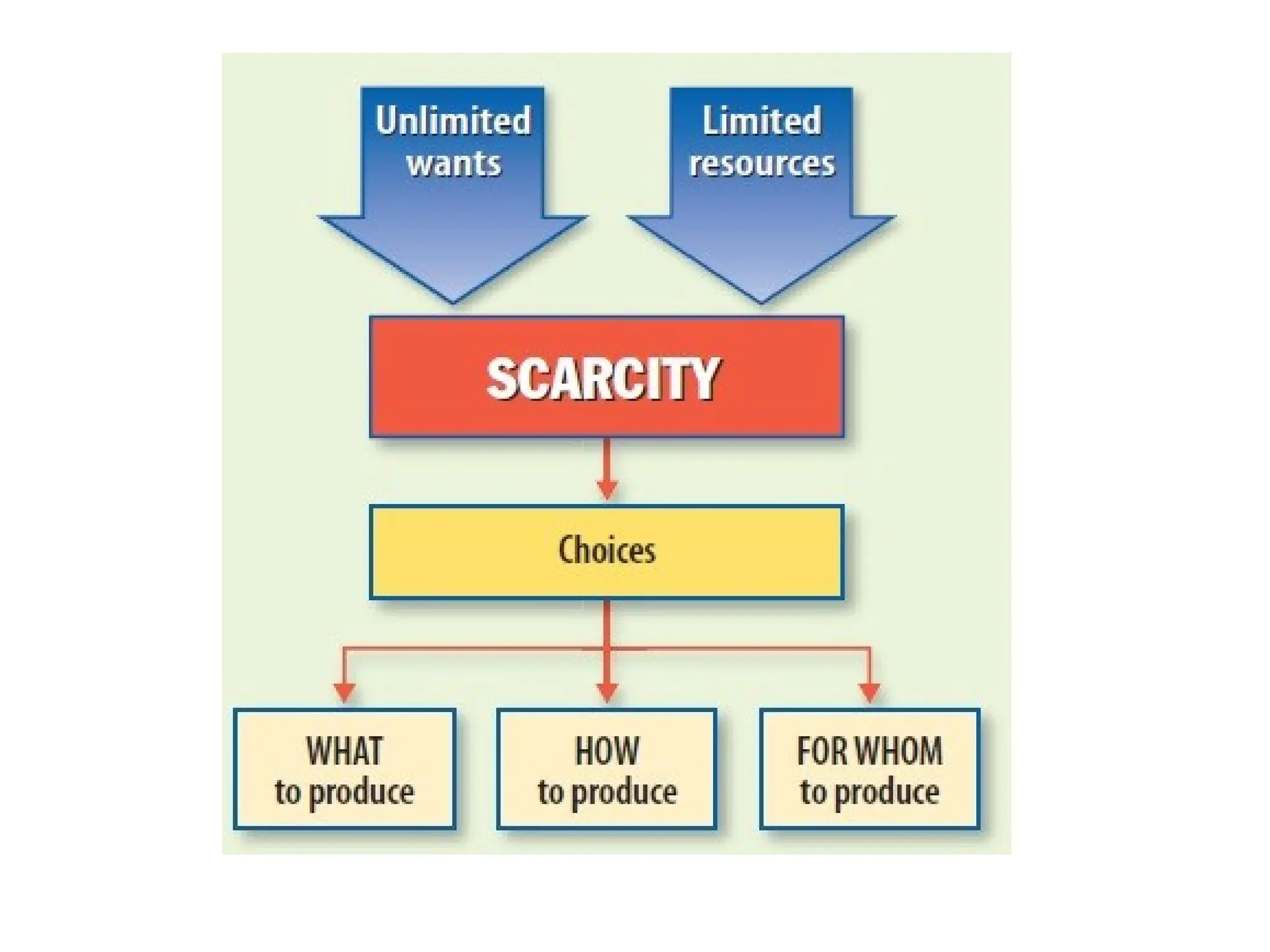

ALLOCATION OF RESOURCES

11.

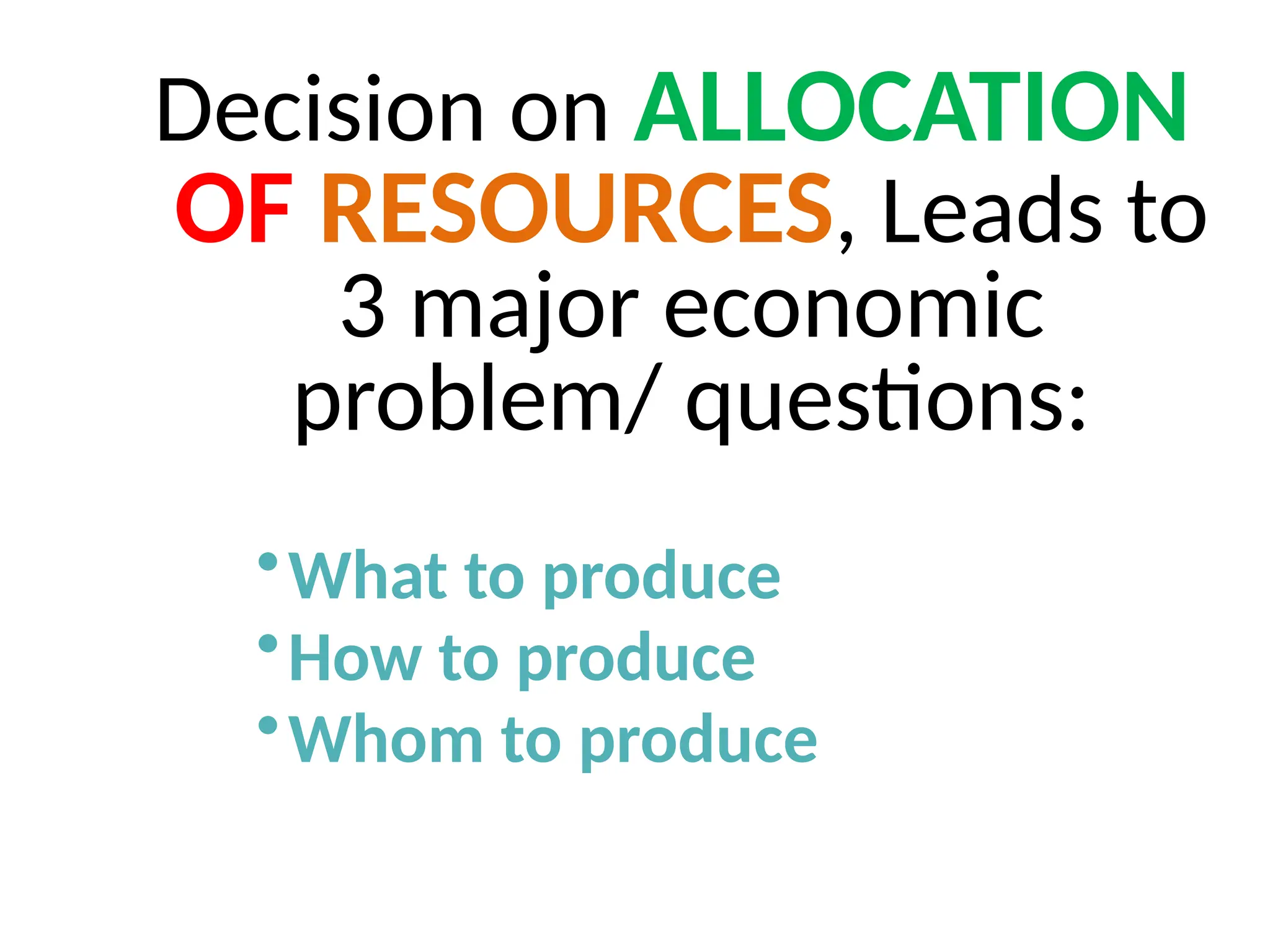

Decision on ALLOCATION

OFRESOURCES, Leads to

3 major economic

problem/ questions:

•What to produce

•How to produce

•Whom to produce

13.

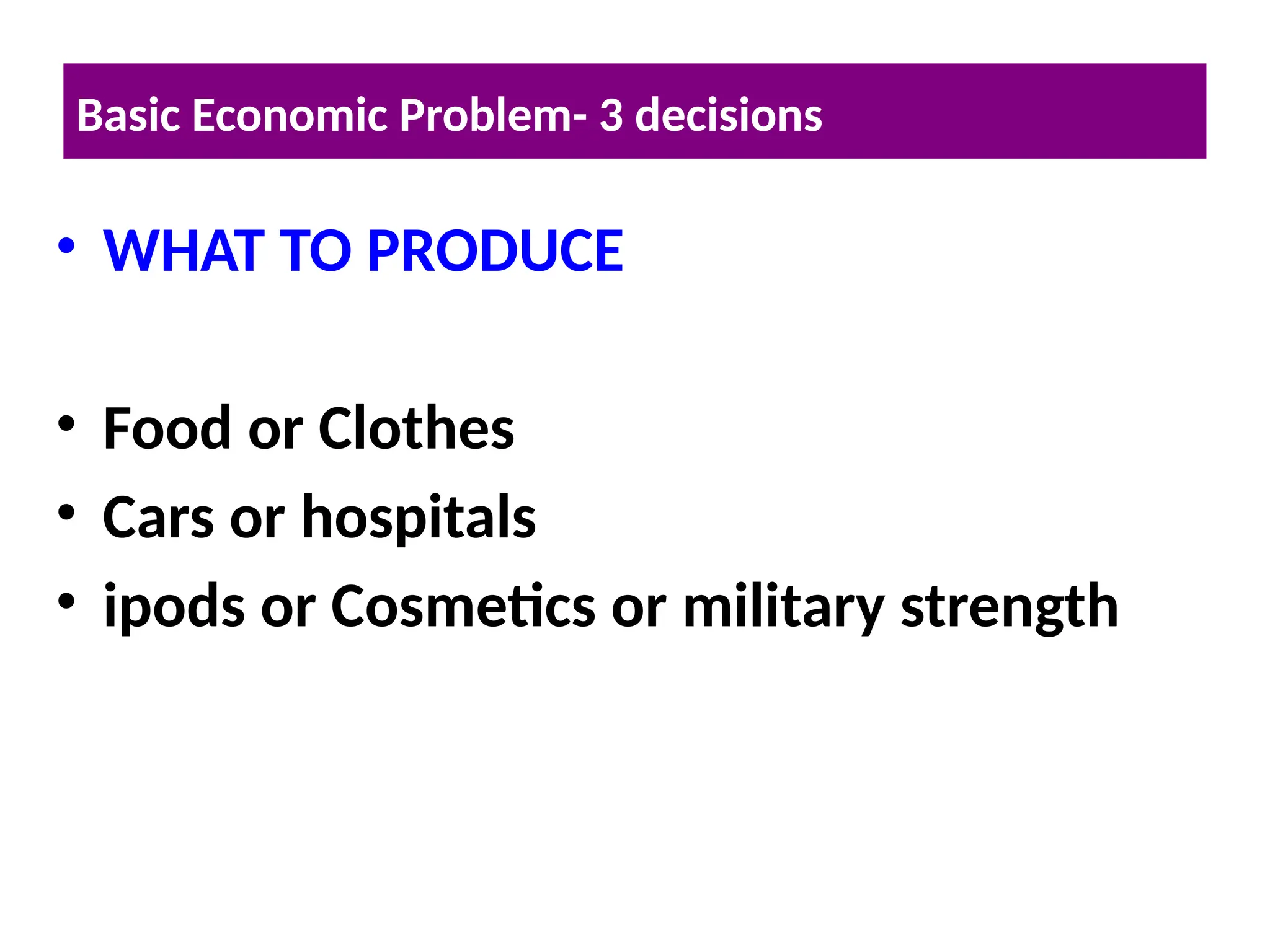

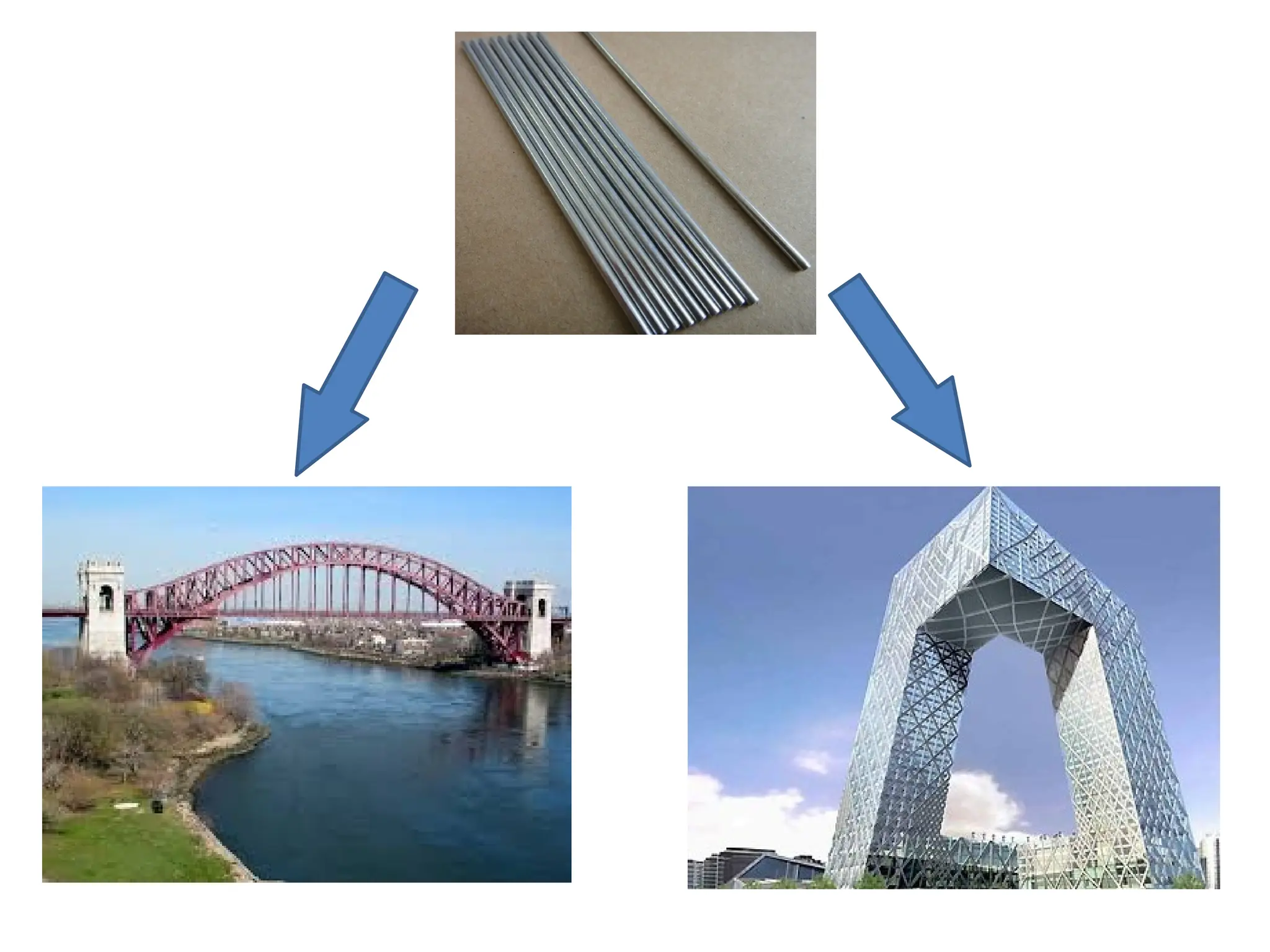

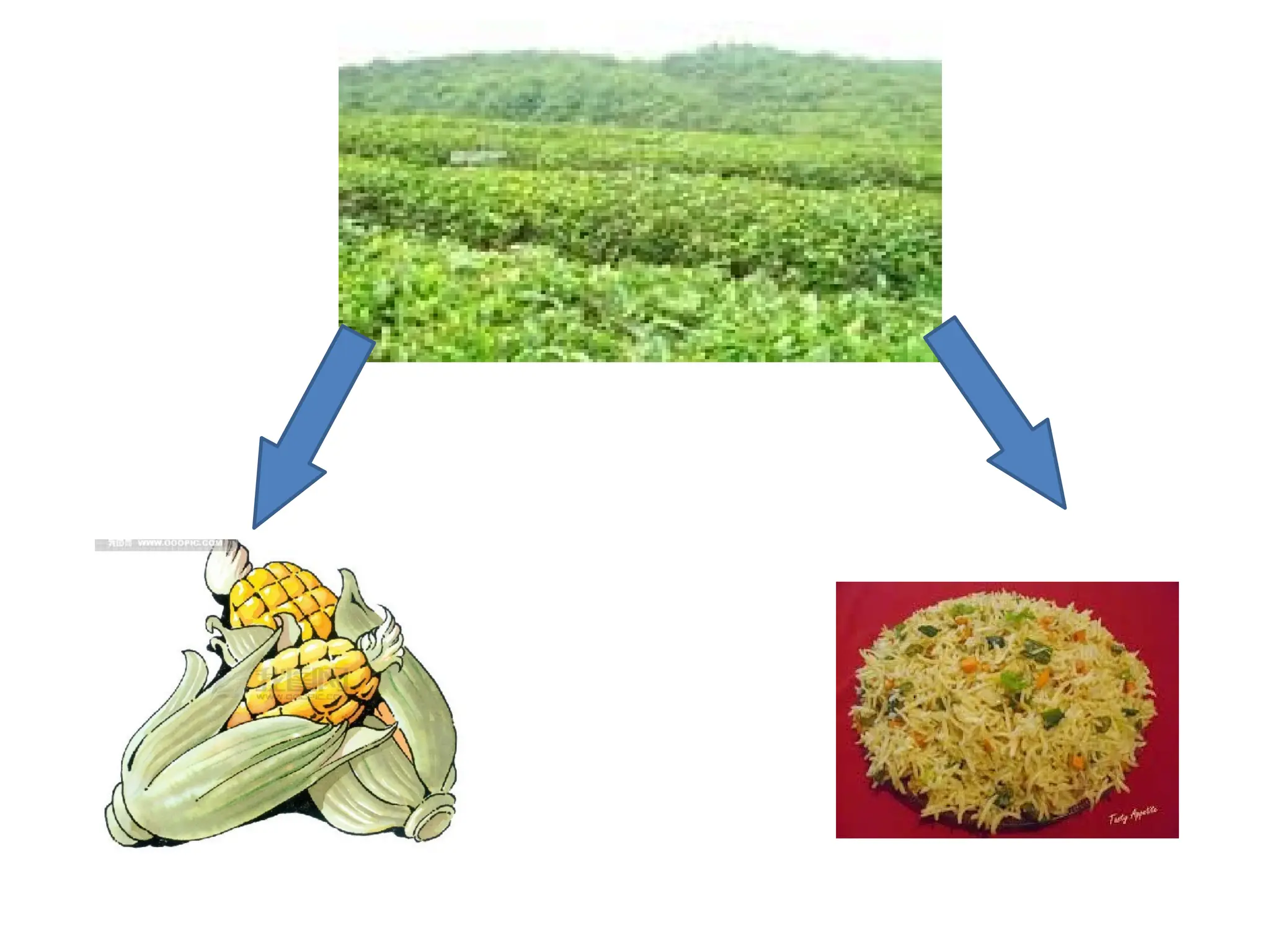

• WHAT TOPRODUCE

• Food or Clothes

• Cars or hospitals

• ipods or Cosmetics or military strength

Basic Economic Problem- 3 decisions

14.

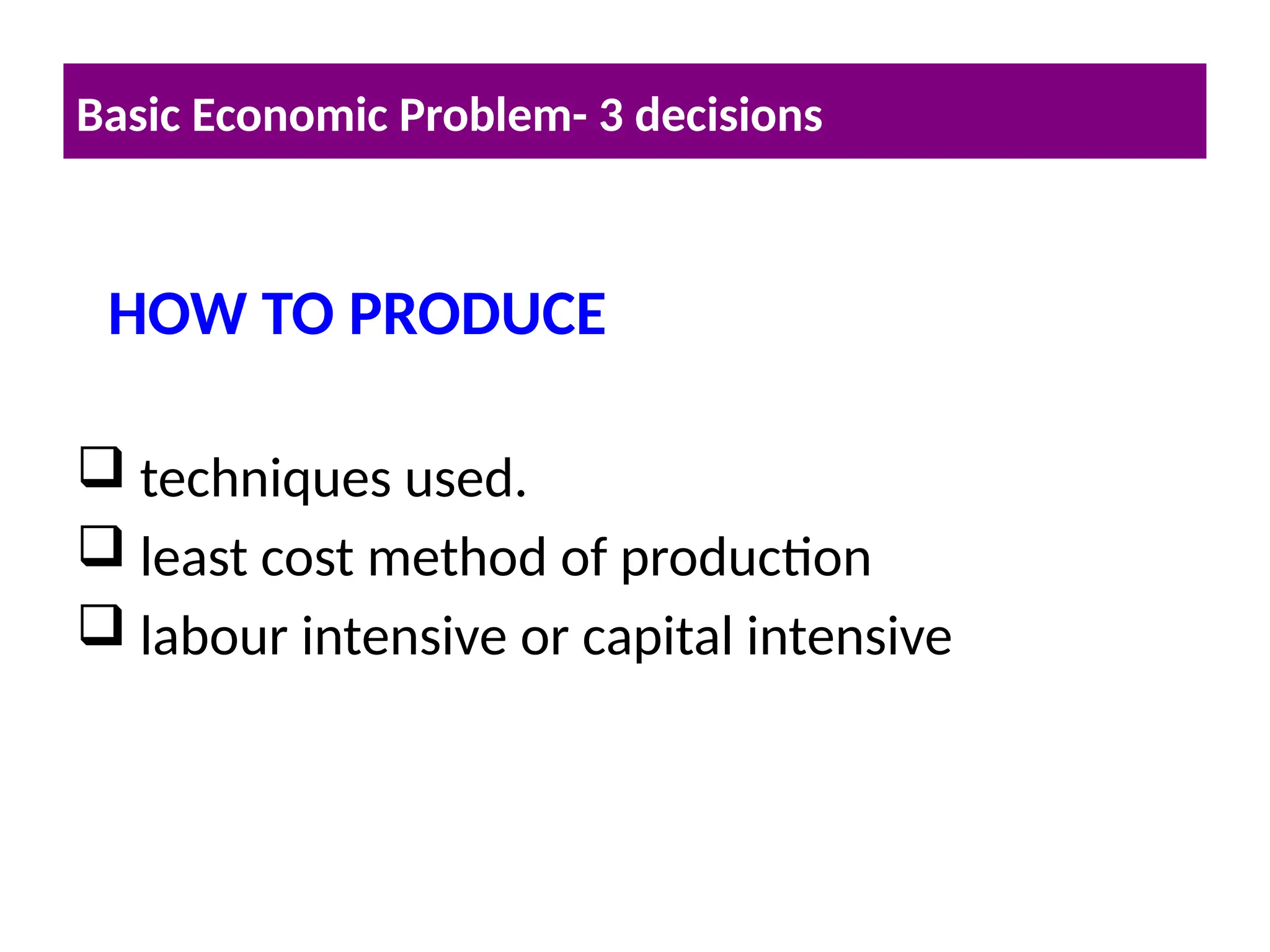

techniques used.

least cost method of production

labour intensive or capital intensive

Basic Economic Problem- 3 decisions

HOW TO PRODUCE

15.

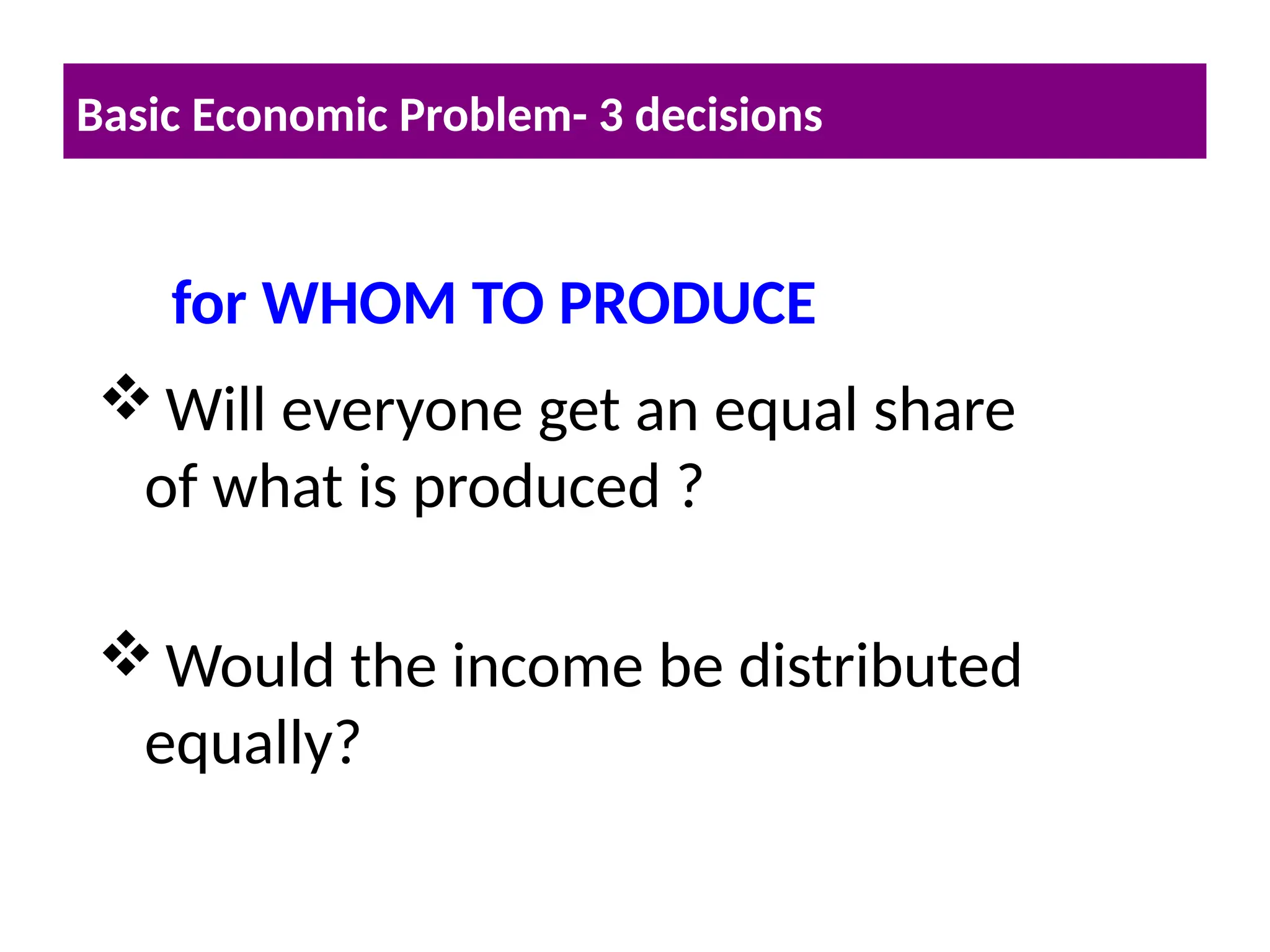

Will everyone getan equal share

of what is produced ?

Would the income be distributed

equally?

Basic Economic Problem- 3 decisions

for WHOM TO PRODUCE

16.

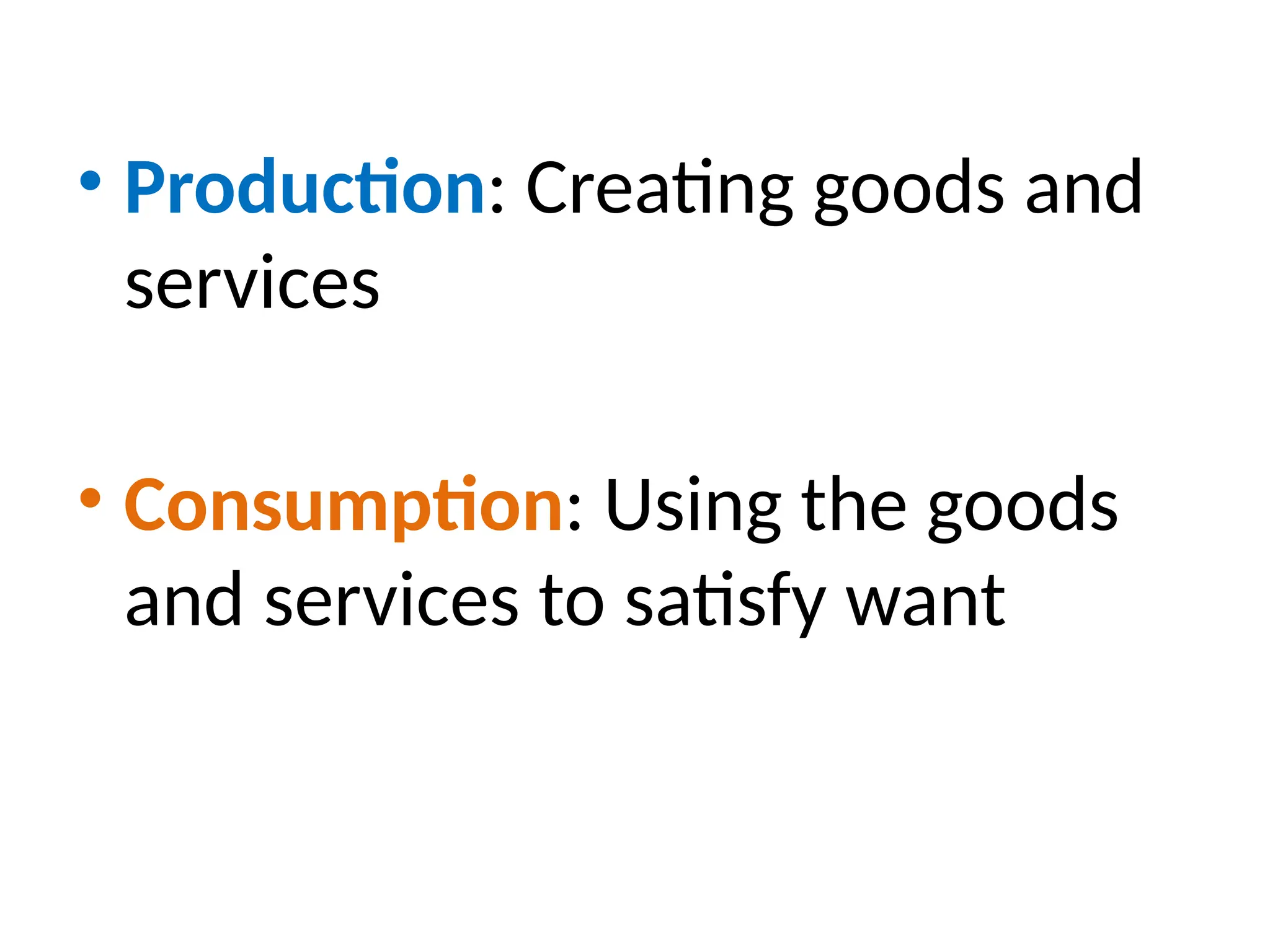

• Production: Creatinggoods and

services

• Consumption: Using the goods

and services to satisfy want

• What youDO NOT CHOOSE is your

Opportunity Cost

• Opportunity Cost is the highest cost forgone

when making the decision

28.

Who has toface this problem

of Opportunity Cost?

• You and me (Individuals)

• Firms (Business)

• Government

29.

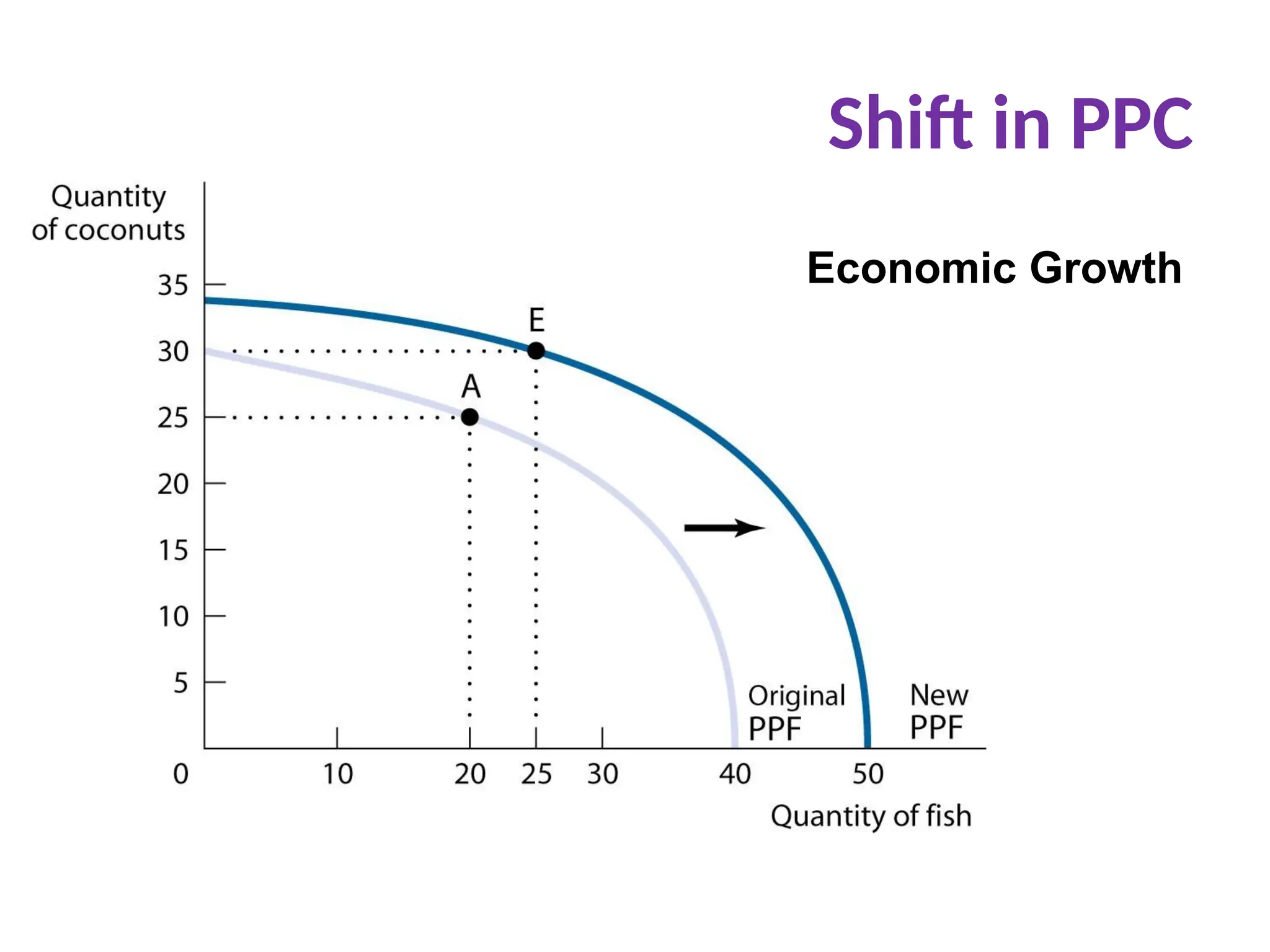

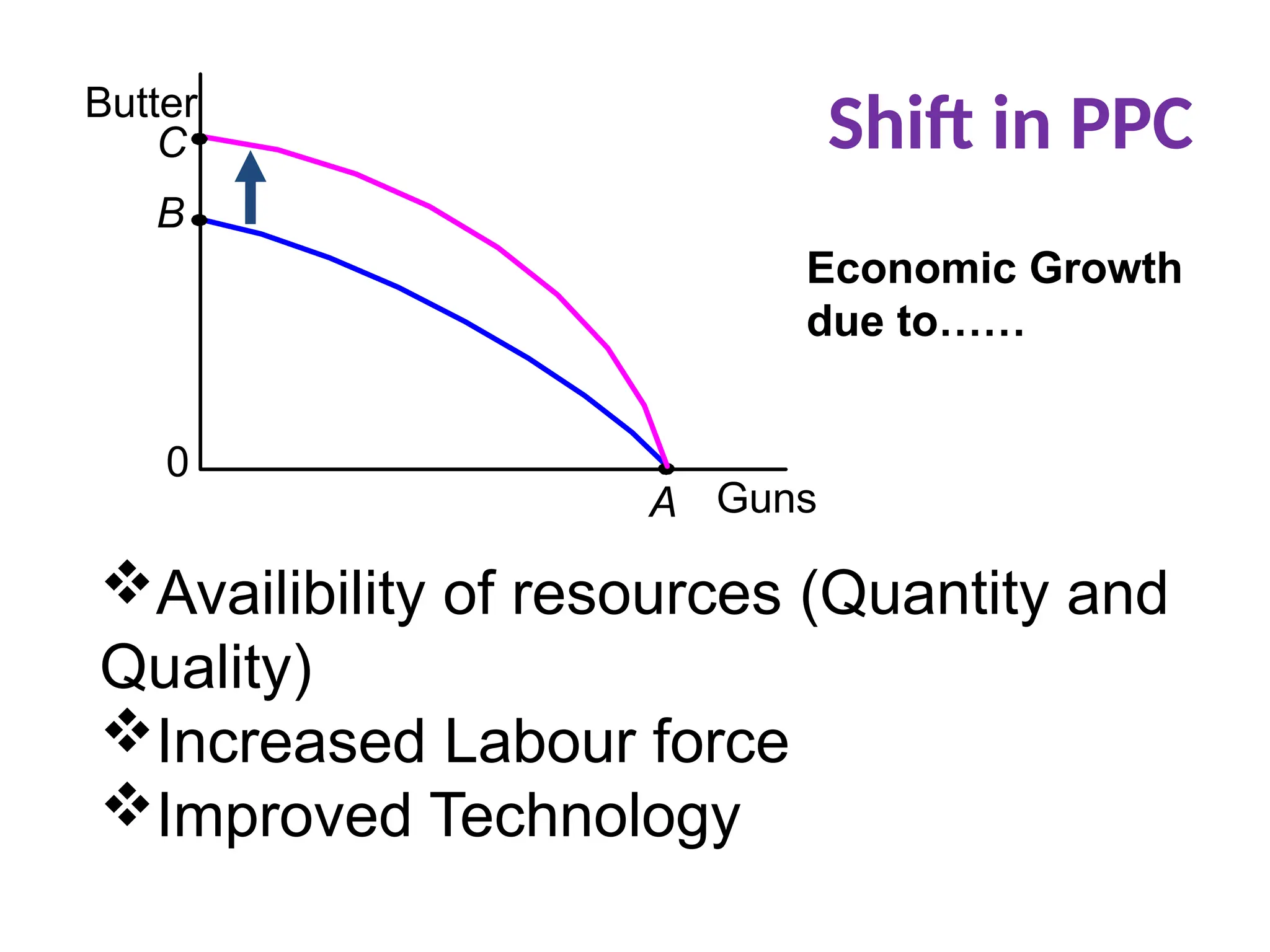

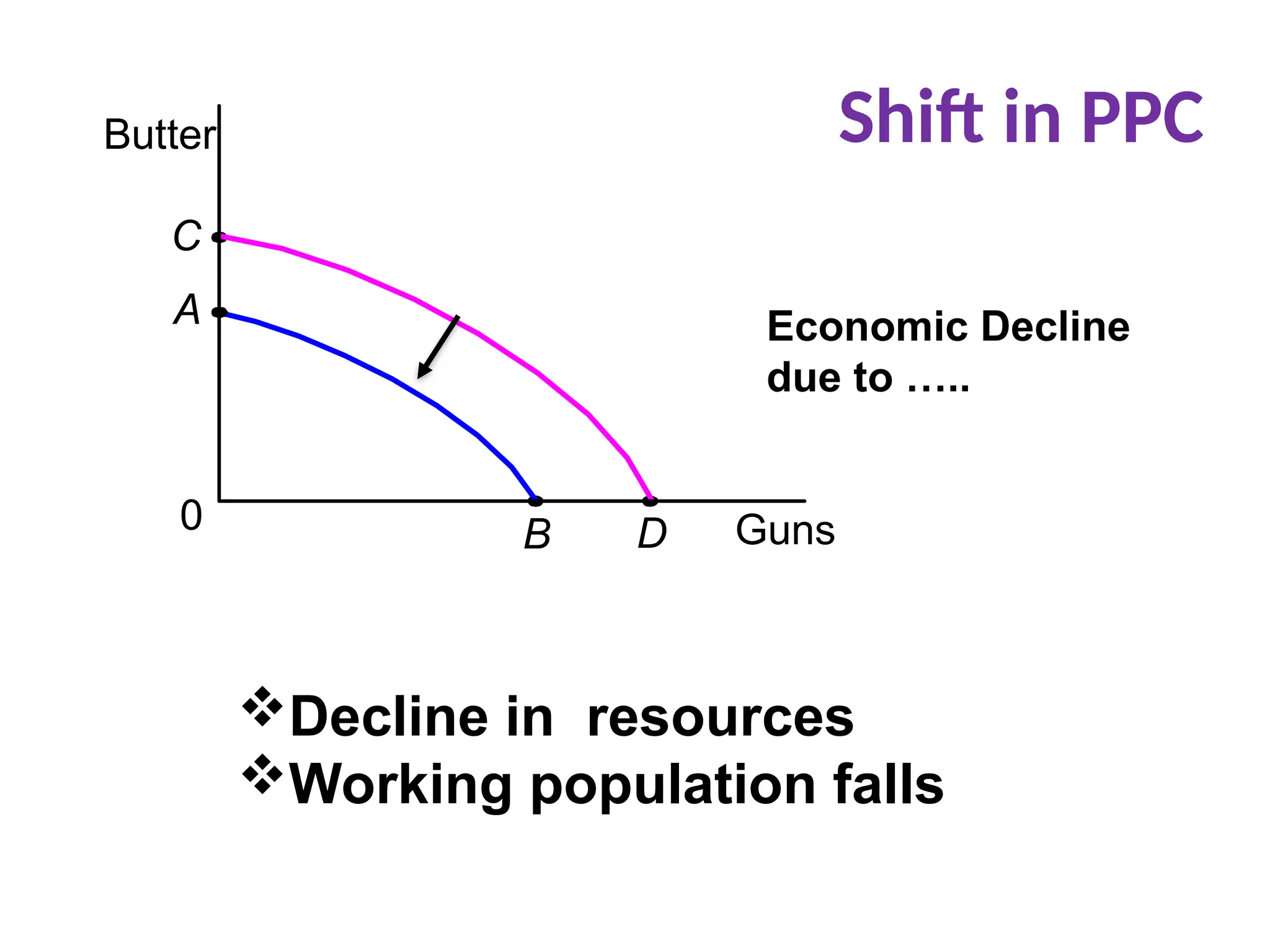

Production Possibility Curve(PPC)

• Every decision/choice we make has

an Opportunity Cost

• This idea of Opportunity Cost can be

illustrated using a PPC

30.

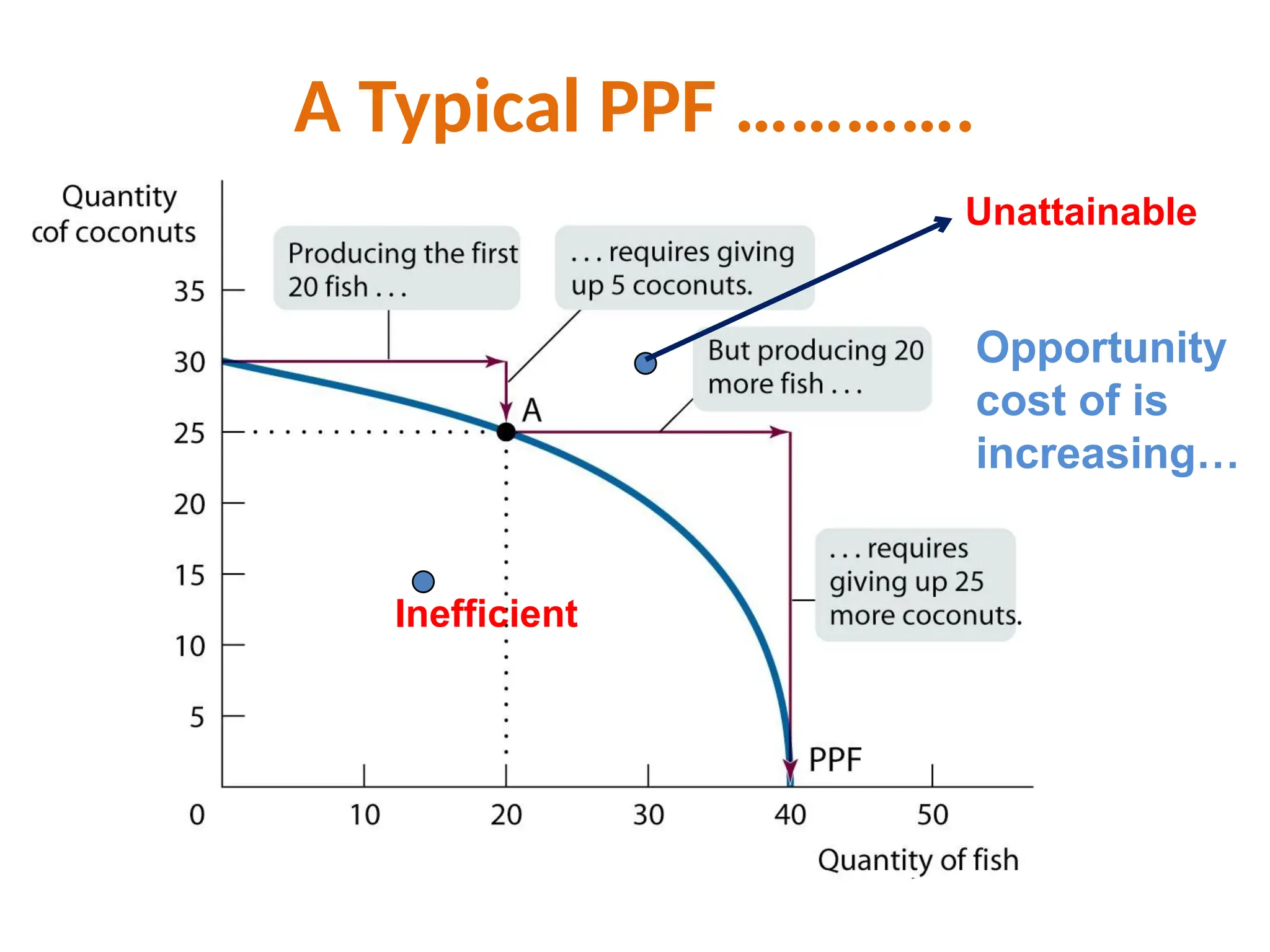

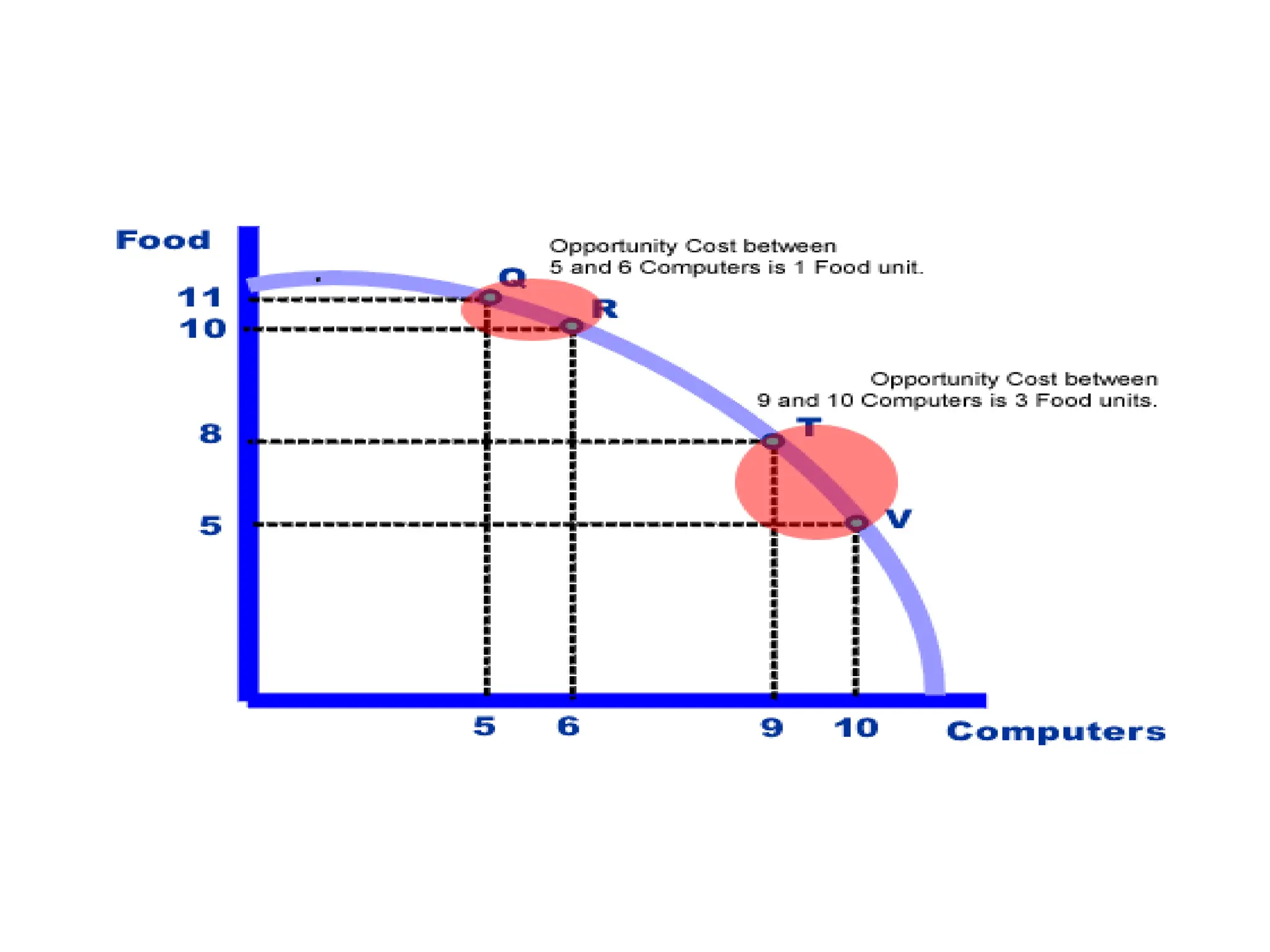

A Typical PPF………….

Unattainable

Inefficient

Opportunity

cost of is

increasing…

31.

• Production Possibilitycurve (PPC) shows the

maximum combinations of goods and

services that can be produced by an

economy in a given time period with its

limited resources

• A point outside the graph is unachievable

and a point inside the graph is inefficient

32.

PPC also tellsyou:

• What you can and cannot produce

• What is the cost of producing the

other good

33.

Depending on ourchoices of Production,

the opportunity cost may

Remain Constant

Increase

Decrease

35.

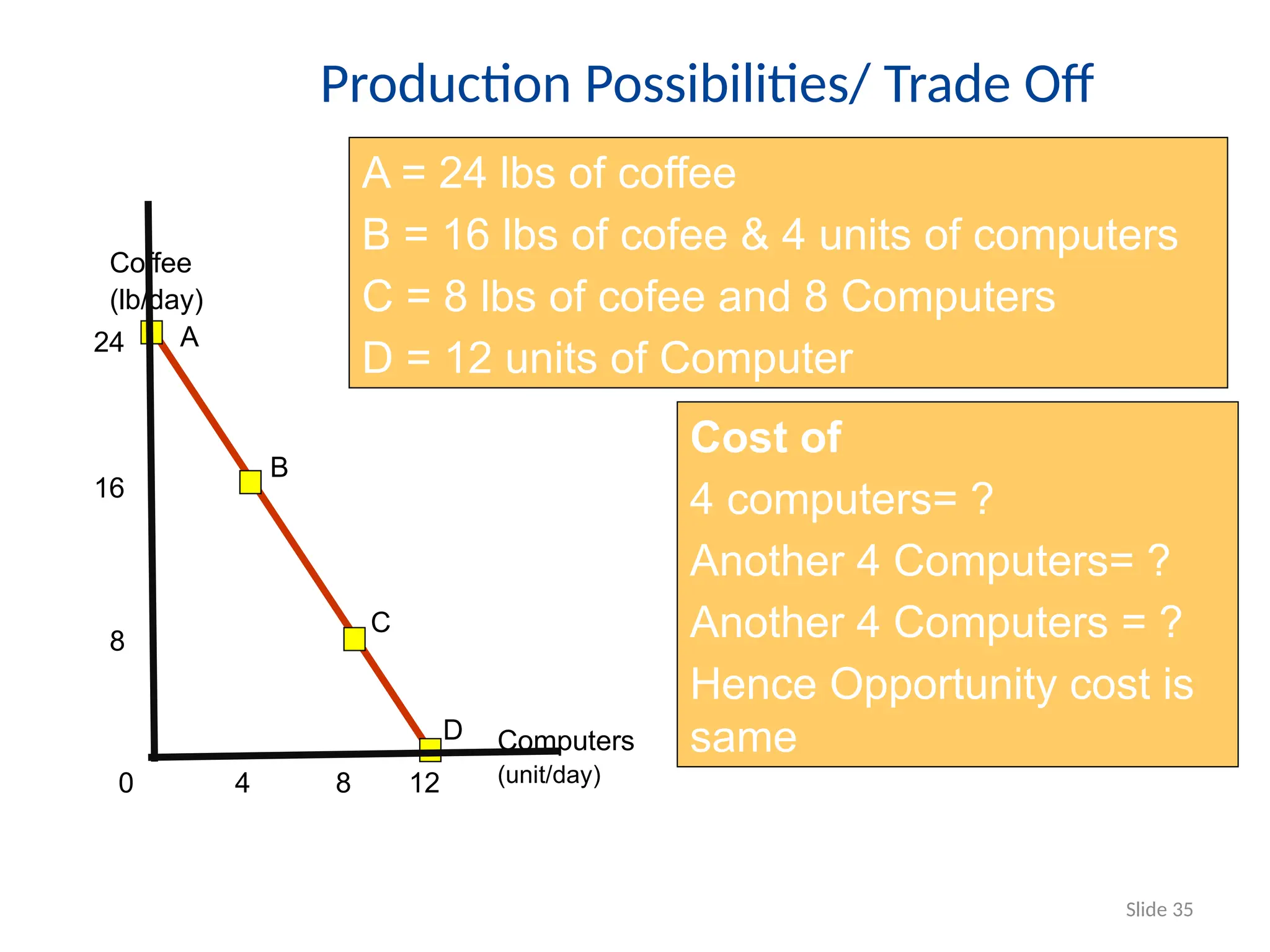

Production Possibilities/ TradeOff

Slide 35

A = 24 lbs of coffee

B = 16 lbs of cofee & 4 units of computers

C = 8 lbs of cofee and 8 Computers

D = 12 units of Computer

Coffee

(lb/day)

Computers

(unit/day)

A

B

C

D

24

0

16

8

4 8 12

Cost of

4 computers= ?

Another 4 Computers= ?

Another 4 Computers = ?

Hence Opportunity cost is

same

36.

Unit 1 :Macroeconomics

National Council on Economic

Education

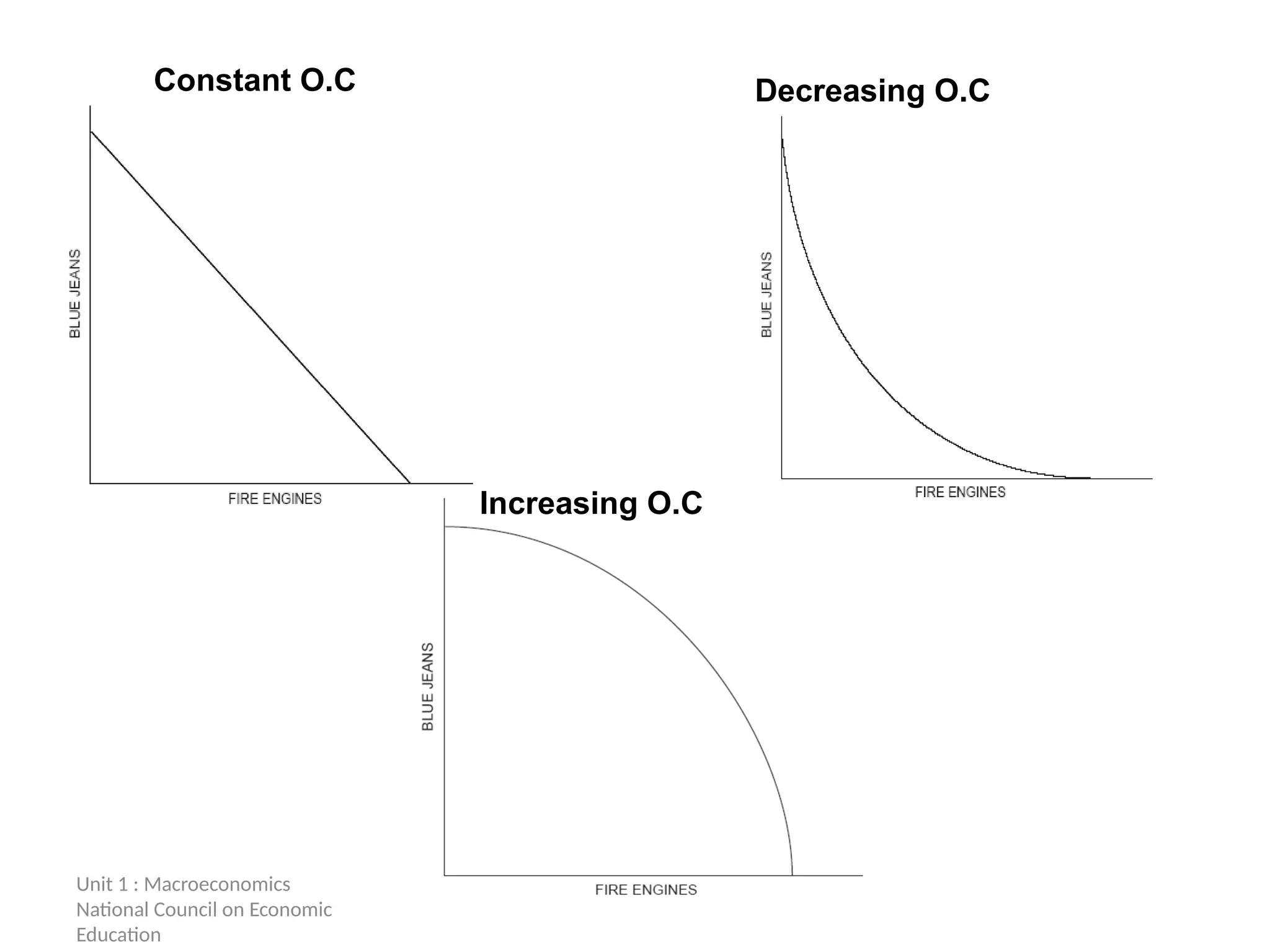

Constant O.C Decreasing O.C

Increasing O.C

37.

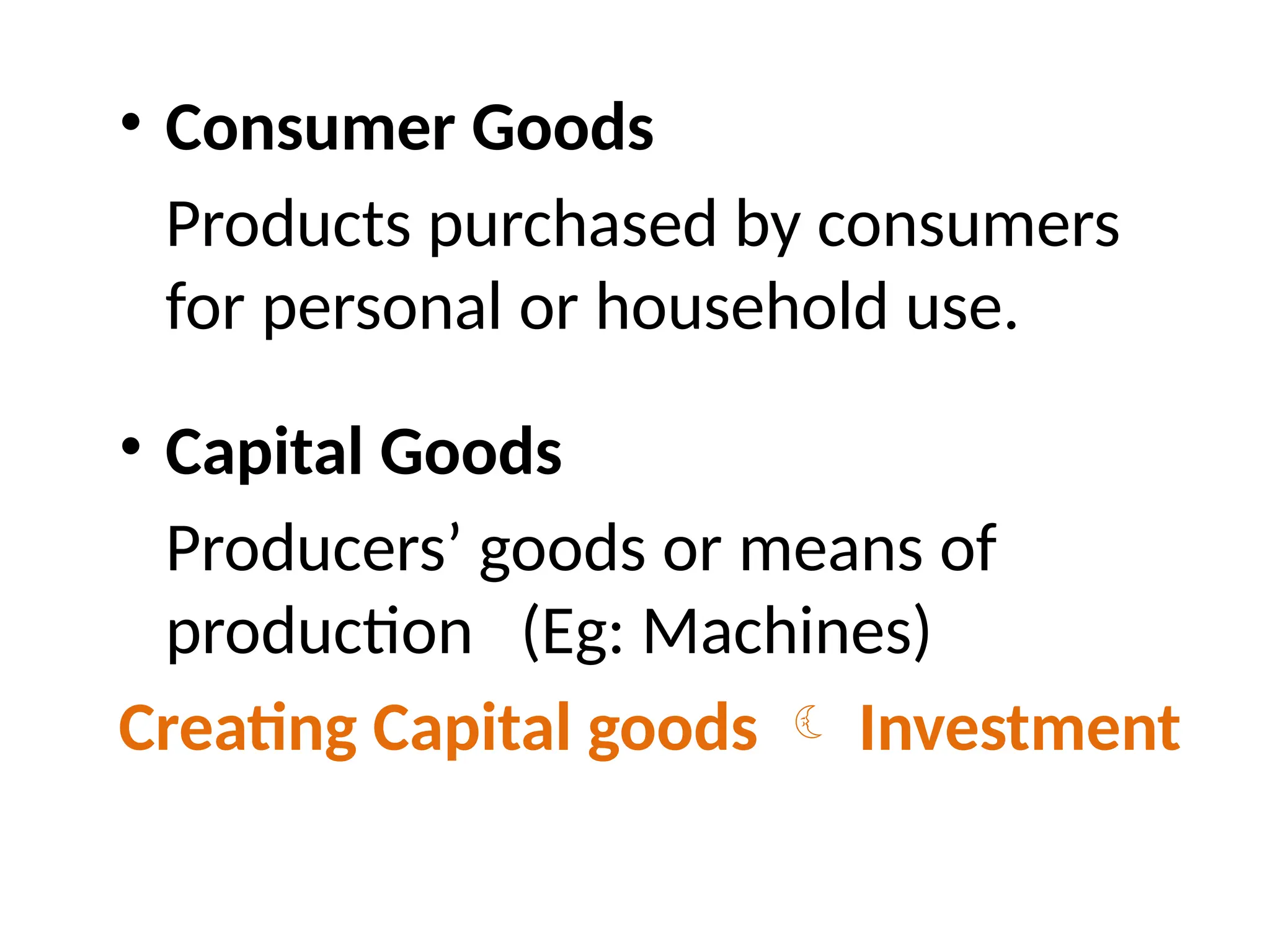

• Consumer Goods

Productspurchased by consumers

for personal or household use.

• Capital Goods

Producers’ goods or means of

production (Eg: Machines)

Creating Capital goods Investment