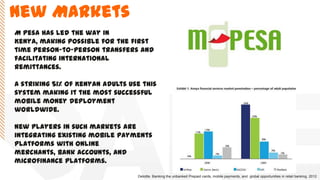

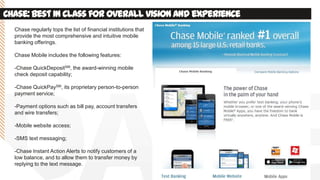

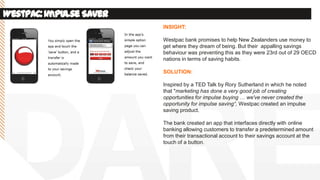

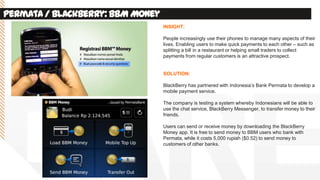

The document discusses the rise of mobile banking and how it has transformed consumer behavior, with bank visits dropping significantly from 1995 to 2012. It emphasizes the importance of mobile services, innovations, and convenience as key drivers for customer retention and satisfaction in financial services. Various case studies illustrate successful mobile banking strategies and platforms that cater to both banked and unbanked populations, highlighting the dynamic landscape of digital commerce.

![A variety of new players are

entering the

market, including tech

specialists such as

Google, start-ups such as

Square, and established

online payment providers

such as PayPal.

Google in particular has bold

plans: It wants to close the

last mile and is willing to

give away everything to

merchants (including point-of-

sale terminals, digital

wallets, and Trusted Service

Manager [TSM] services) to

make this happen.

Digital commerce](https://image.slidesharecdn.com/mobileandfinancialservices-np-130708155537-phpapp02/85/Opportunities-for-disruption-in-Financial-Services-with-a-mobile-focus-13-320.jpg)