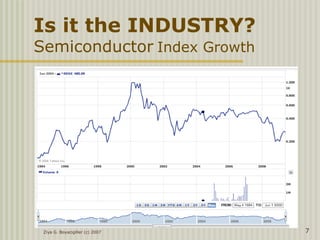

Downloaded 45 times

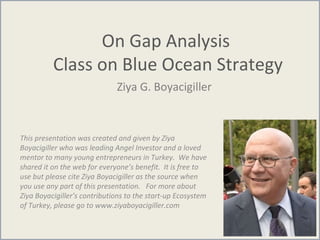

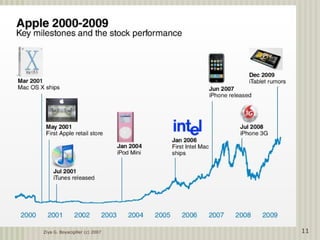

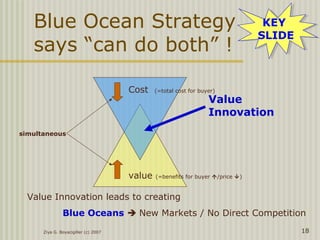

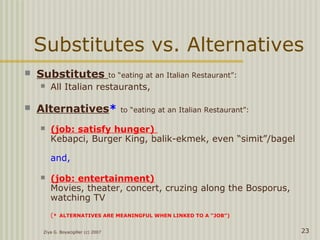

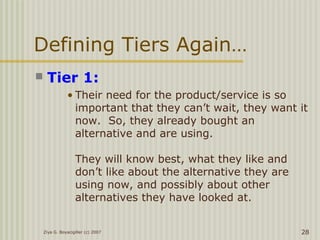

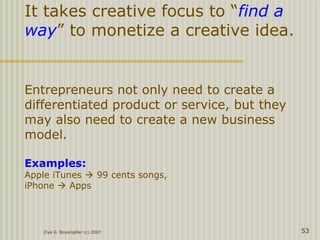

![Ziya G. Boyacigiller (c) 2007 35

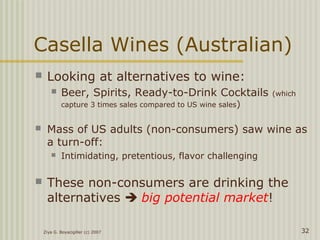

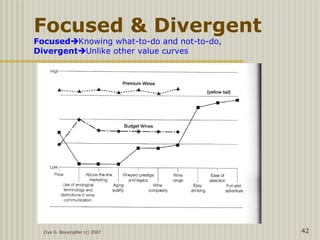

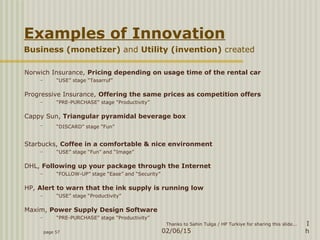

[yellow tail]

•Fun, social drink accessible to nonwine

drinkers

•Fastest growing brand in the histories of

both Australian and US wine industries

•#1 imported wine into USA, surpassing

wines of France, Italy

•#1 red wine in 750ml bottle in USA,

surpassing California labels

•Sales in about 2 years hit over 4.5million

cases

•While competing with 1,600 wineries in the

USA !](https://image.slidesharecdn.com/new4bosblueoceanstrategy-150602132955-lva1-app6891/85/New4-bos-blue-ocean-strategy-35-320.jpg)

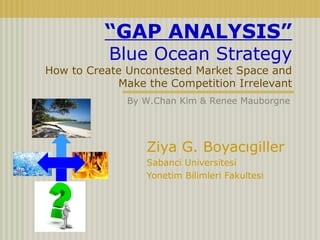

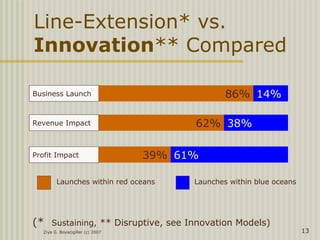

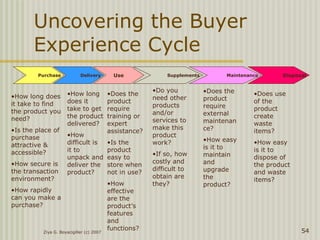

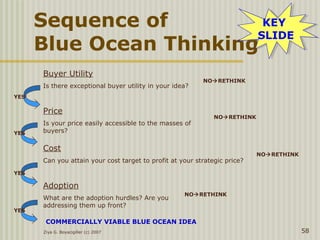

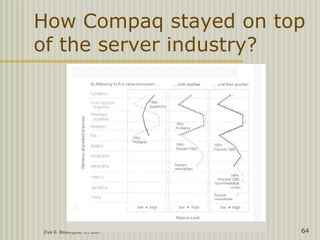

![Ziya G. Boyacigiller (c) 2007 37

Strategy Canvas of

[yellow tail]](https://image.slidesharecdn.com/new4bosblueoceanstrategy-150602132955-lva1-app6891/85/New4-bos-blue-ocean-strategy-37-320.jpg)

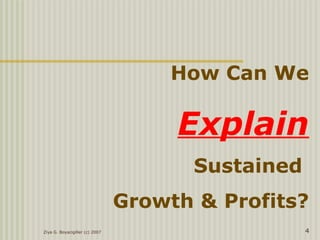

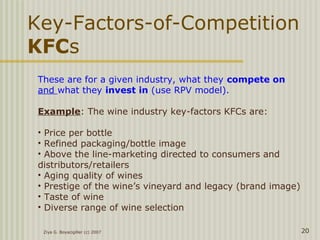

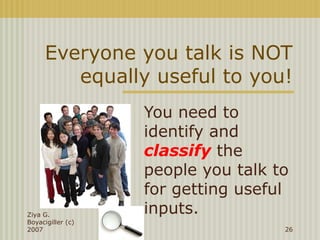

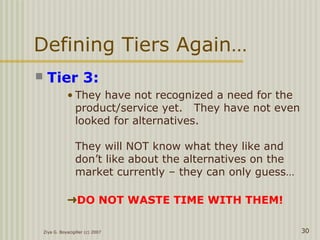

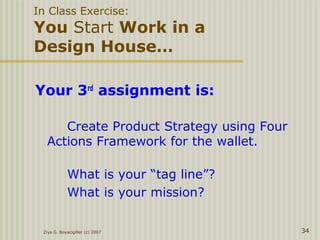

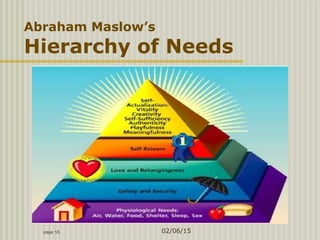

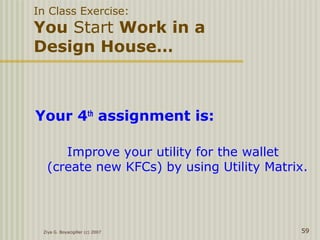

![Ziya G. Boyacigiller (c) 2007 38

Focus on

alternatives & noncustomers

others [yellow tail]

Easy

drinking

Wine’s complicated taste

is difficult to appreciate

compared to alternatives

[yellow tail] is soft in taste,

with pronounced fruit flavors

(easy drinking wine that

doesn’t need developed

appreciation over time)

Ease of

selection

Isles of wine in markets

overwhelmed and

intimidated customers

Only 2 to choose from (one

white/one red (used same

bottle design for both to

reduce cost)

Fun and

adventure

Elite image did not

resonate with general

public

Australian theme, unusual

label, no mention of vineyard

or other intimidating wine

vocabulary](https://image.slidesharecdn.com/new4bosblueoceanstrategy-150602132955-lva1-app6891/85/New4-bos-blue-ocean-strategy-38-320.jpg)

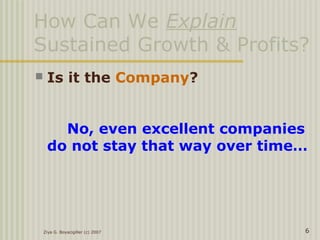

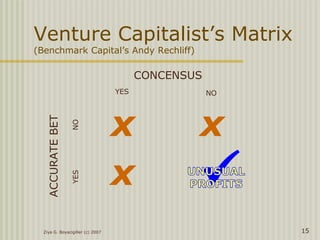

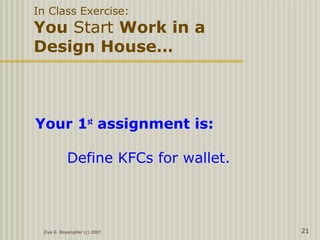

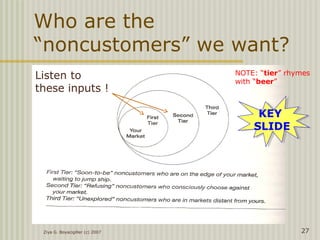

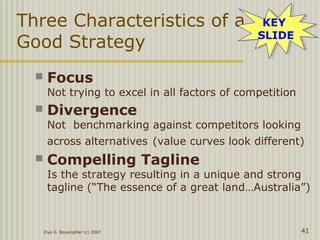

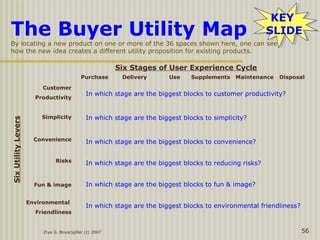

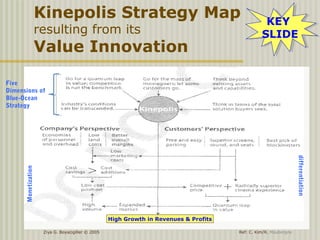

![Ziya G. Boyacigiller (c) 2007 39

Eliminate-Reduce-Raise-Create

Grid for [yellow tail]

Eliminate

Enological terminology and

distinctions

Aging qualities

Above-the-line marketing

Raise

Price compared to budget

wines

Retail store support and

involvement

Reduce

Wine complexity

Wine range (variety)

Vineyard prestige

Create

Easy drinking

Ease of selection

Fun and adventure (new

delightful experience)

KEY

SLIDE

KEY

SLIDE](https://image.slidesharecdn.com/new4bosblueoceanstrategy-150602132955-lva1-app6891/85/New4-bos-blue-ocean-strategy-39-320.jpg)

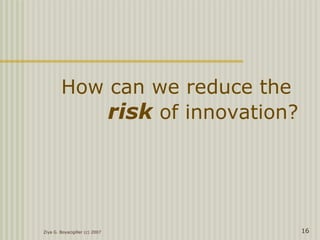

![Ziya G. Boyacigiller (c) 2007 40

I have to apologize, that I just tried a different boxed

California cabernet, which tasted like a bad children's

fruit drink. I have learned my lesson and will stick to

yellow tail merlot! And I must say that I love yellow

tail, because my wife loves yellow tail.

I was never a wine drinker until I was introduced to

Yellow Tail Chardonnay 3 years ago at a dinner party. I

was immediately hooked! Now, there's nothing I look

forward to more than coming home from work on a

Friday night and pouring myself a glass of Yellow Tail

to unwind. It's a standard at parties that I attend and it's

always a welcome gift. Thanks for a wonderful product

and keep up the good work! Is it Friday yet?

What customers are saying…

[yellow tales] from Casella web site](https://image.slidesharecdn.com/new4bosblueoceanstrategy-150602132955-lva1-app6891/85/New4-bos-blue-ocean-strategy-40-320.jpg)

This document summarizes a presentation by Ziya Boyacigiller on blue ocean strategy and gap analysis. It discusses how some companies achieve sustained growth through strategic moves that open new market space rather than competing based on existing industry factors. It introduces the concepts of red and blue oceans, and analyzing alternatives and non-customers to identify opportunities. Key frameworks discussed include the strategy canvas, four actions framework, and visualizing strategy in four steps to develop a "blue ocean" strategy focused on creating value for buyers rather than competing.

![The Times, They Are Changing May 15 Naed [Autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/thetimestheyarechangingmay15naedautosaved-12735050512432-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)