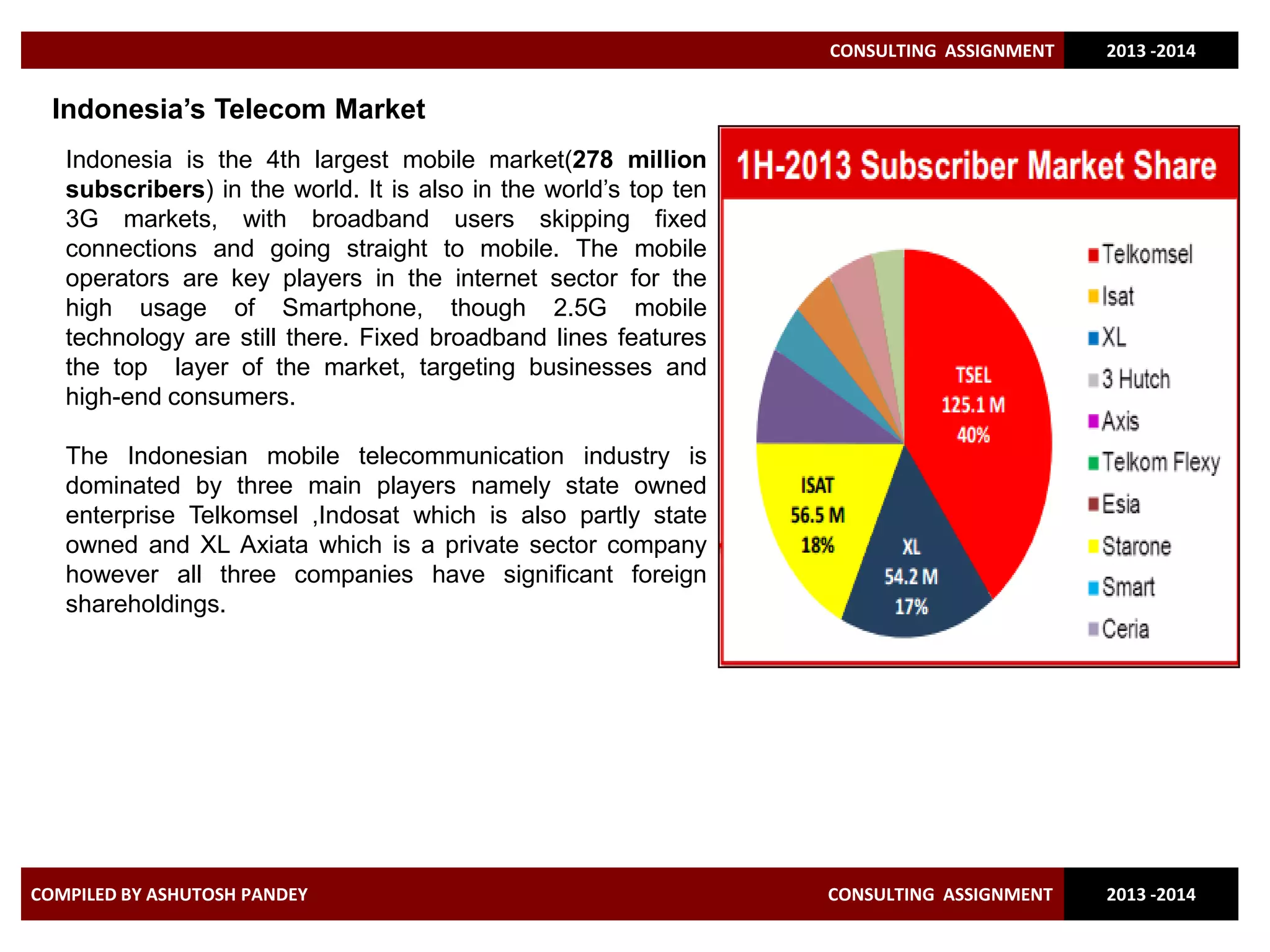

Indonesia has the 4th largest mobile market in the world with 278 million subscribers. It also has a large 3G market, with many users skipping fixed broadband for mobile. The mobile operators Telkomsel, Indosat, and XL Axiata dominate the market, though they have significant foreign ownership. Mobile internet usage is growing rapidly, with internet users expected to more than quadruple by 2016, driven primarily by smartphones and mobile data usage. The telecommunications industry provides many opportunities around enterprise services, e-commerce, digital advertising, and increasing data consumption.