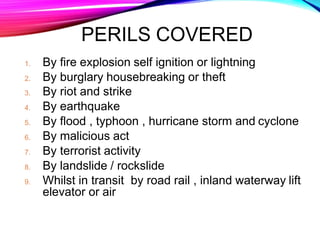

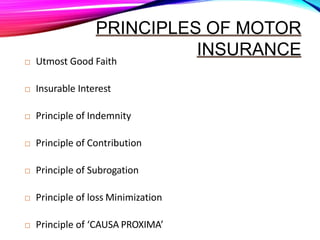

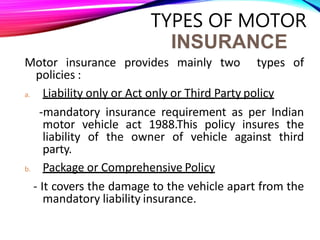

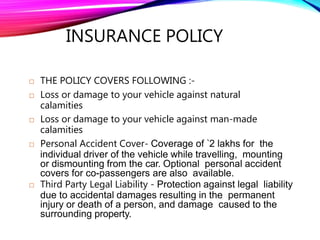

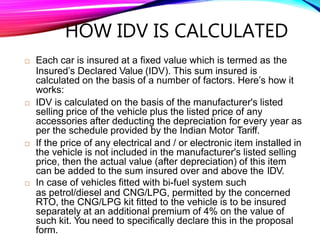

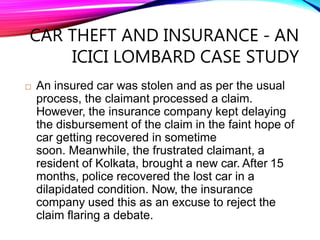

Motor insurance provides protection against physical damage and liability arising from traffic accidents. It is mandatory in India for all vehicles to be insured. This document discusses the different types of motor vehicles, perils covered, exclusions, principles of insurance, factors affecting premium, types of motor insurance policies including liability-only and comprehensive, and claim processes. It provides examples of a car insurance policy and how insured declared value is calculated. It also discusses a case study regarding an insured vehicle that was stolen and the insurance company's rejection of the claim.