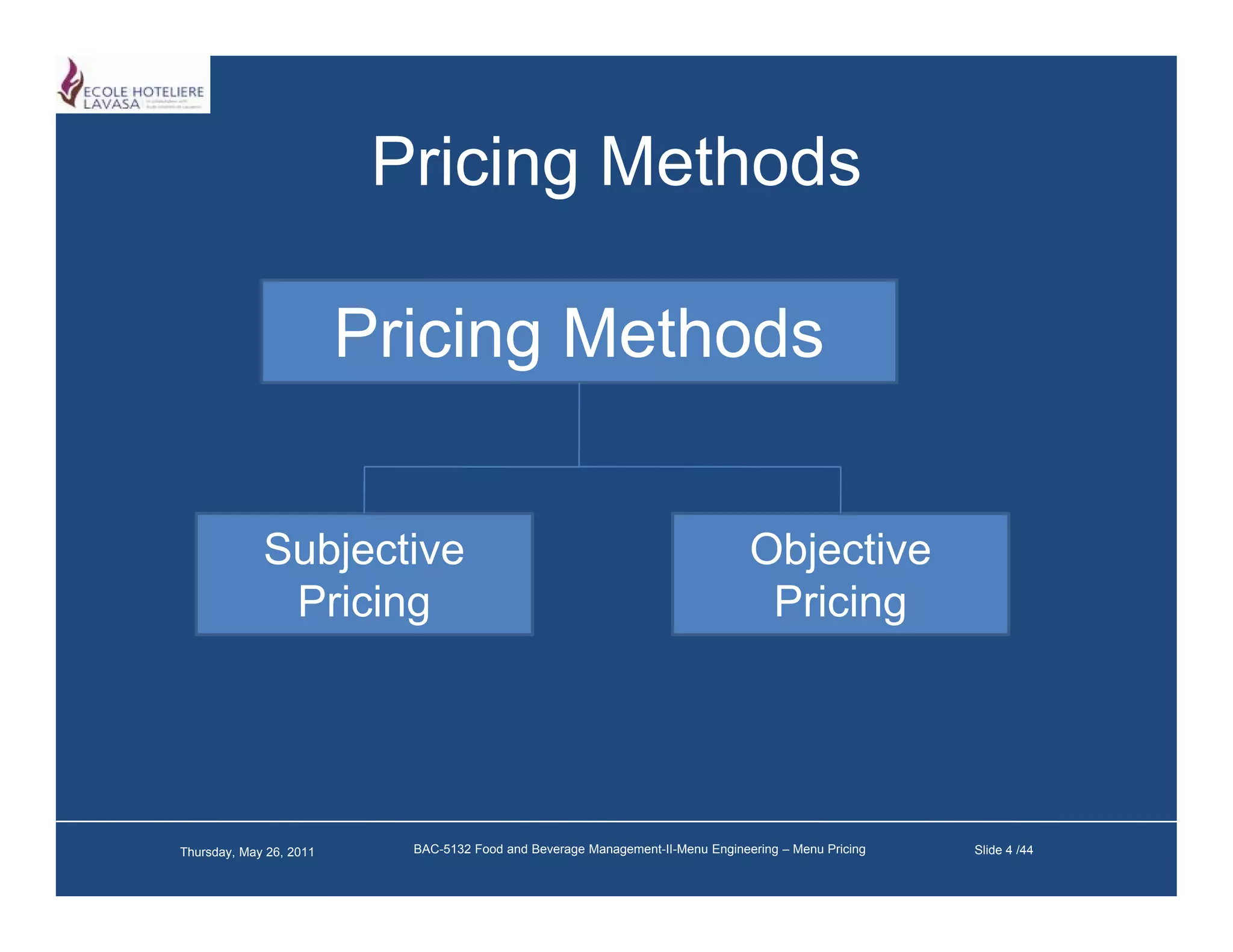

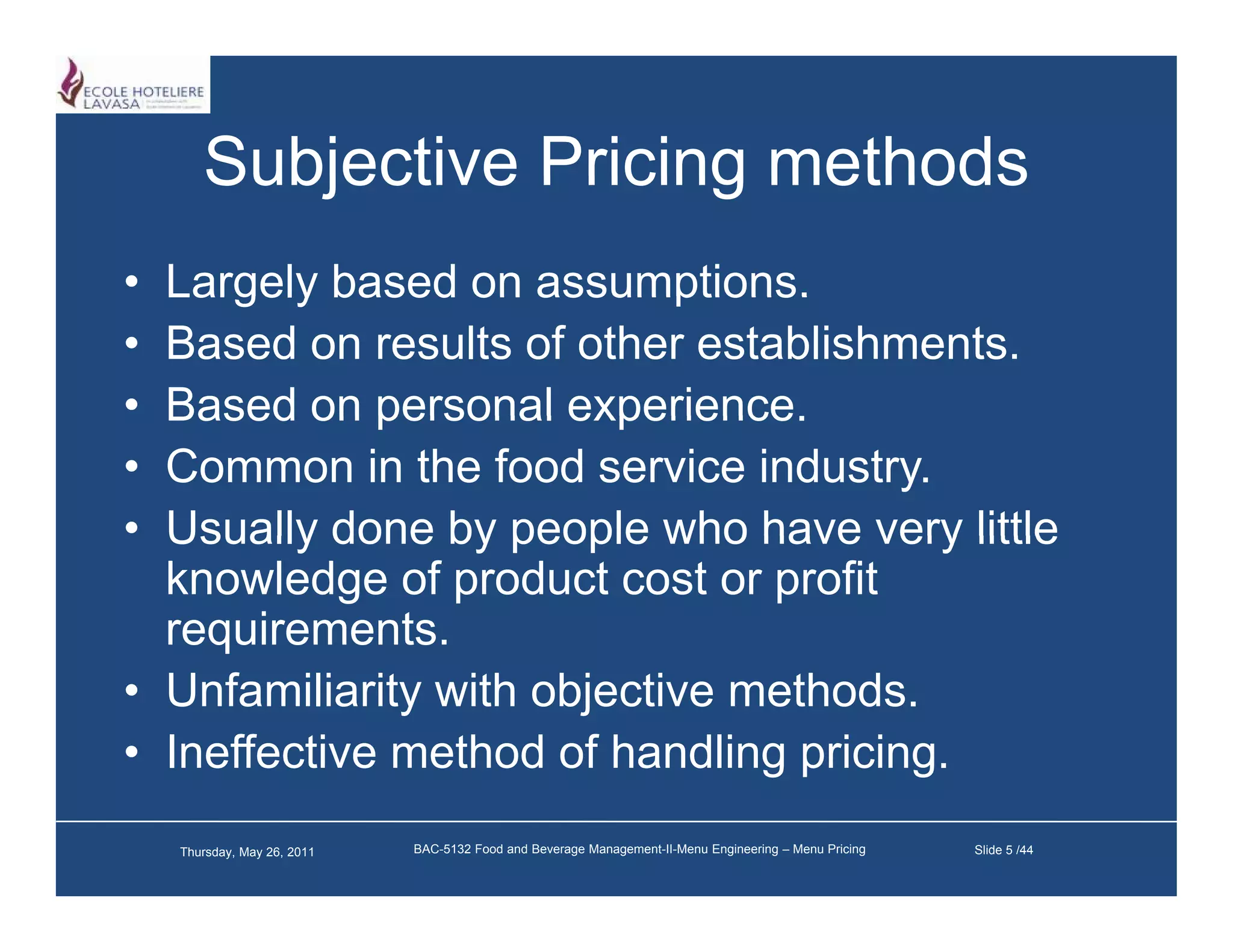

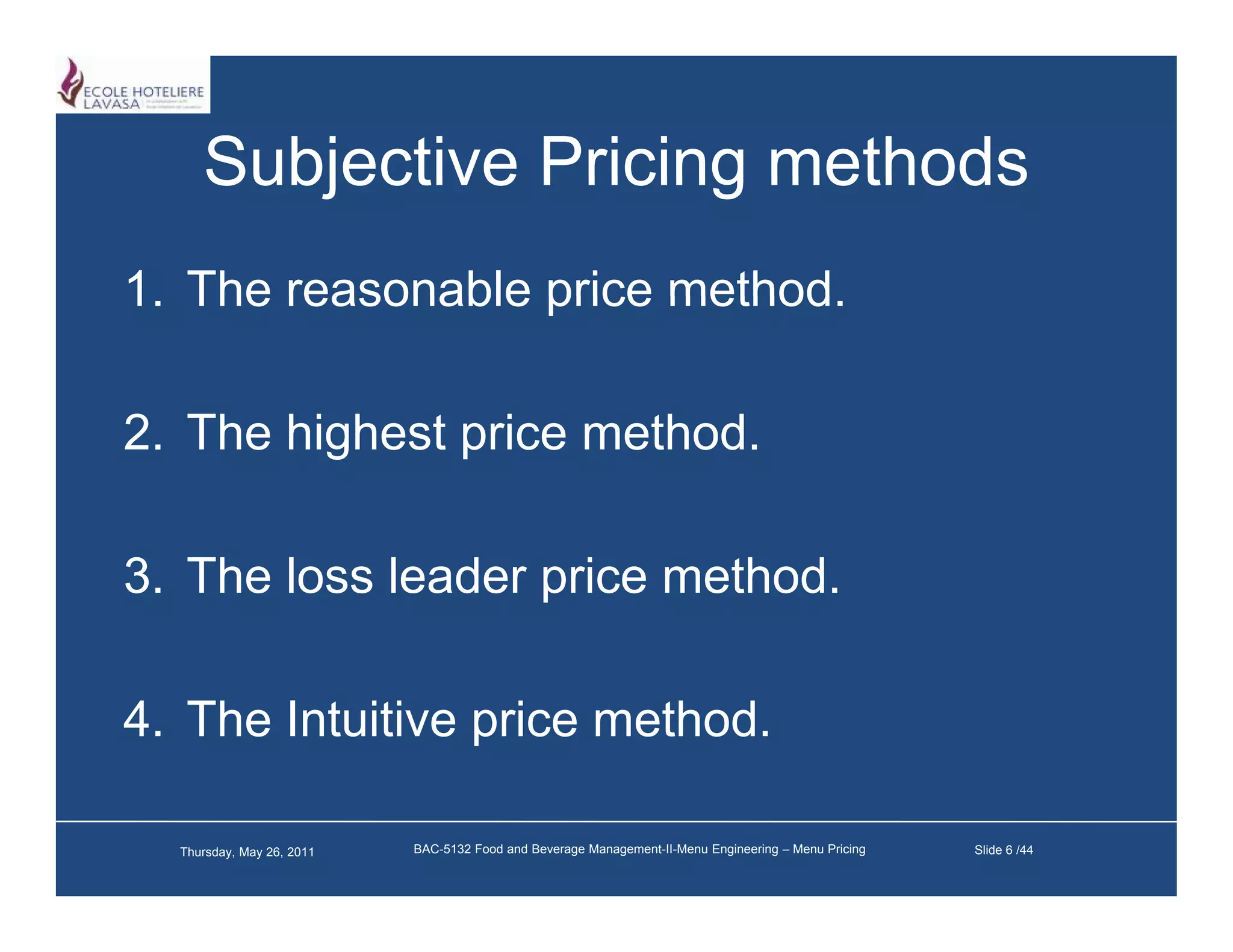

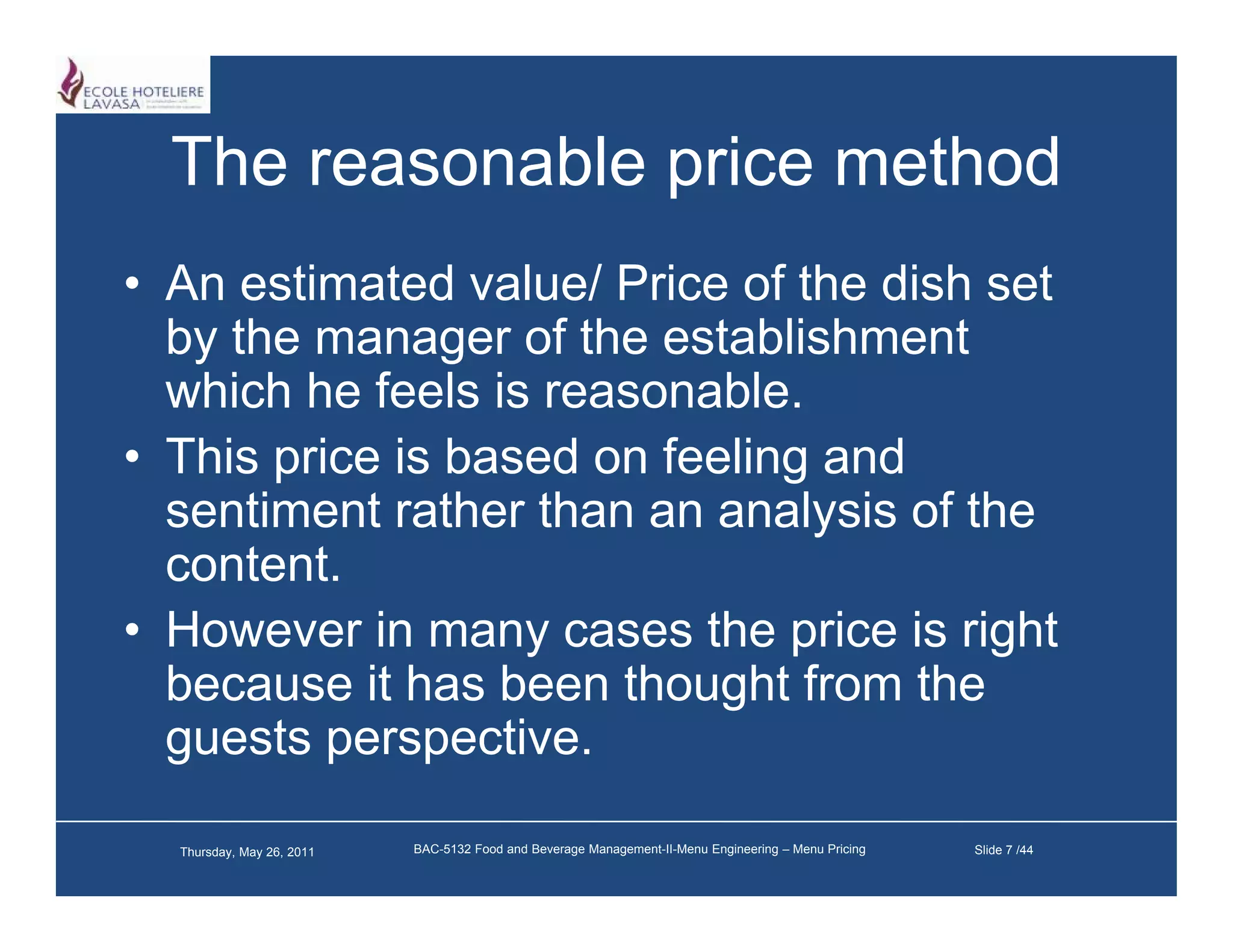

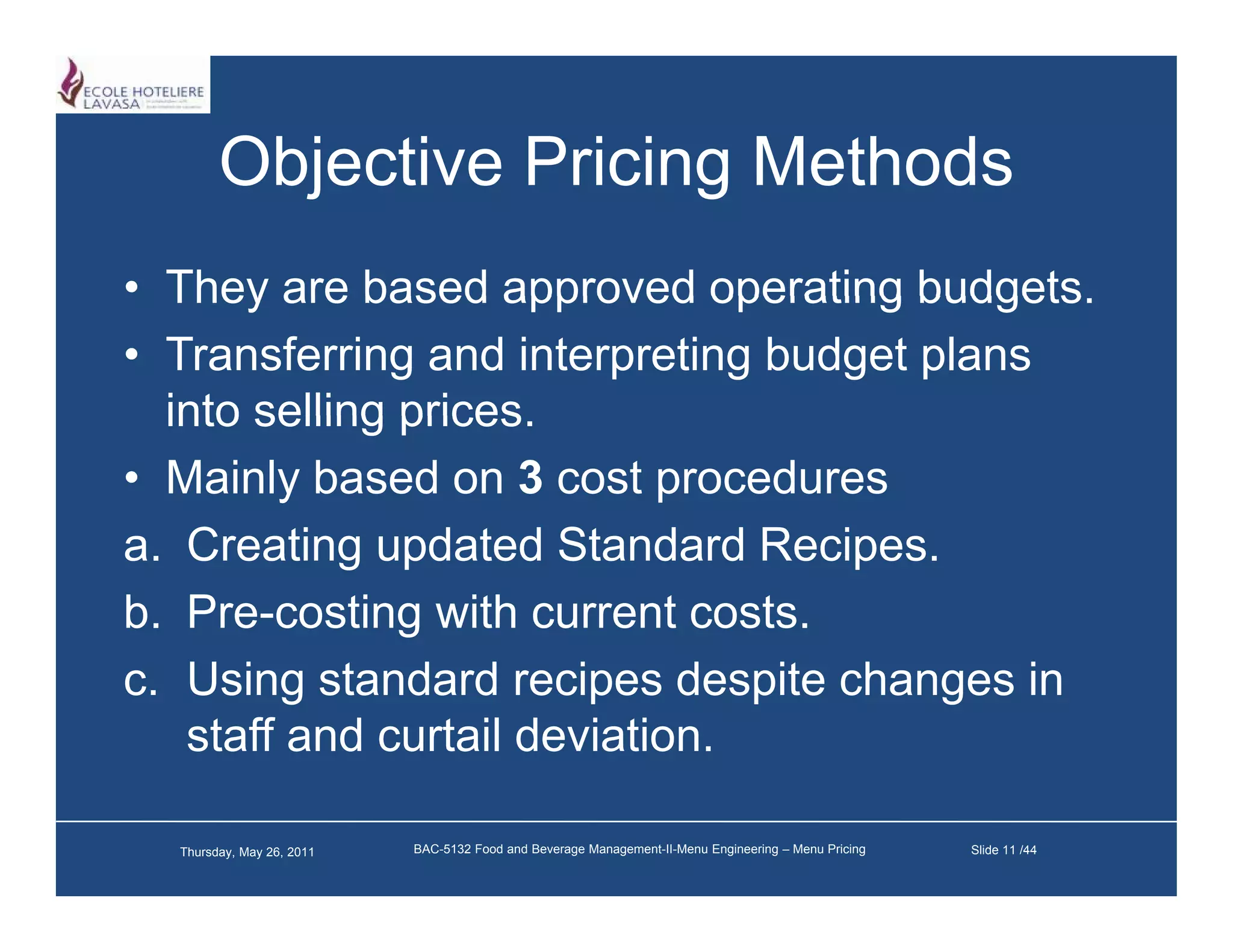

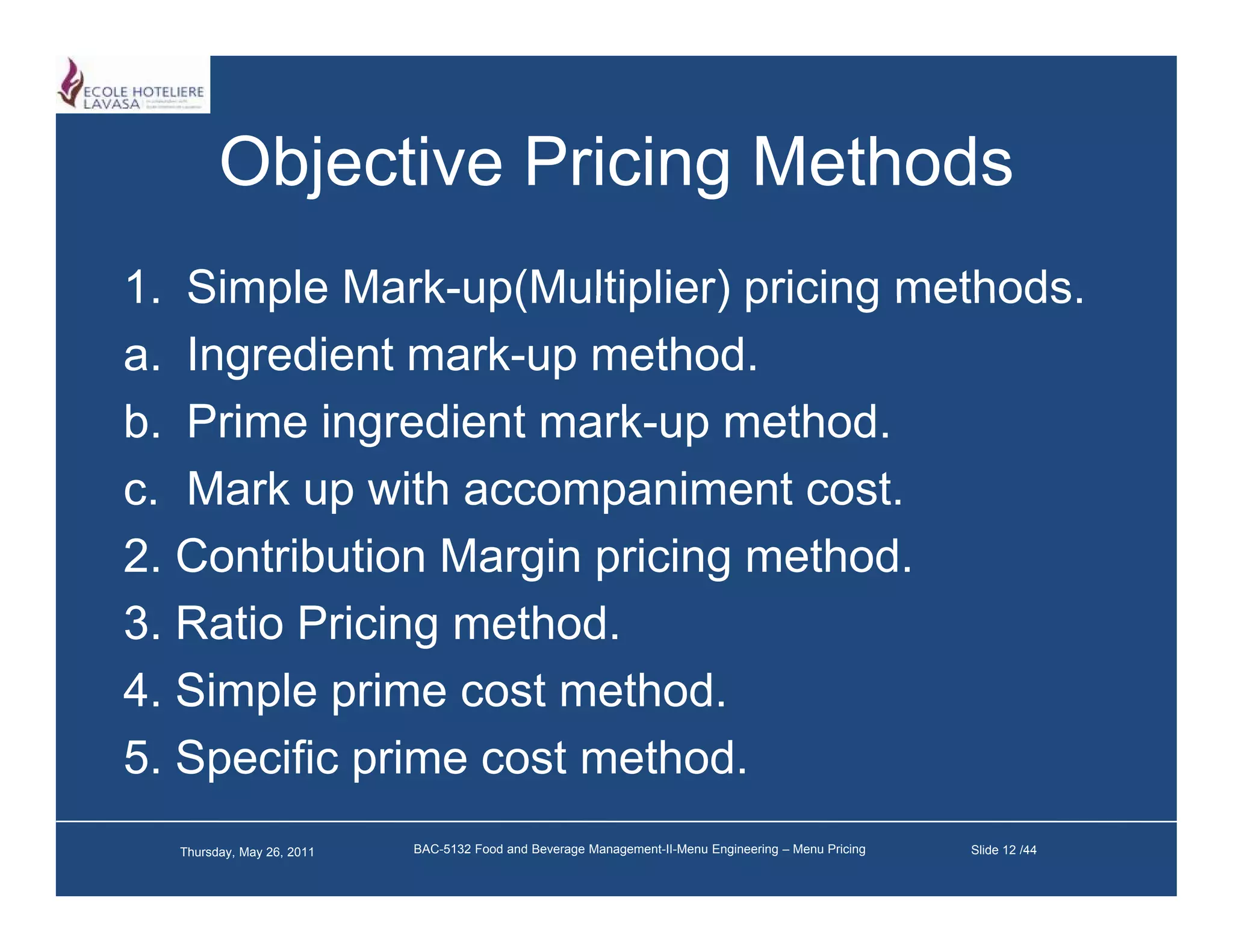

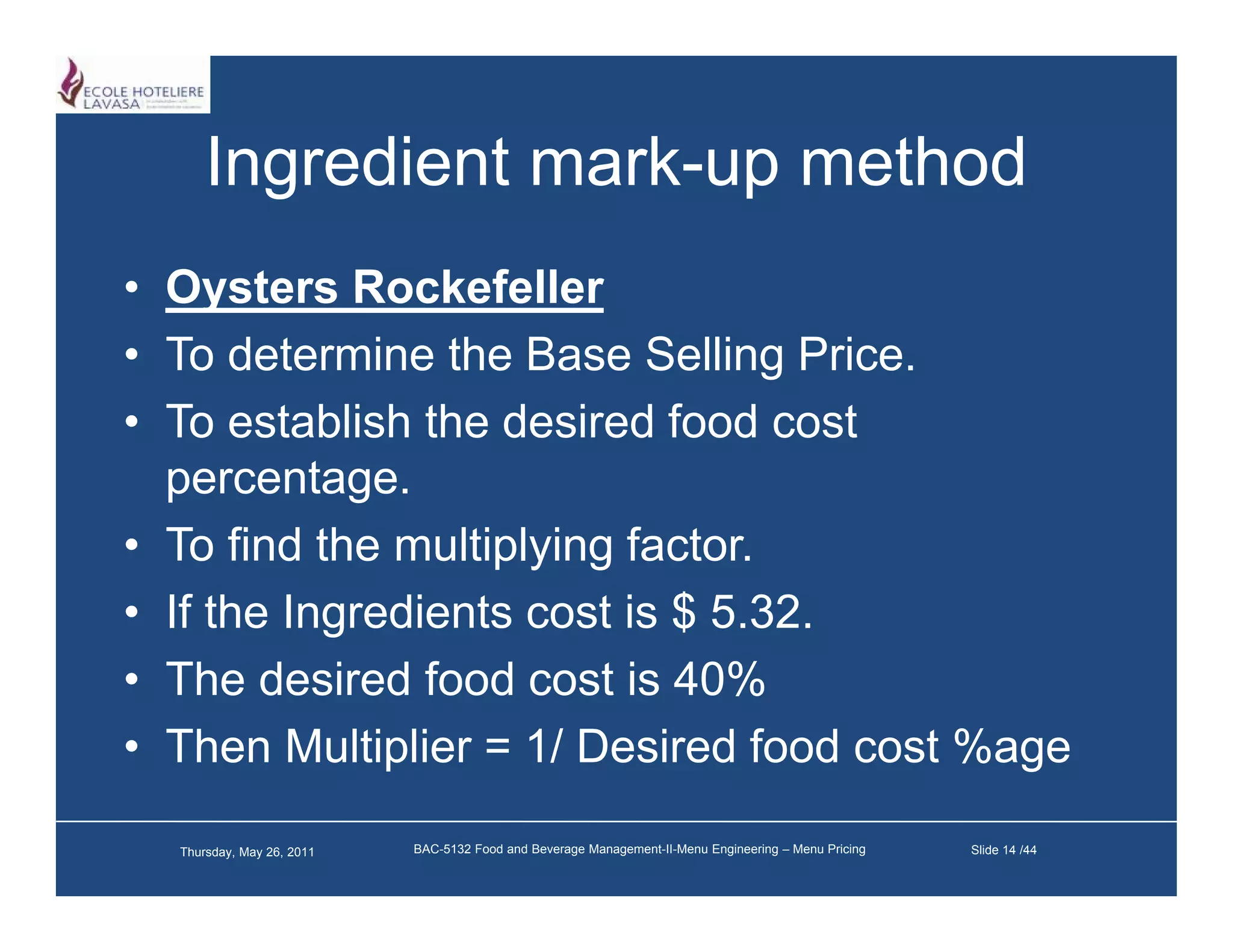

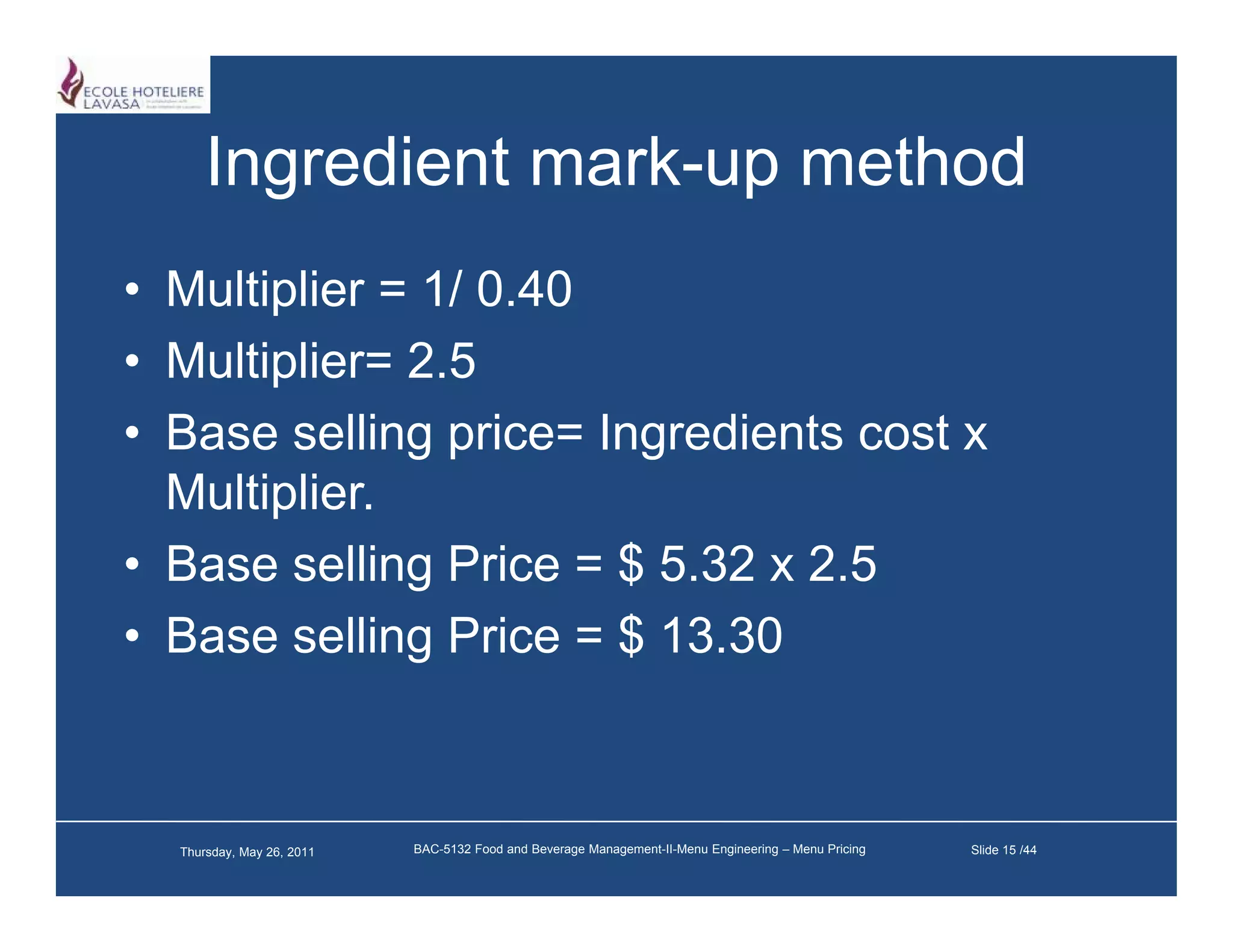

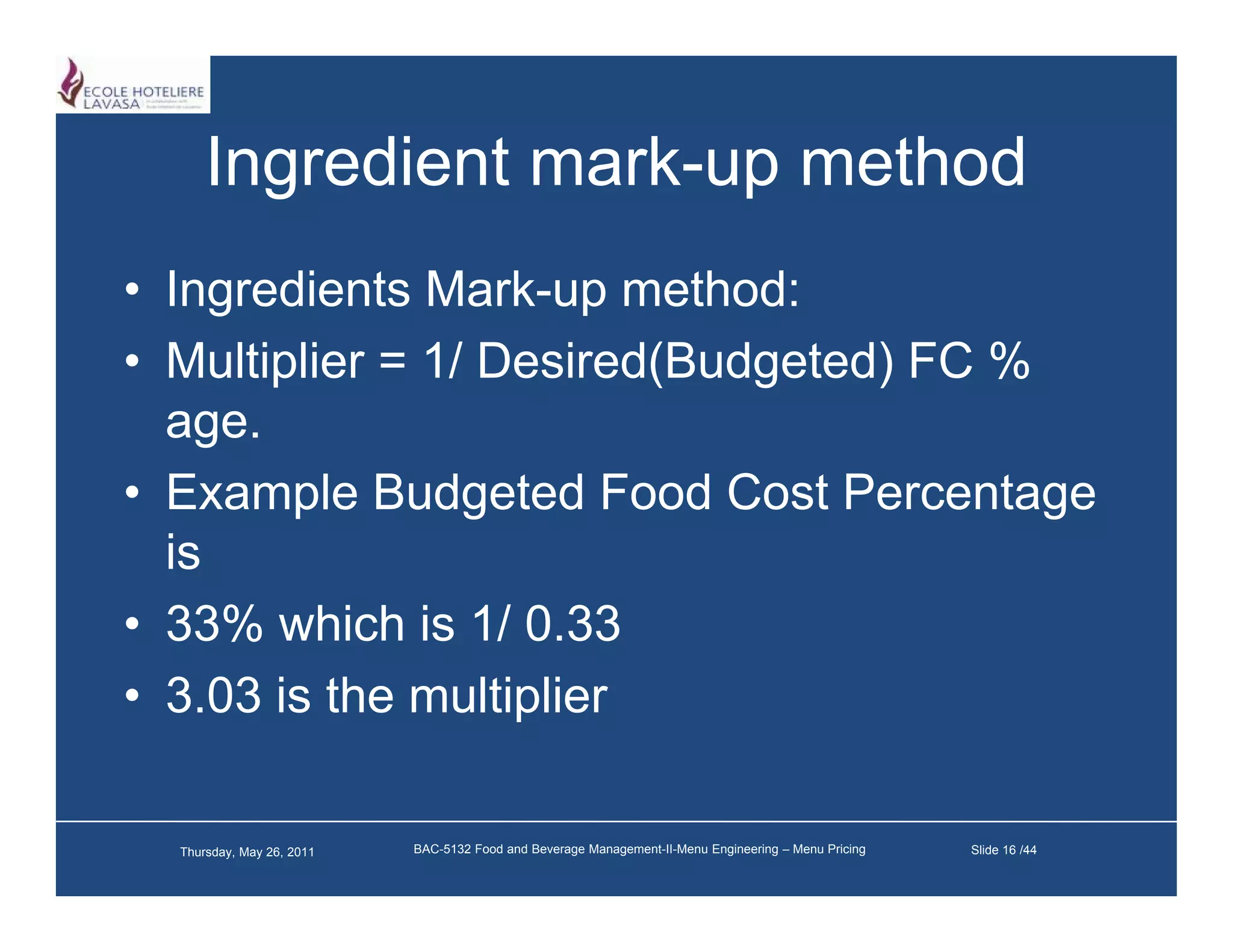

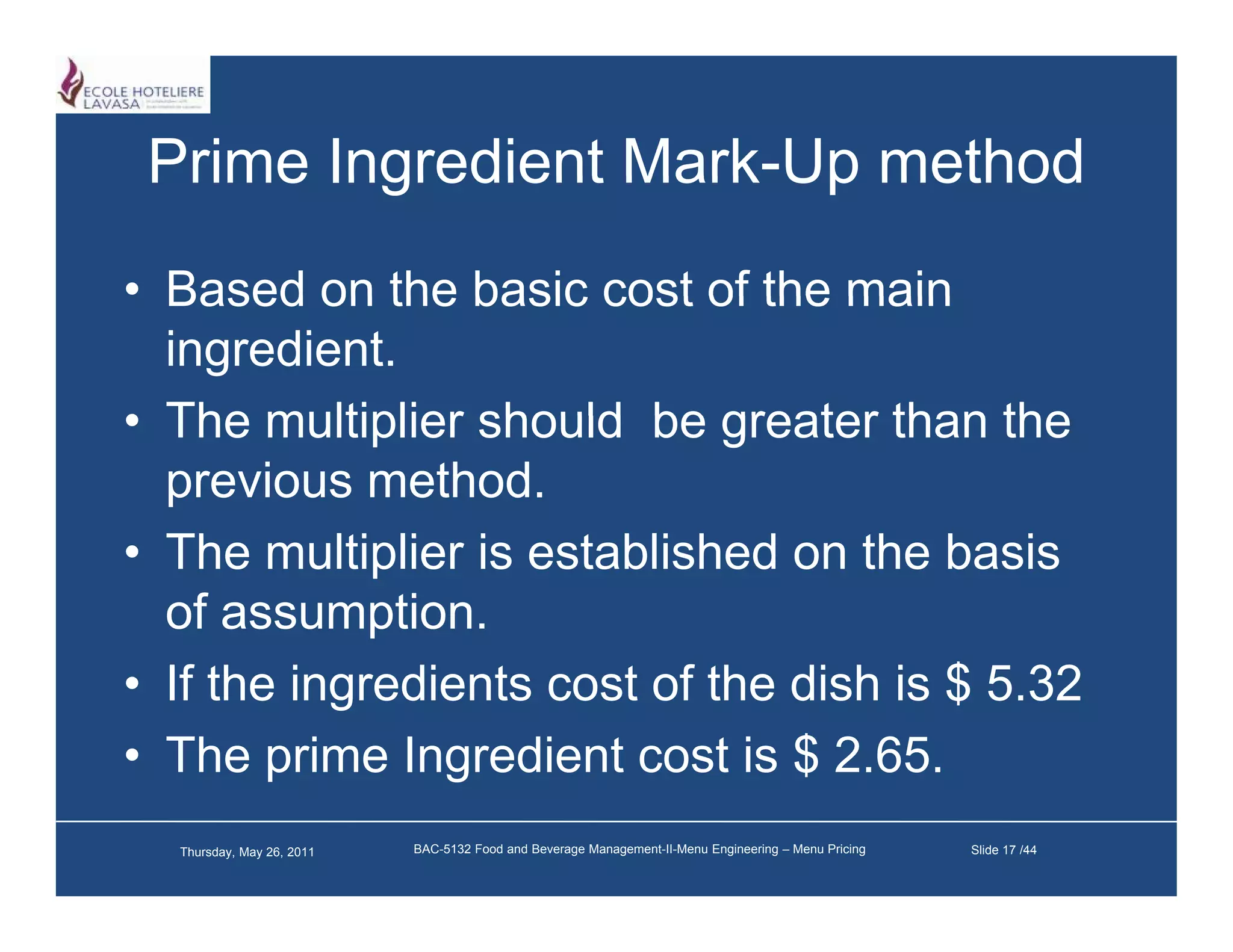

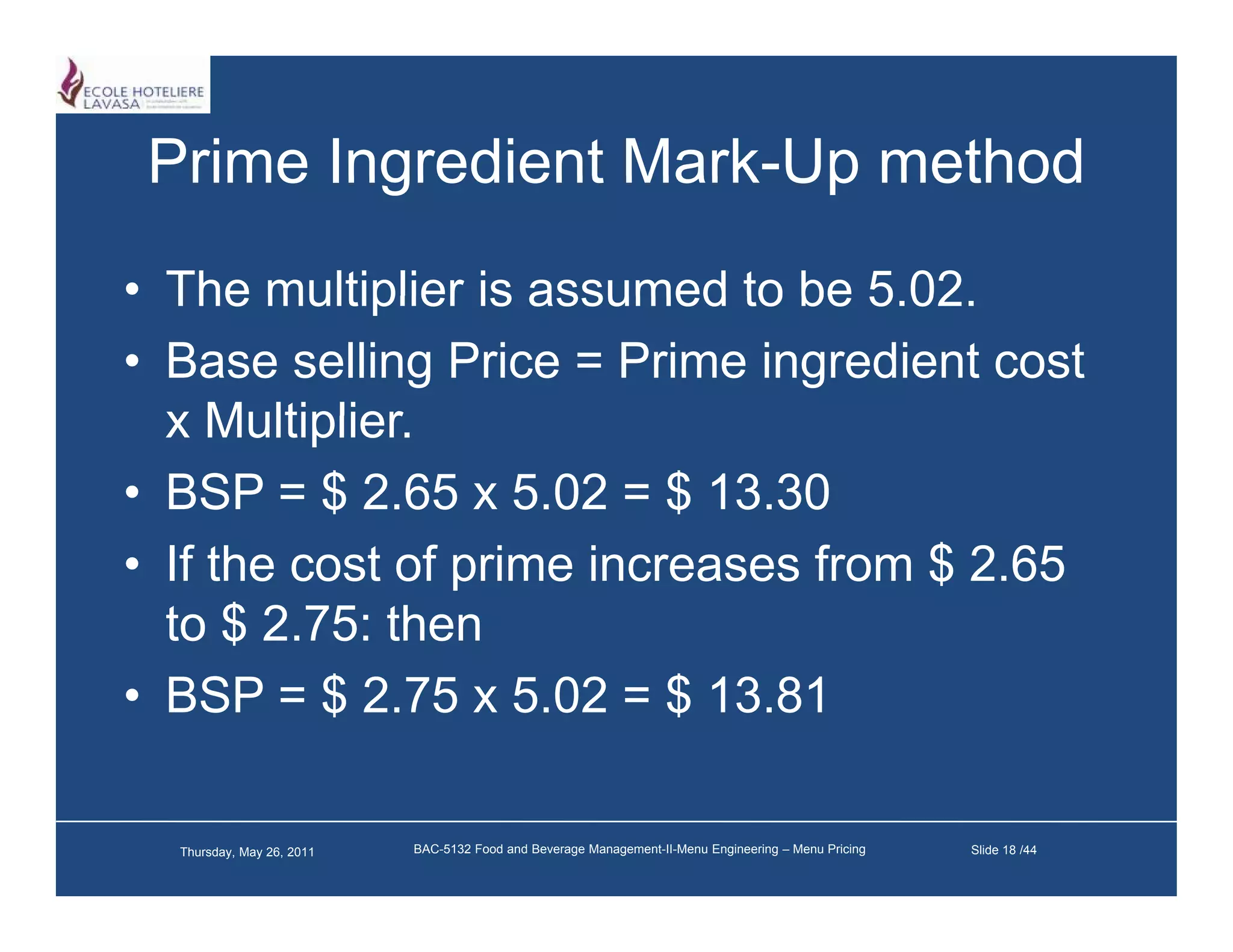

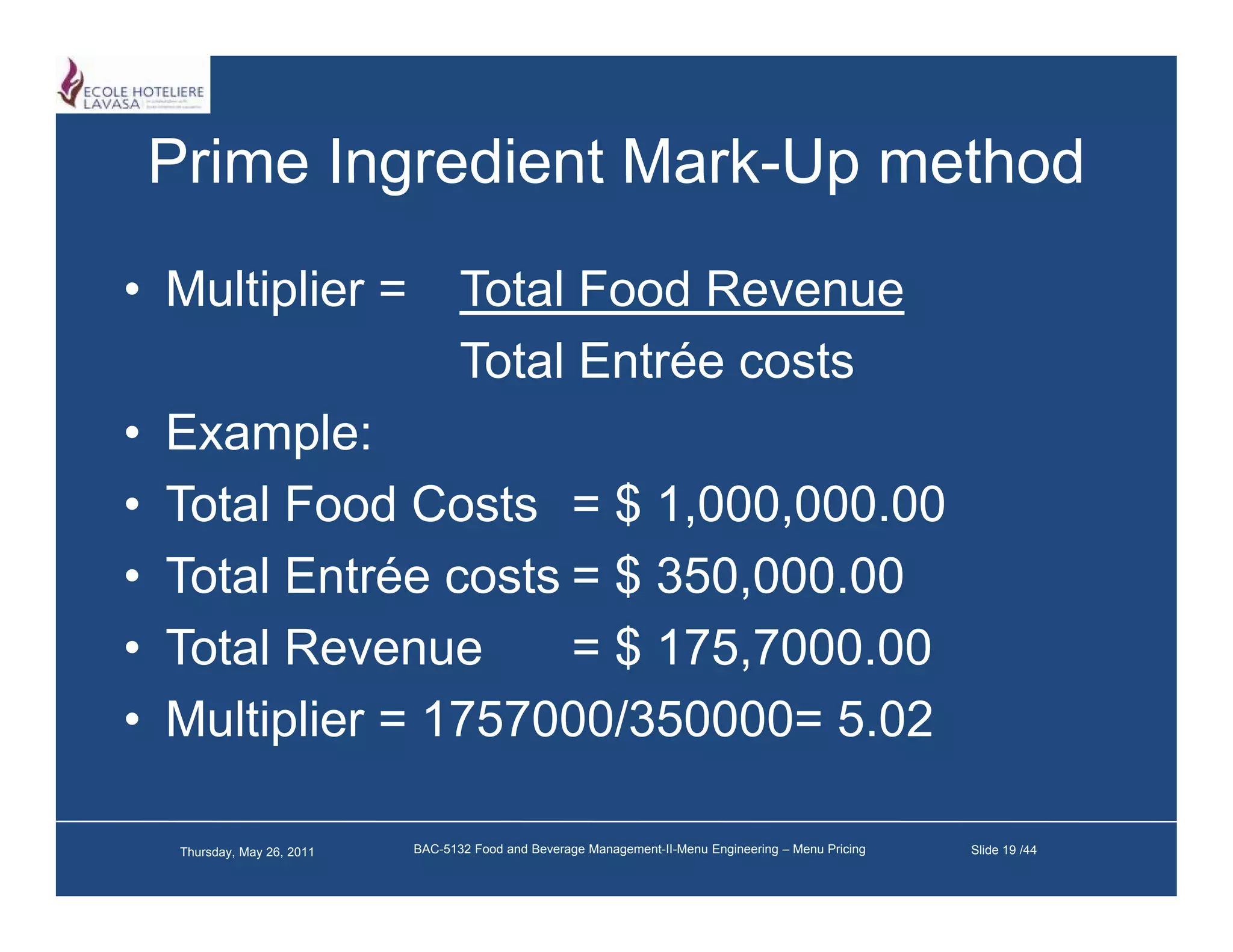

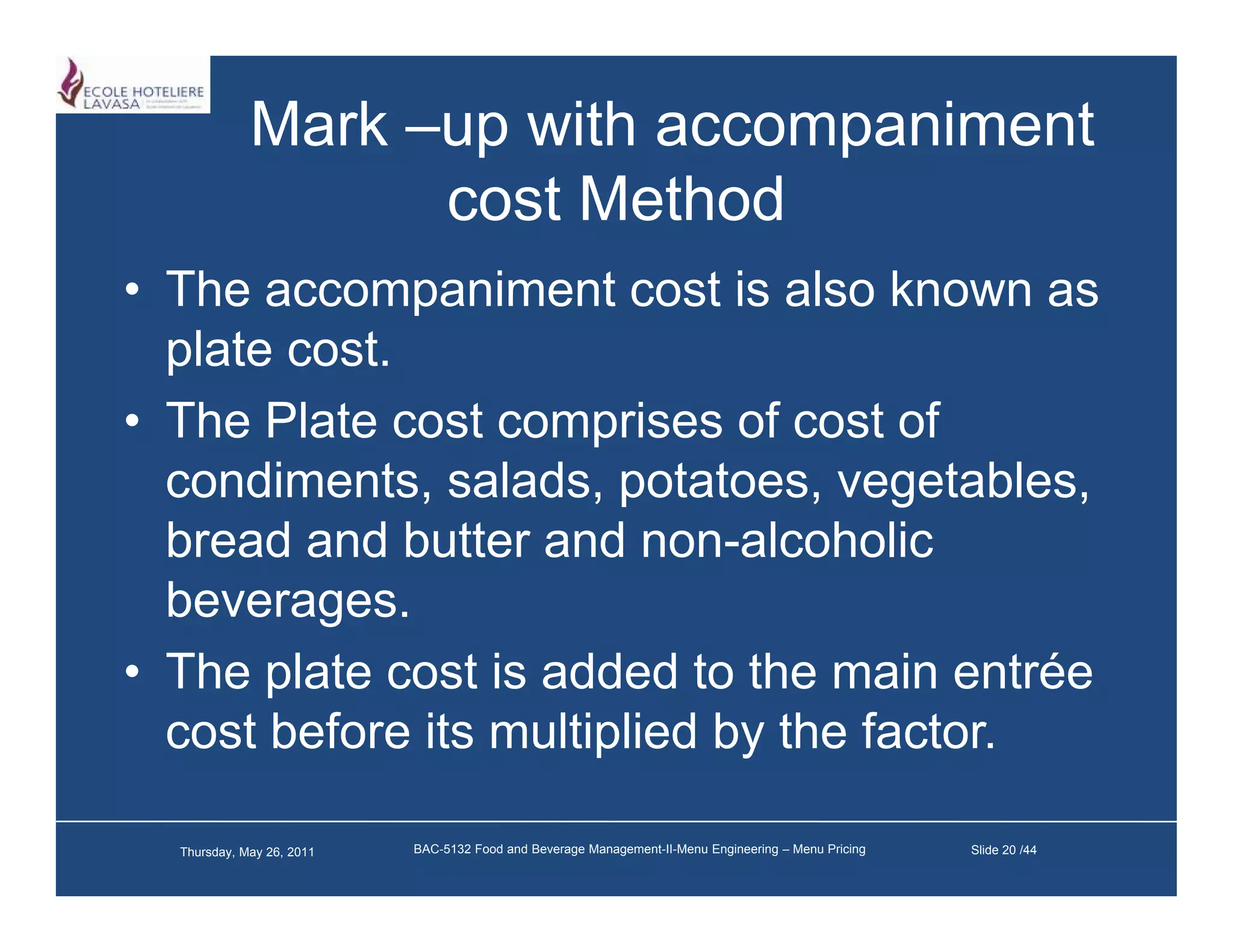

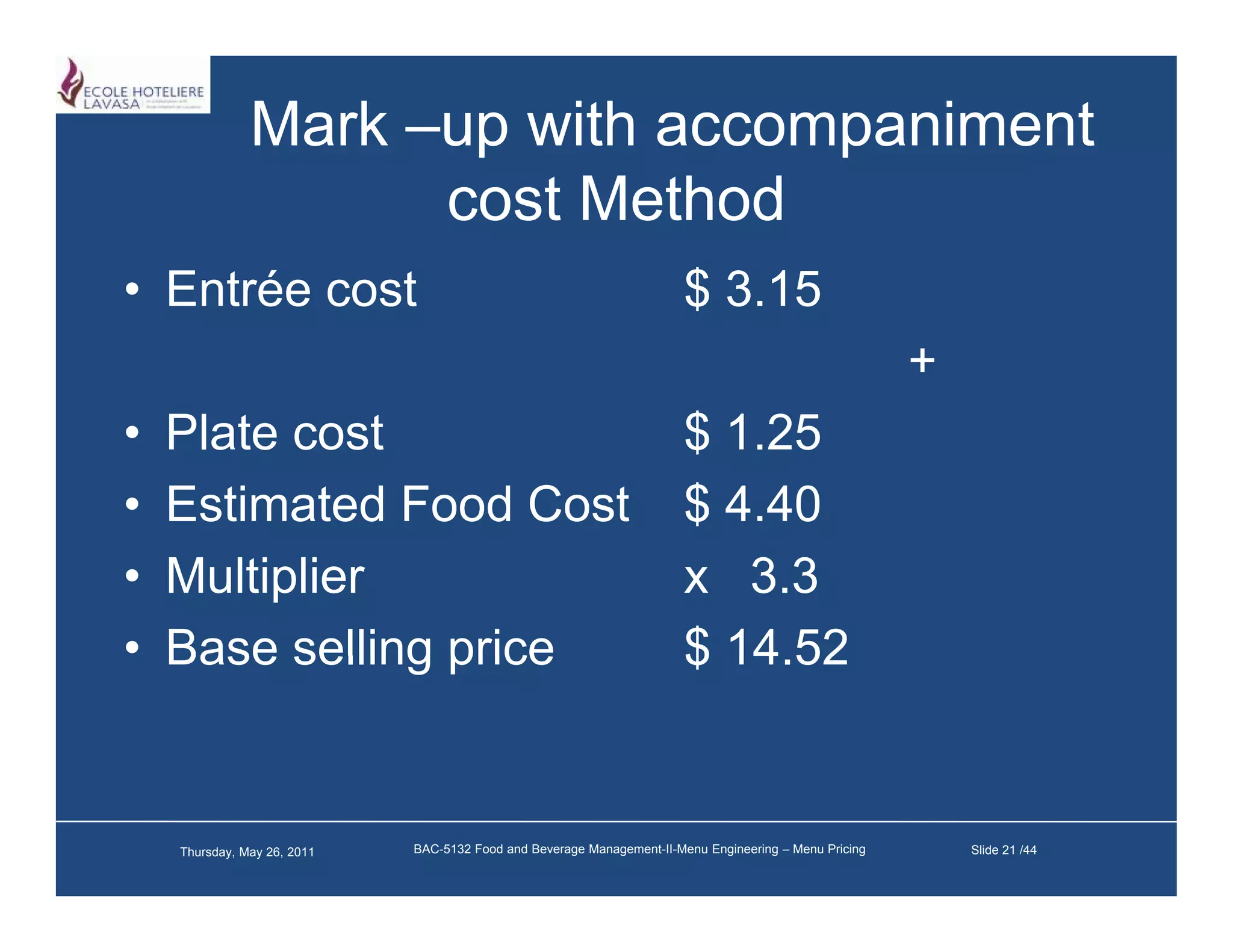

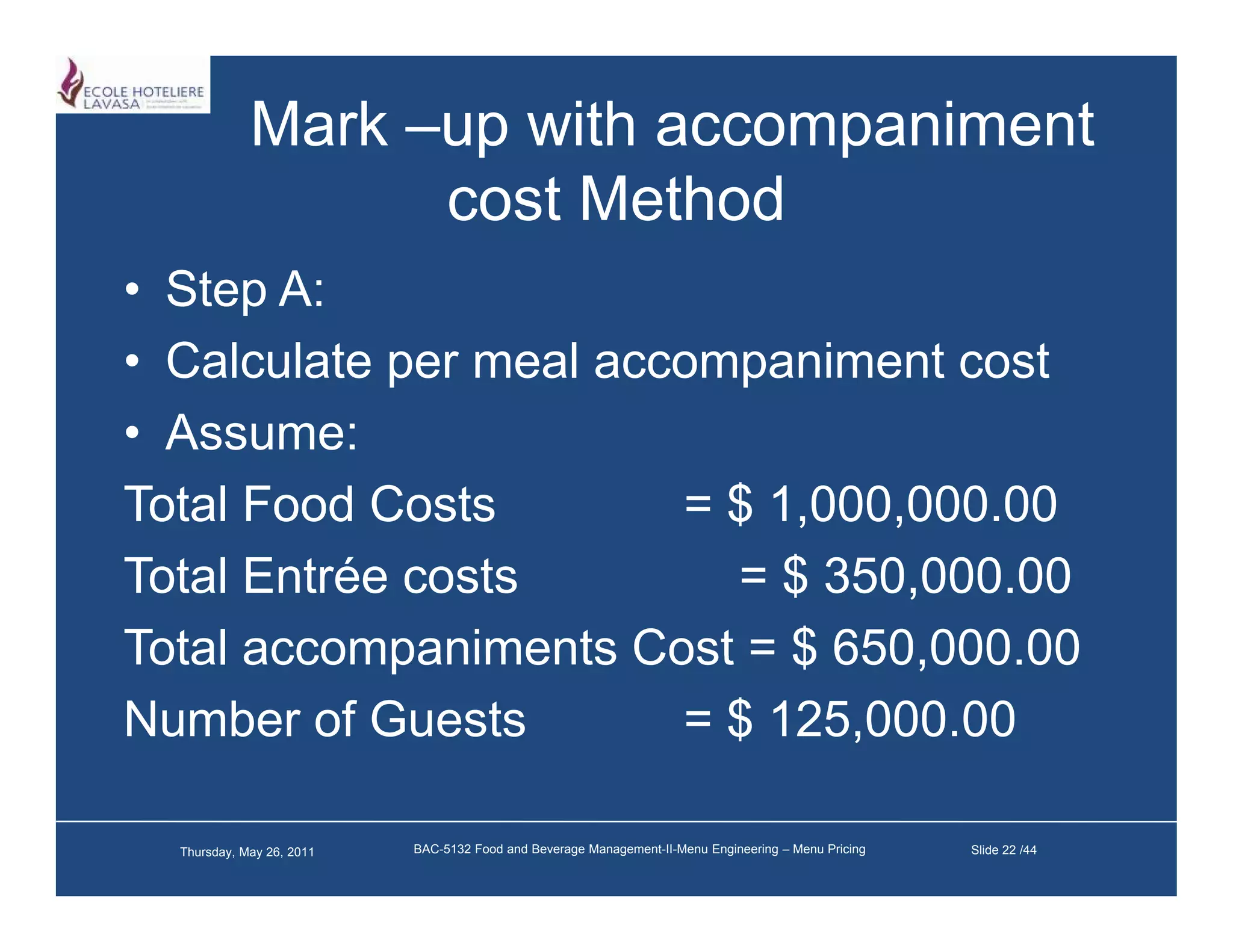

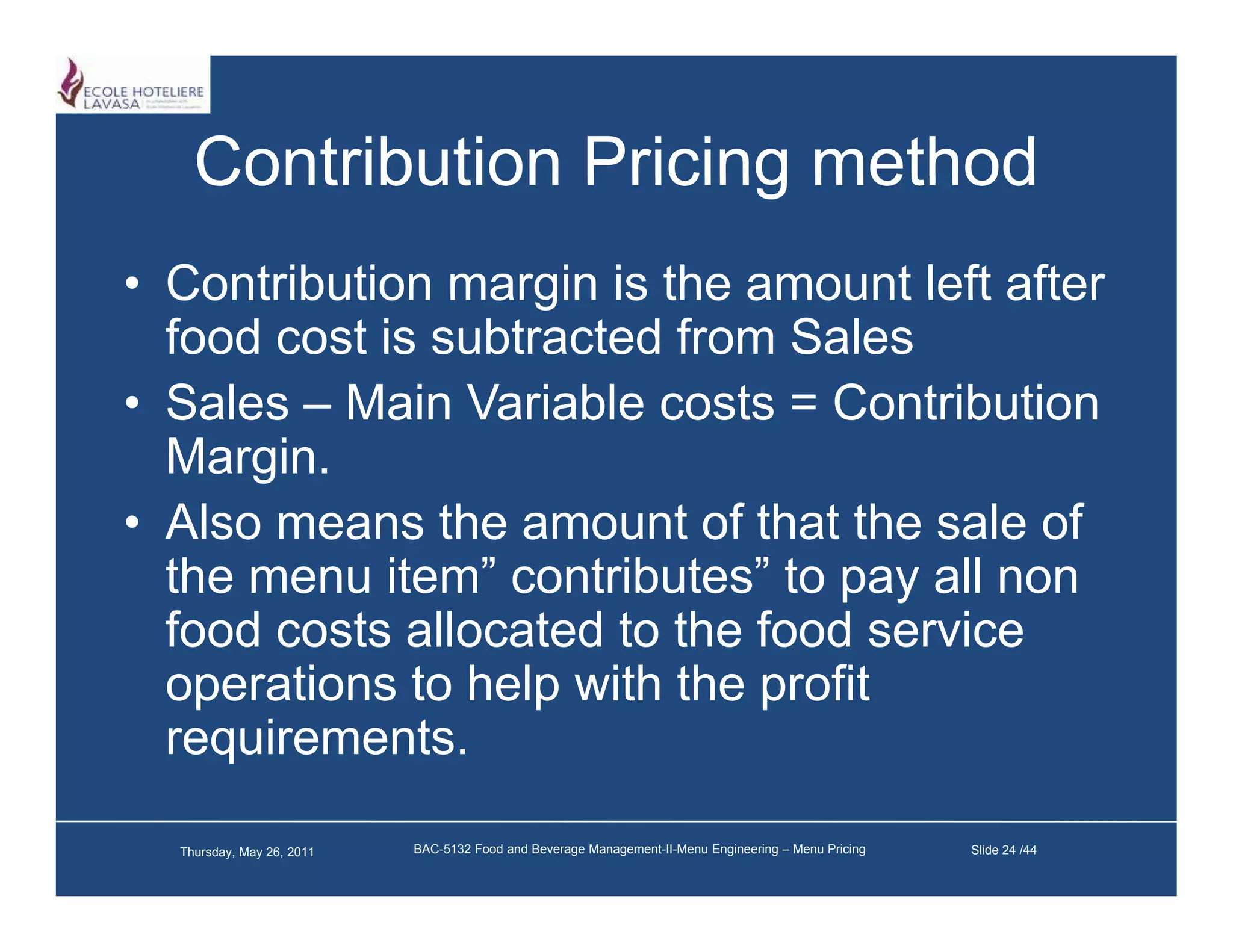

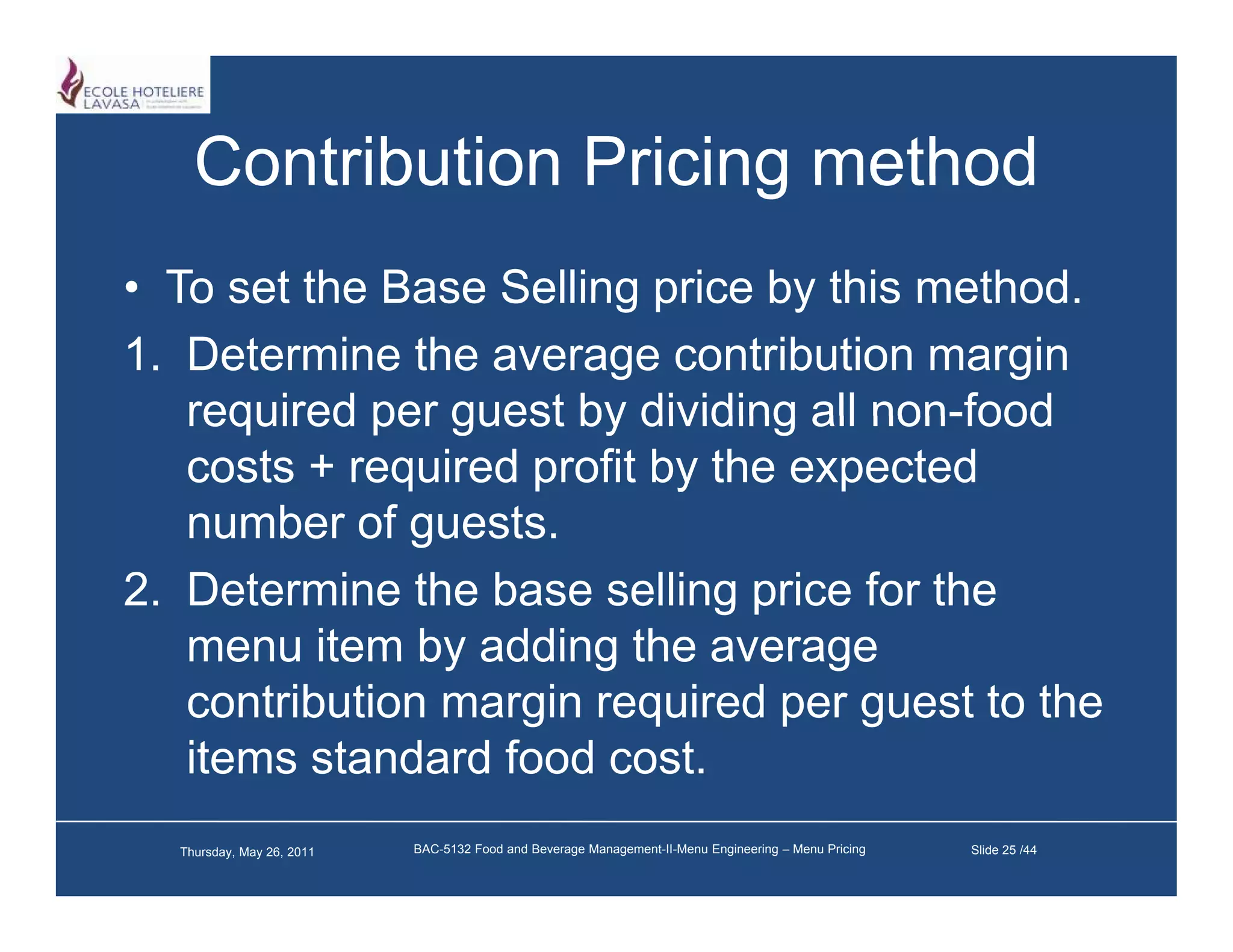

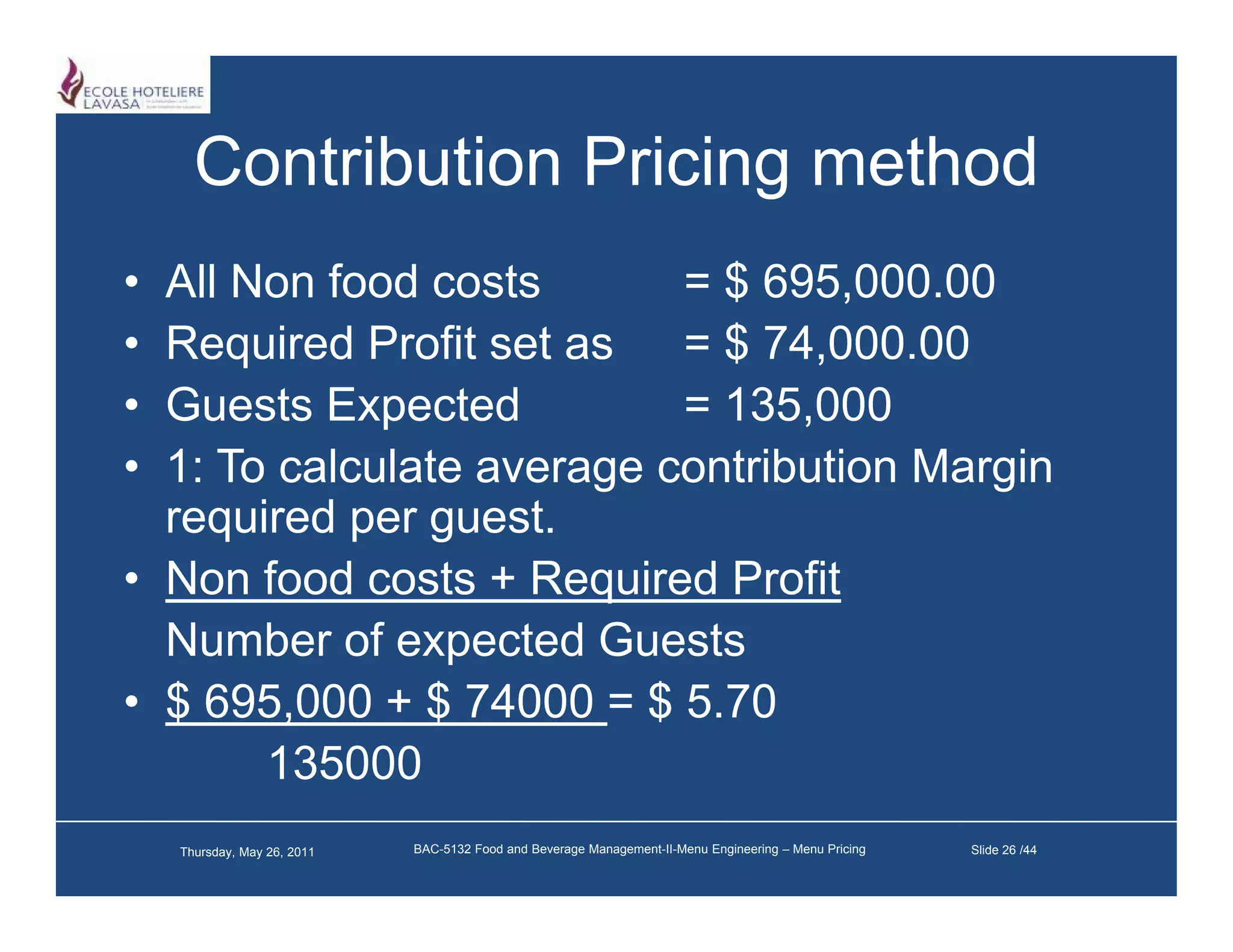

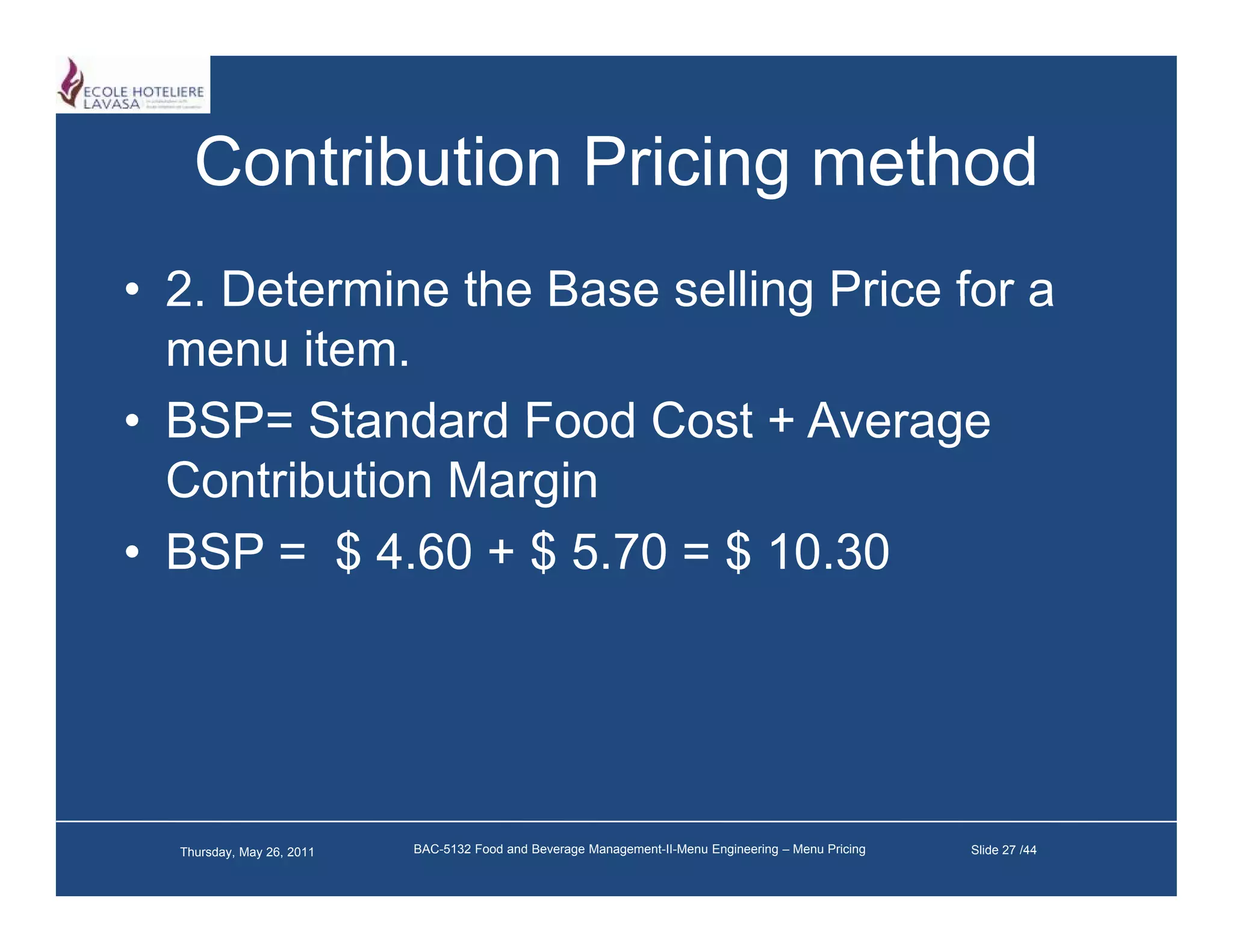

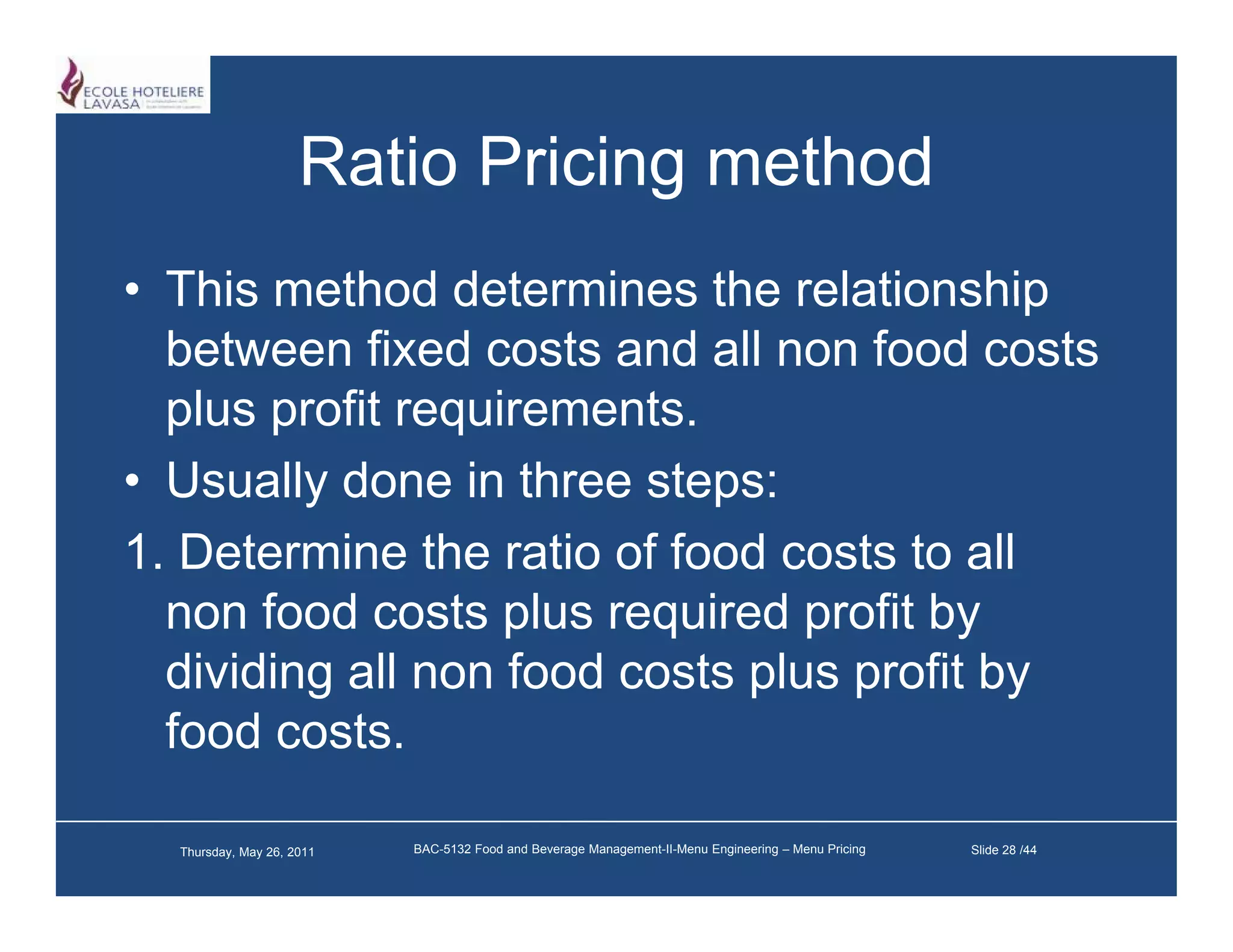

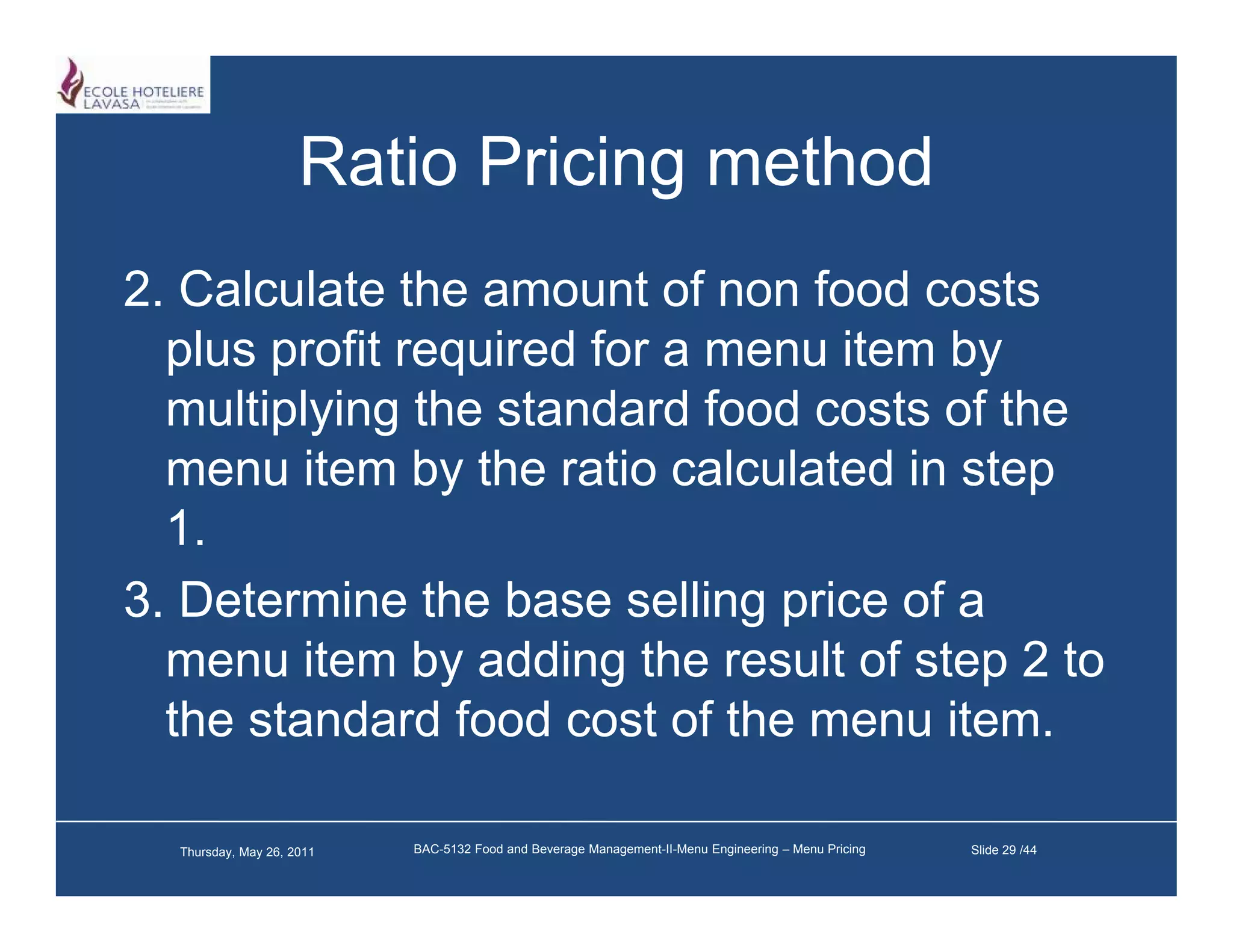

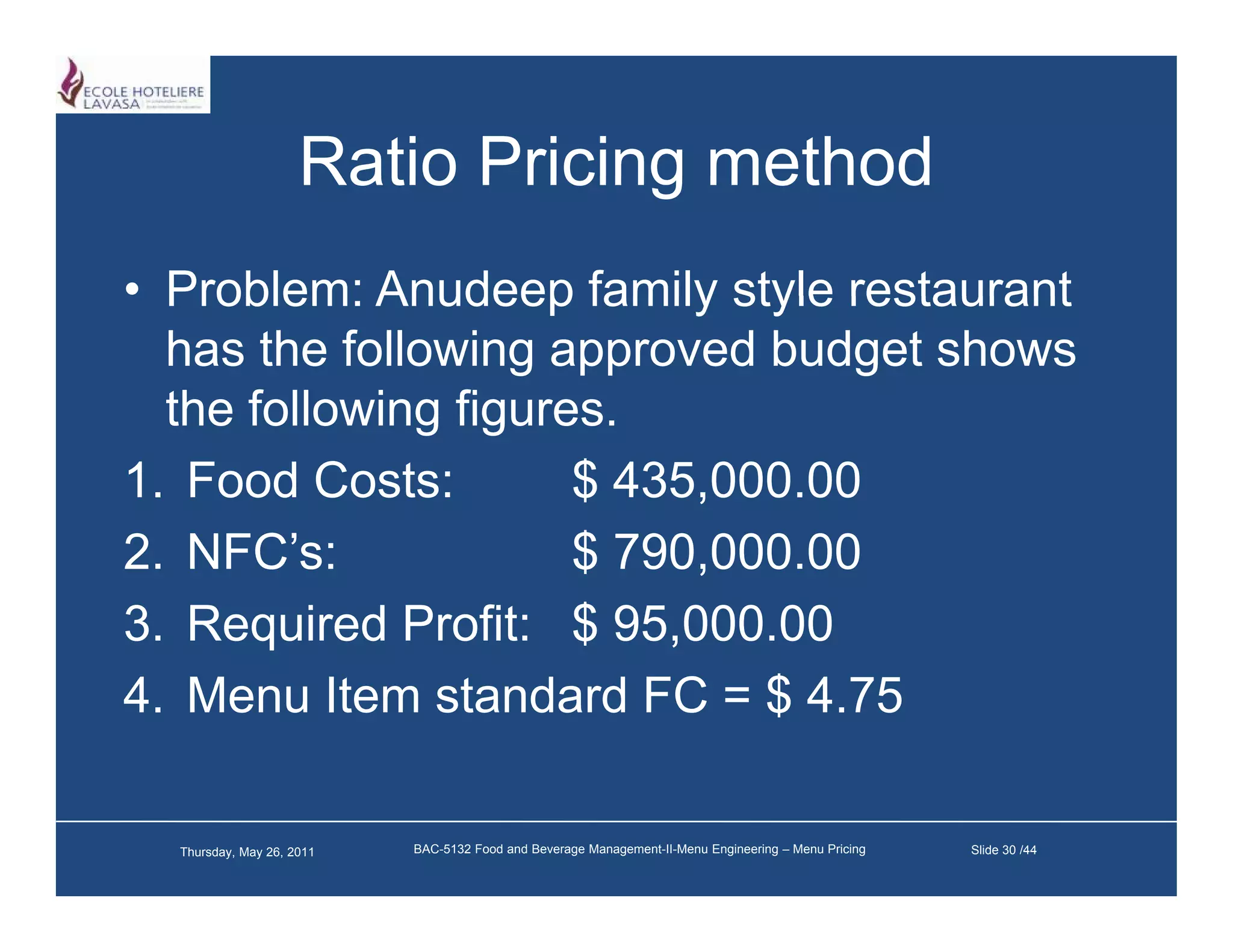

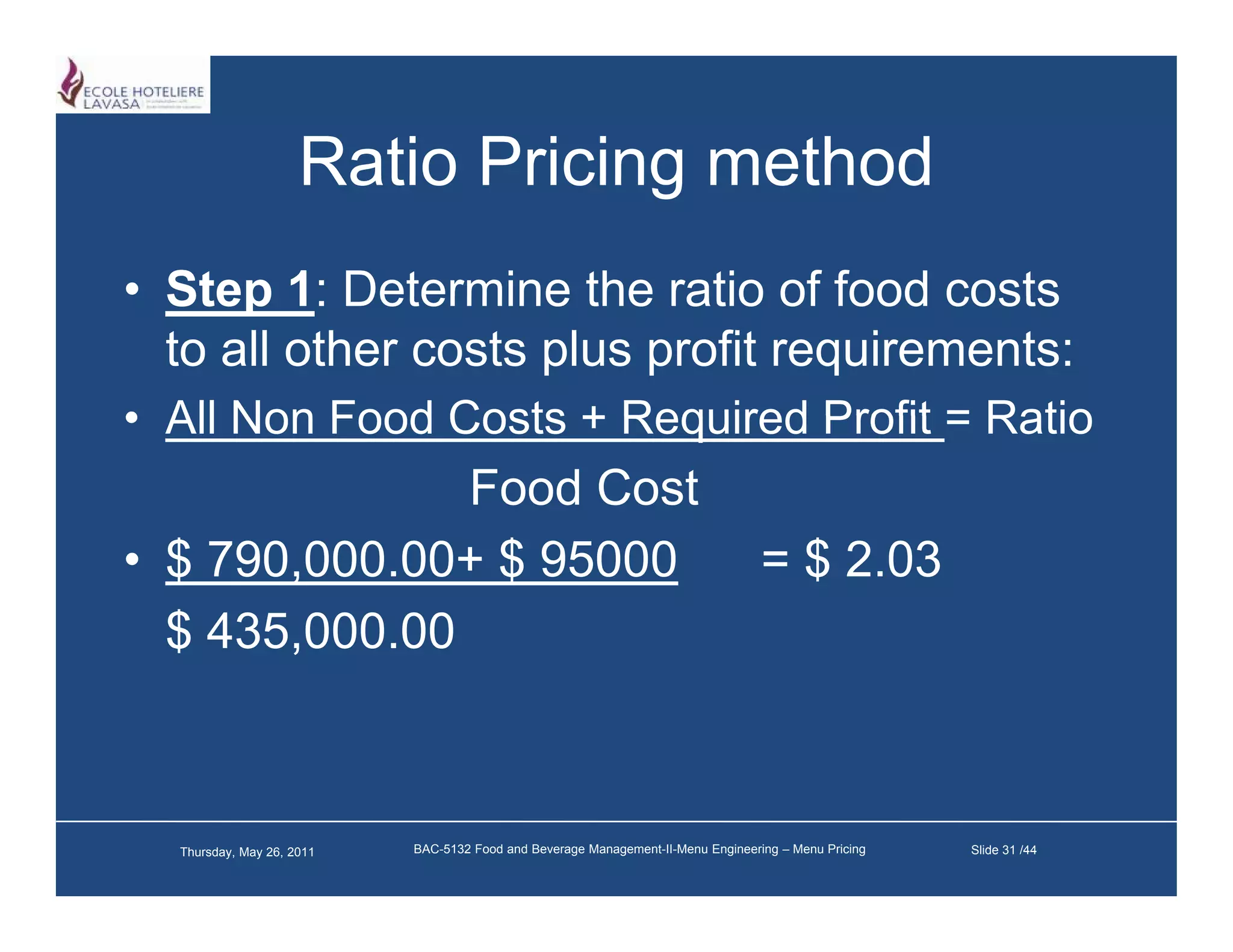

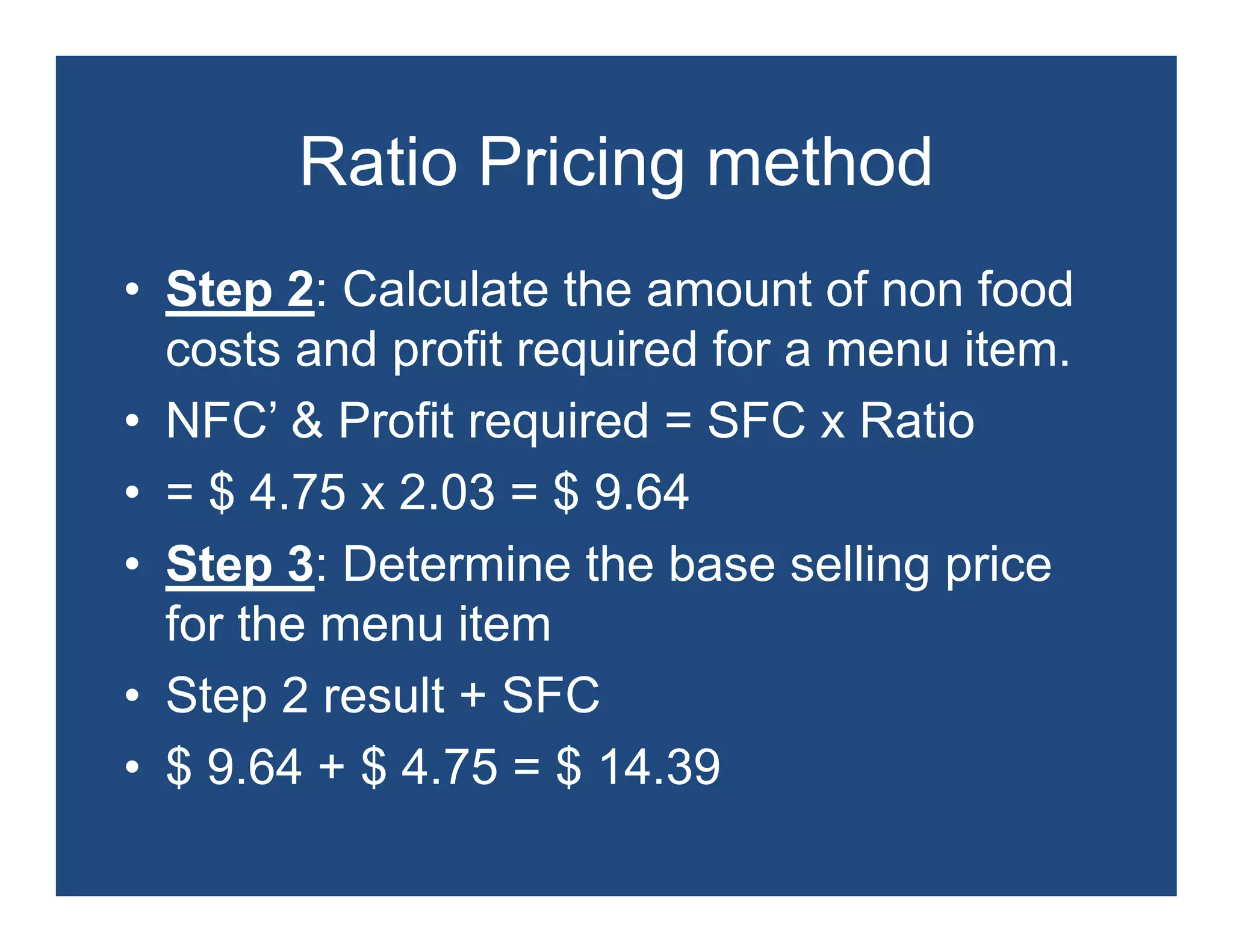

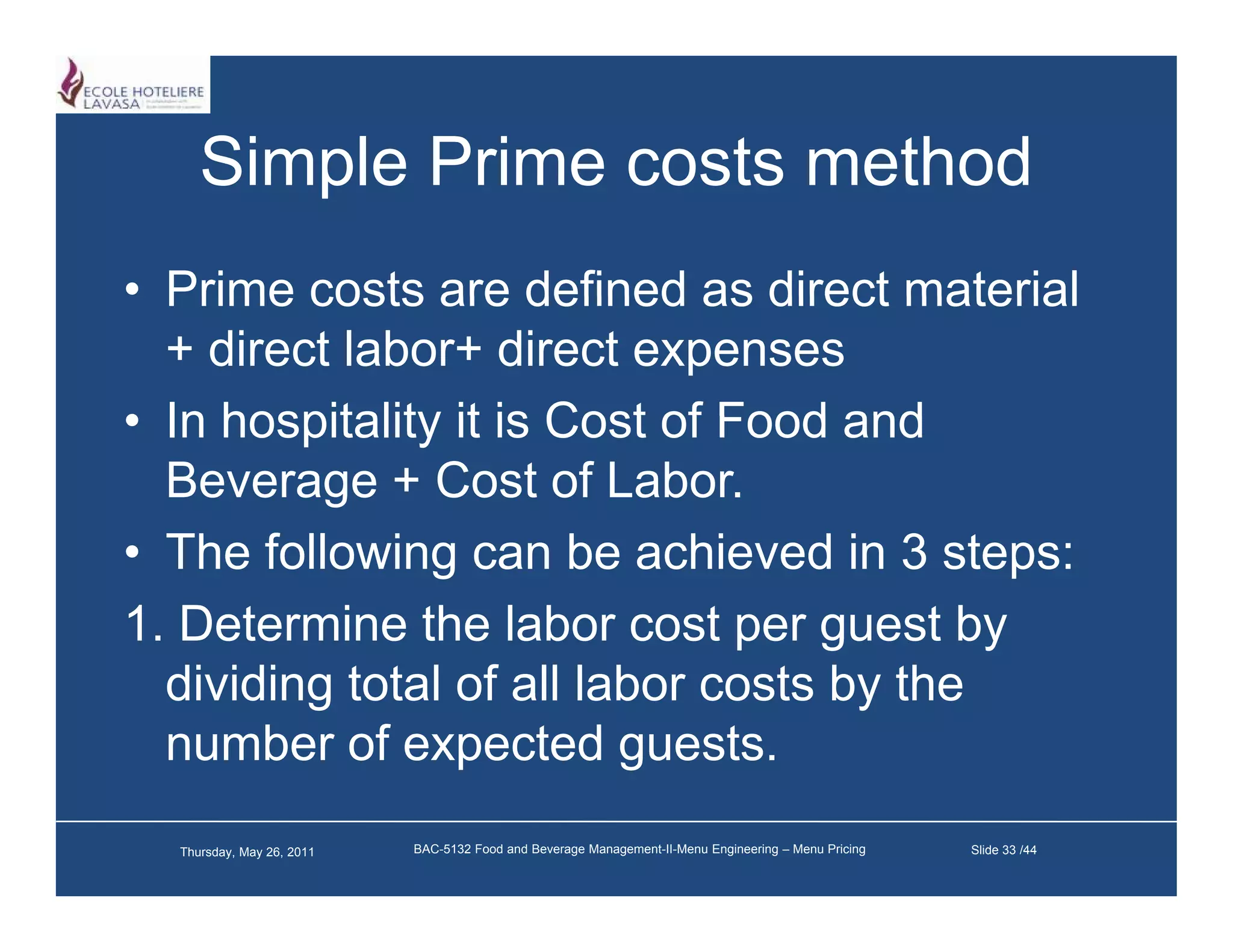

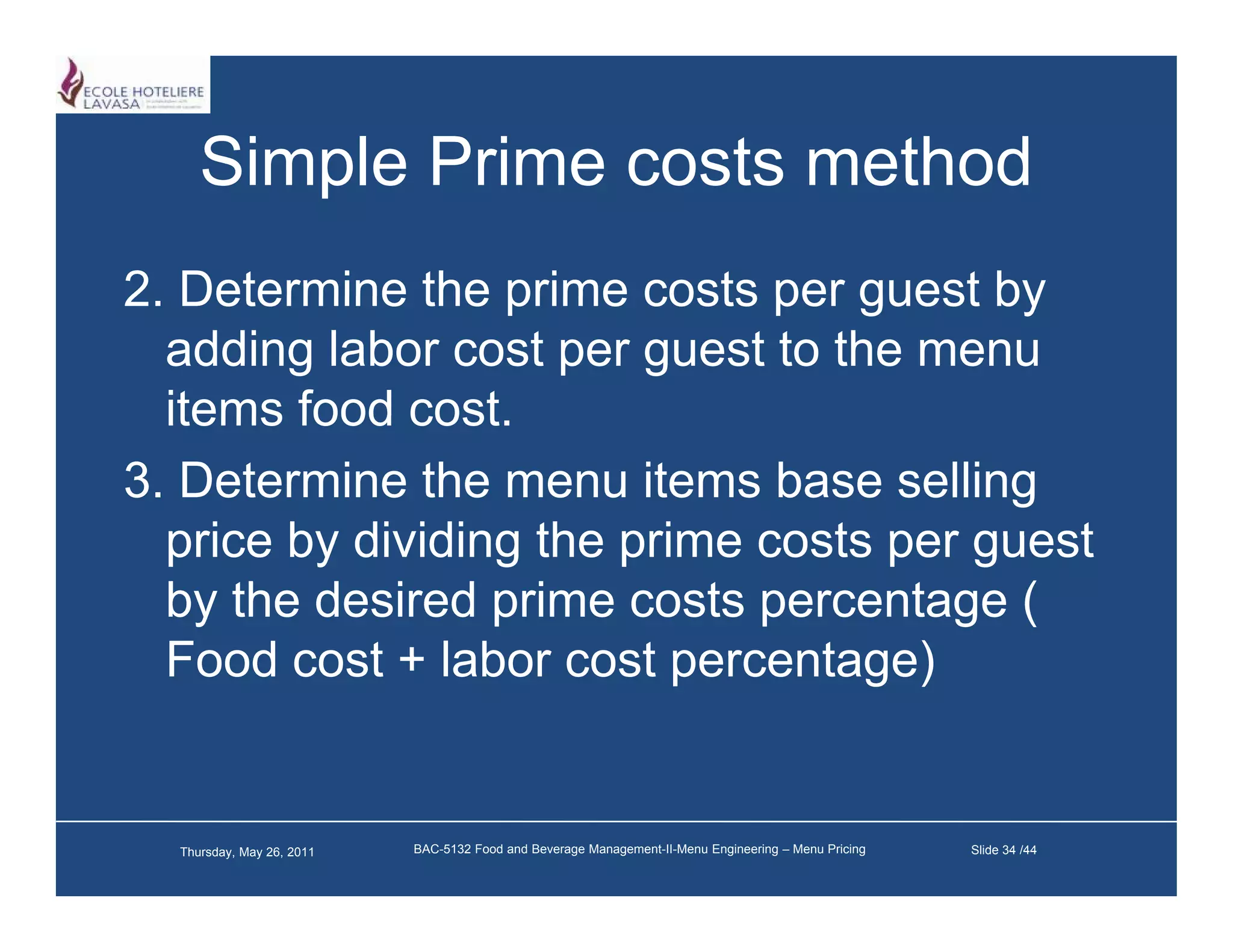

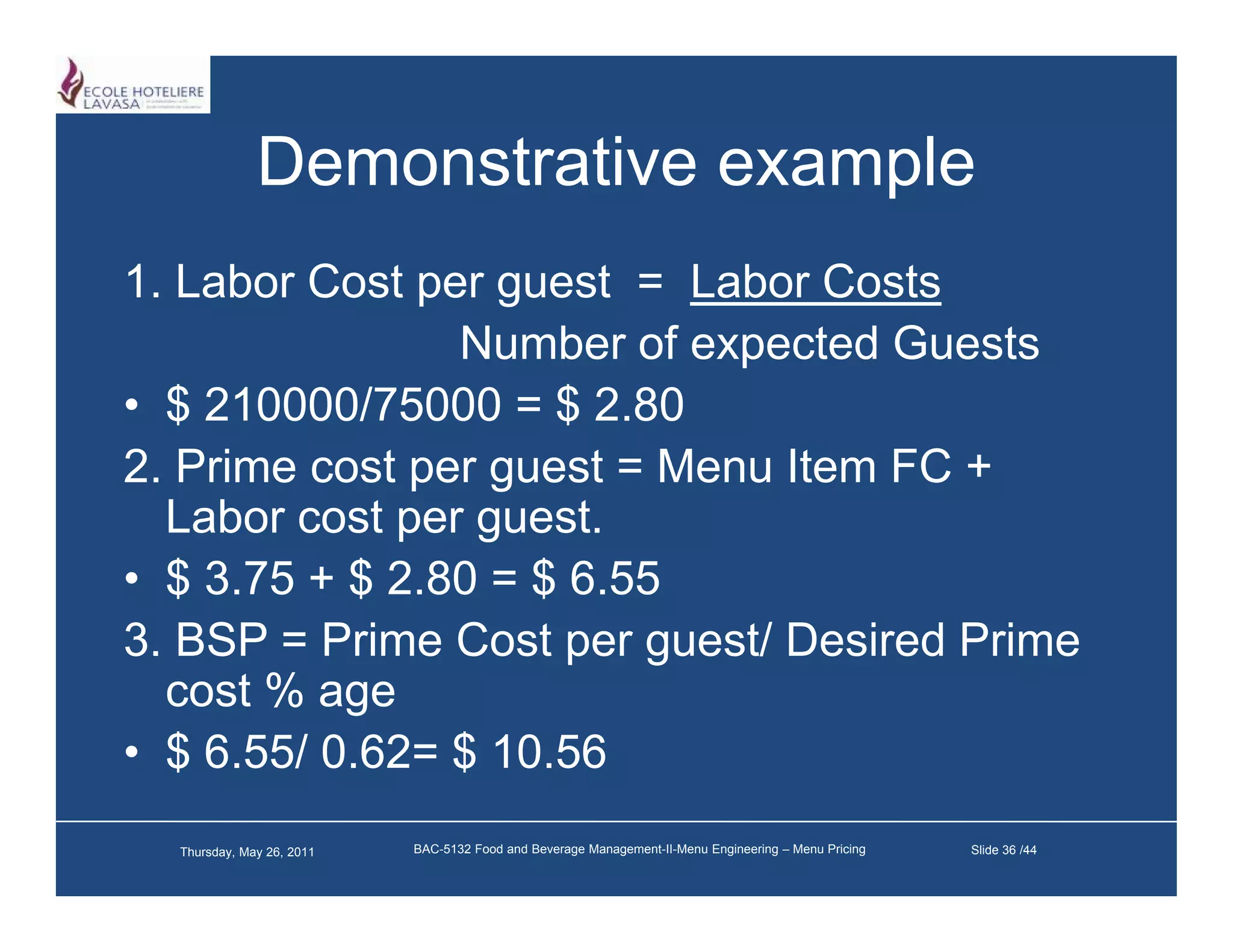

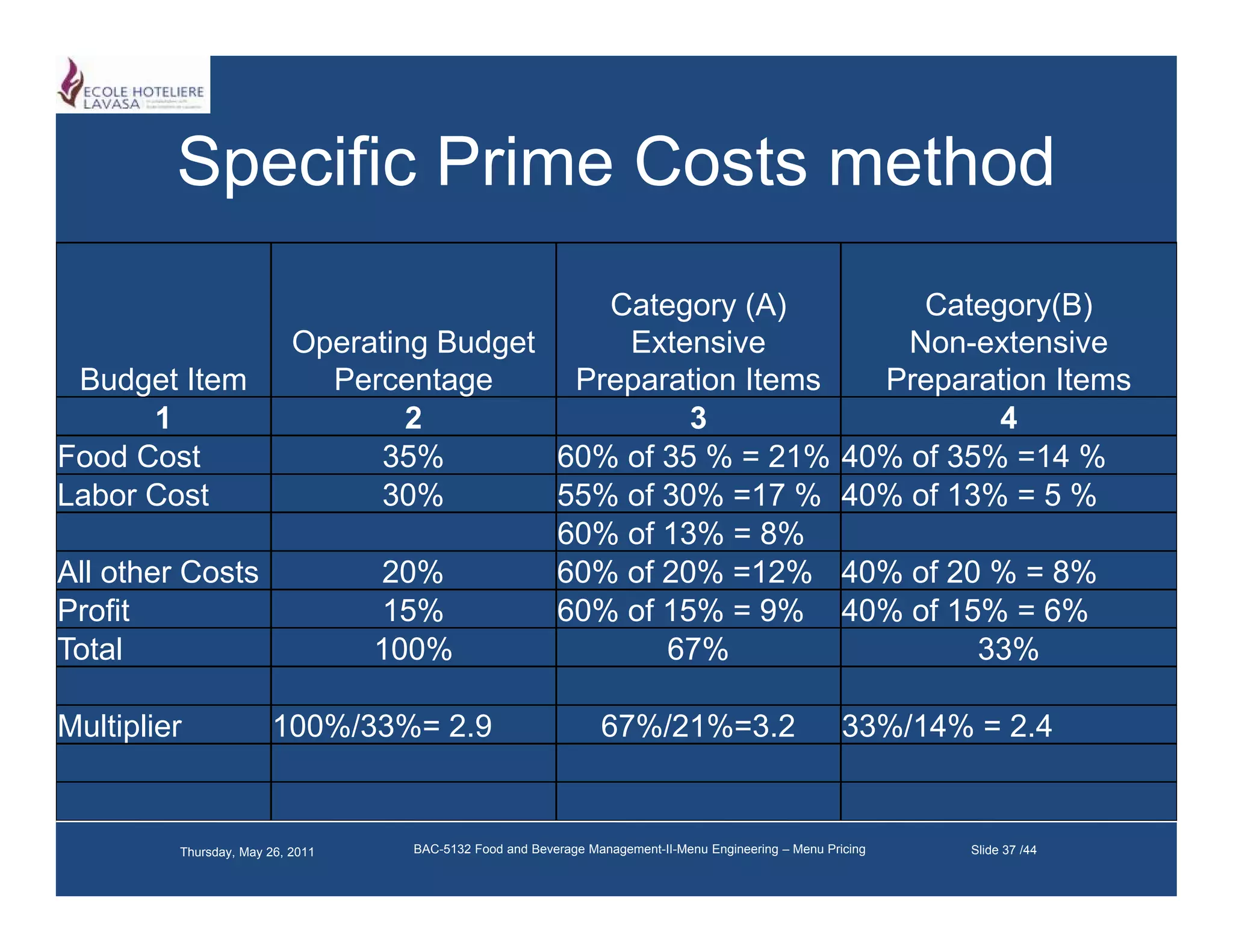

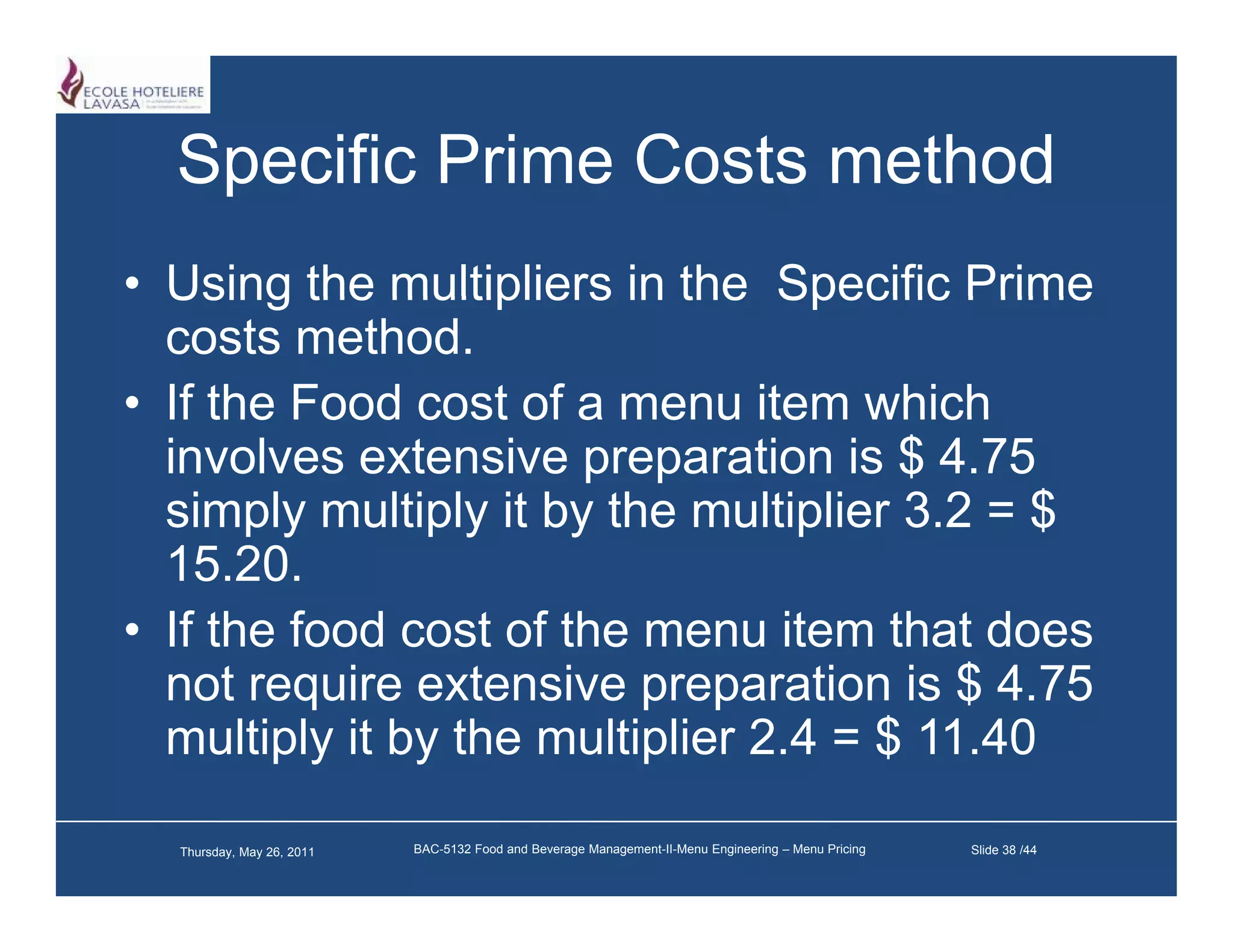

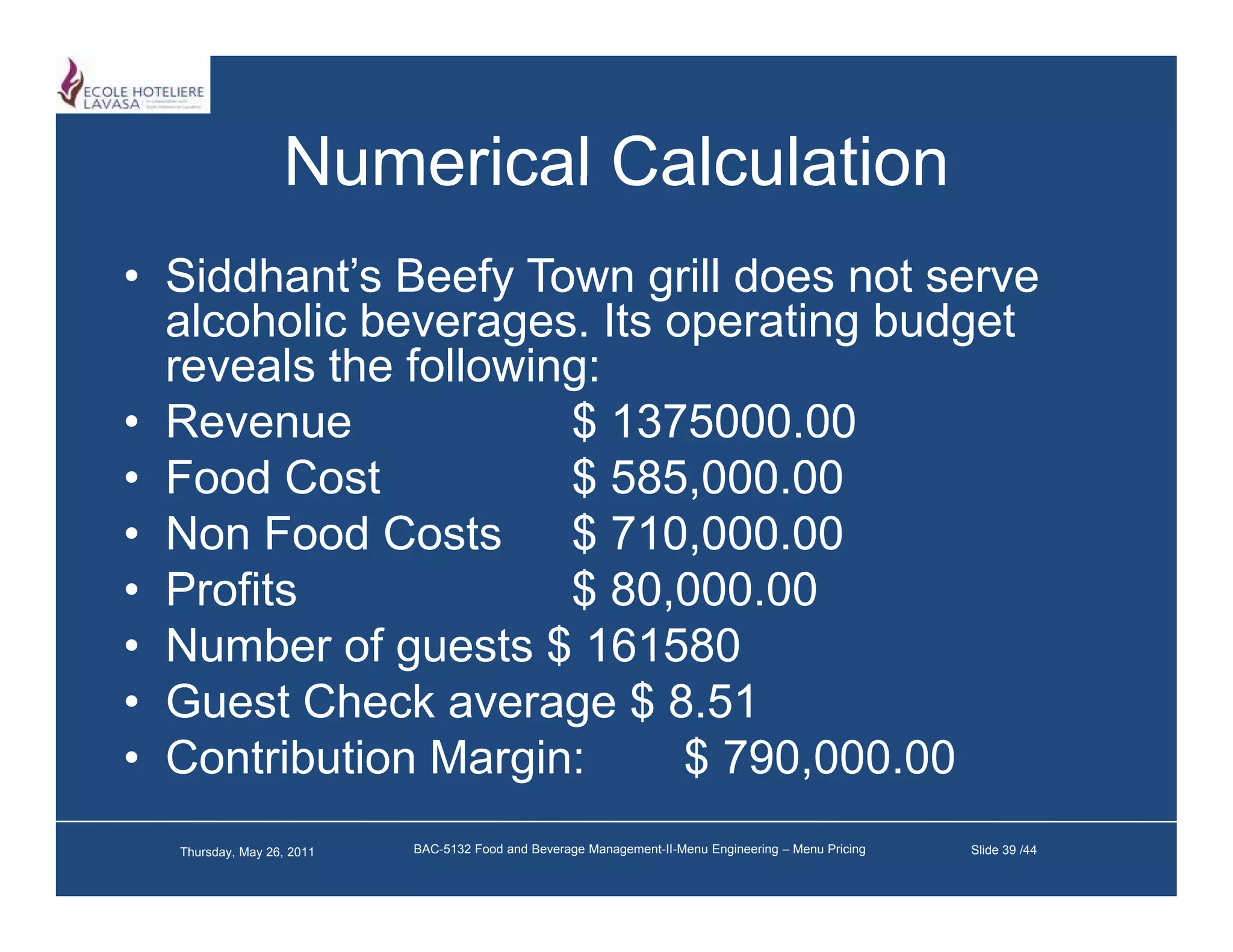

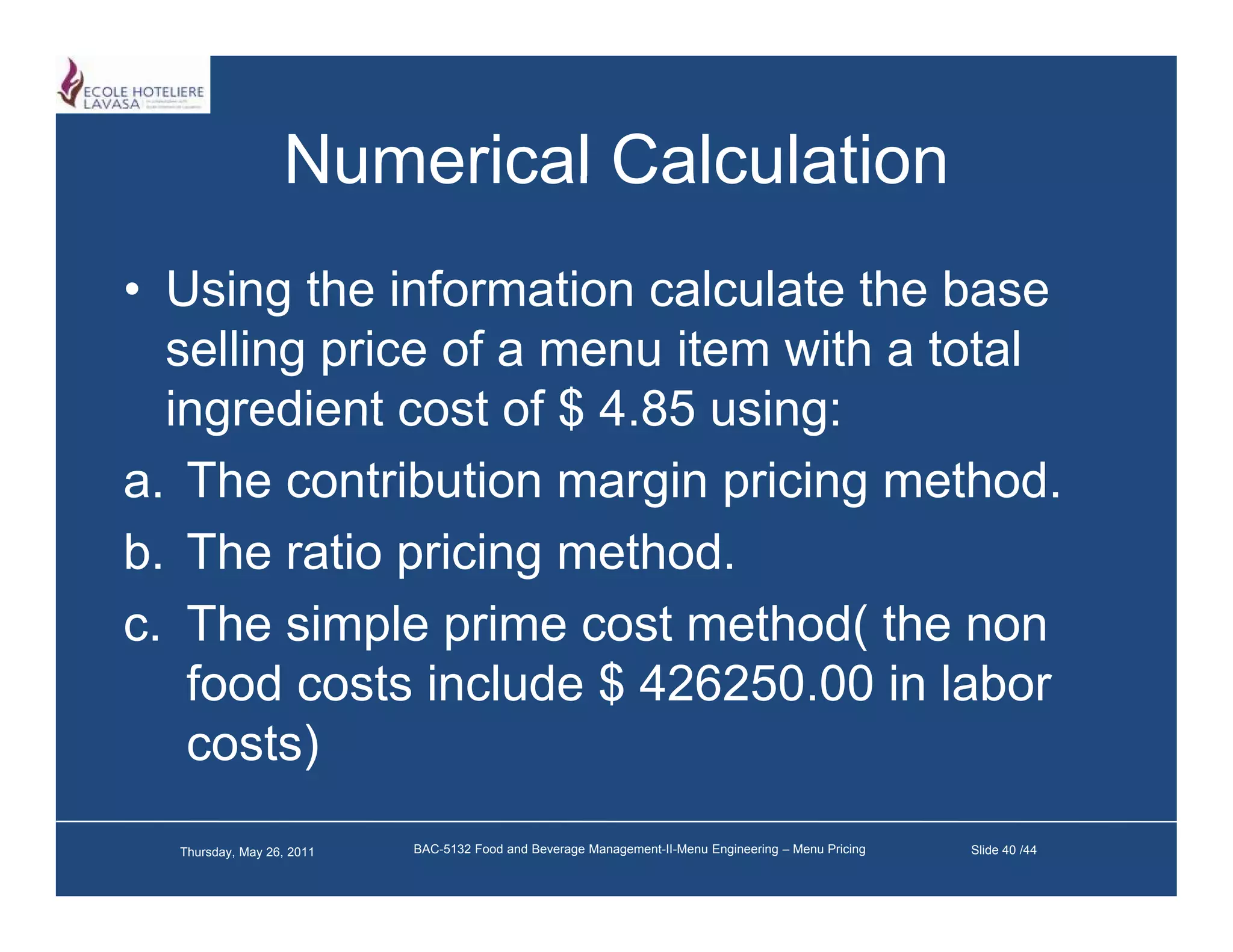

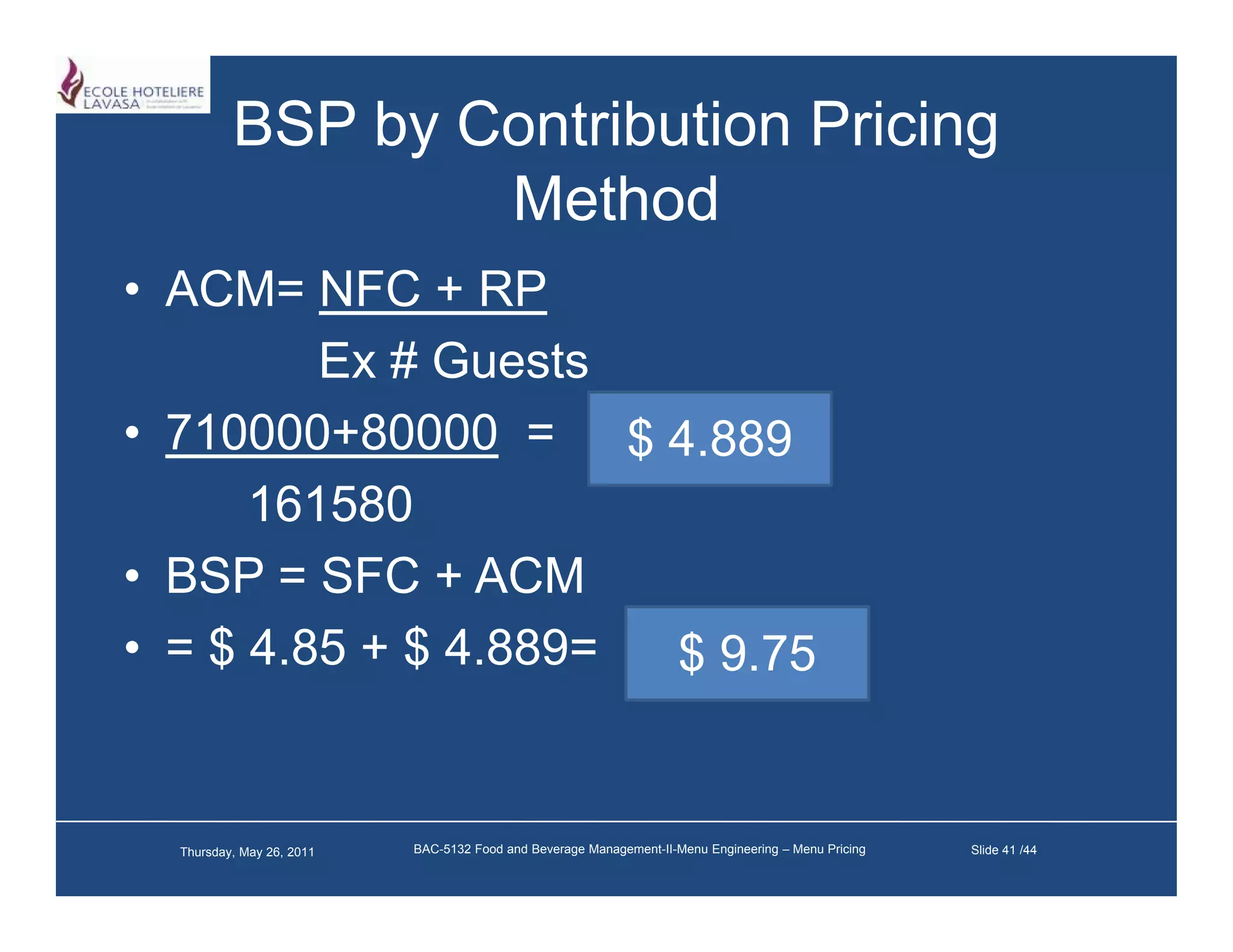

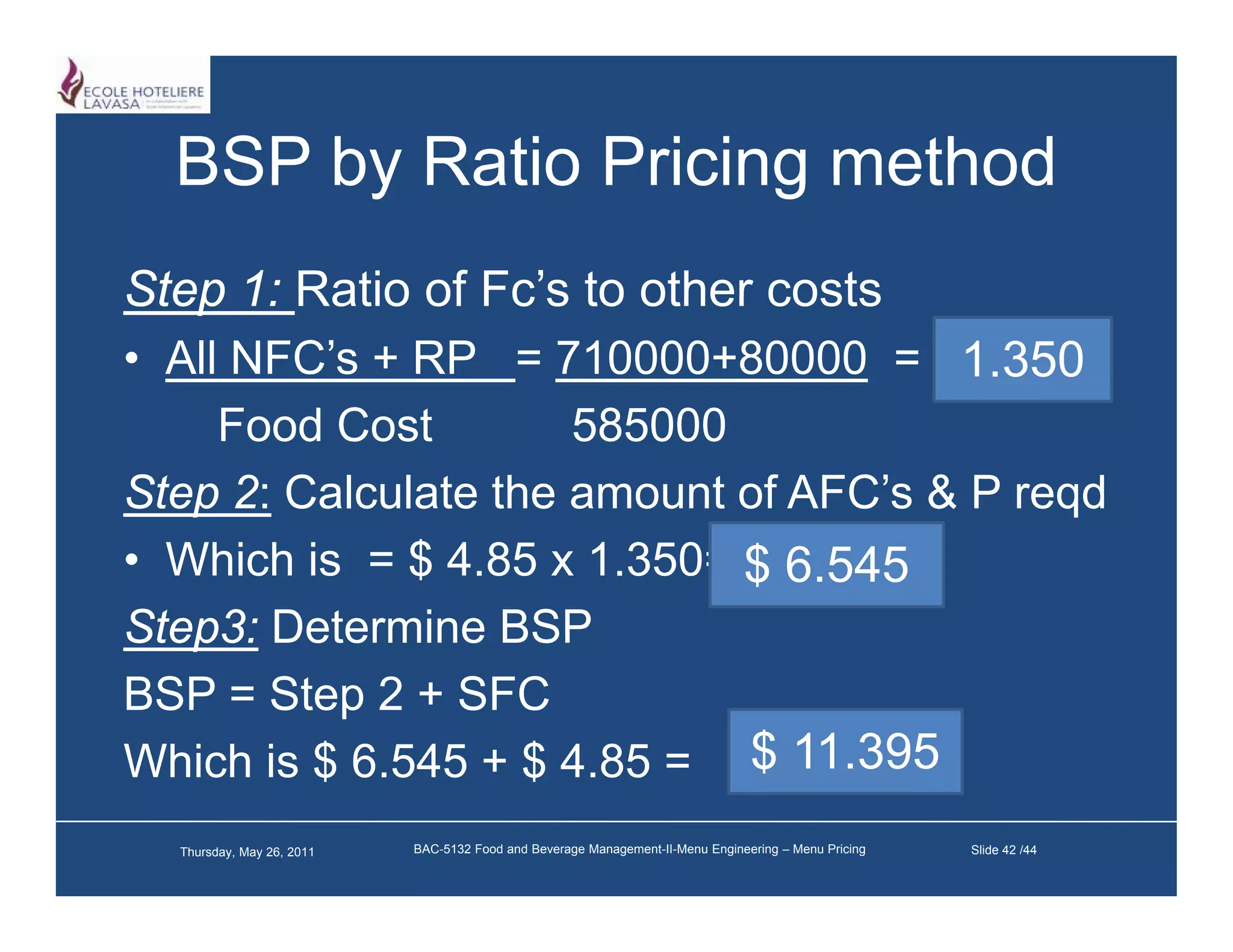

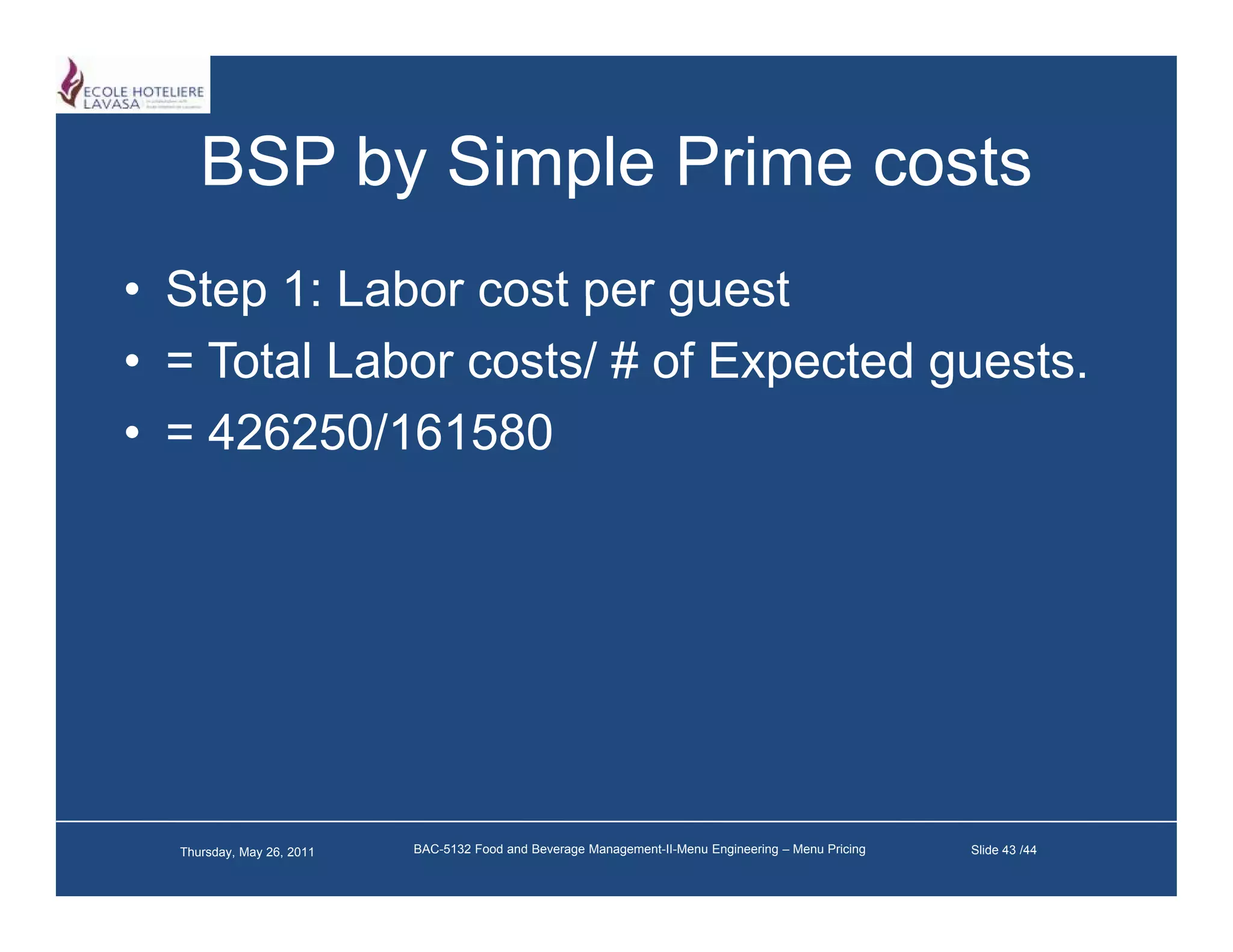

The document discusses various methods for pricing menus, including subjective and objective approaches. Subjective methods are based on assumptions rather than cost analysis, while objective methods use cost data and budgets. Specific pricing methods covered include ingredient markup, prime ingredient markup, markup with accompaniment costs, contribution margin, and ratio pricing. Formulas are provided for calculating multipliers and base selling prices under different methods.

![Menu the foundation for control [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/menuthefoundationforcontrolcompatibilitymode-130708052052-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Facilities design, décor and cleaning [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/facilitiesdesigndcorandcleaningcompatibilitymode-131126044615-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Security and the lodging industry [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/securityandthelodgingindustrycompatibilitymode-130119023537-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![The challenge of f&b operations [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/thechallengeoffboperationscompatibilitymode-130116220357-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)