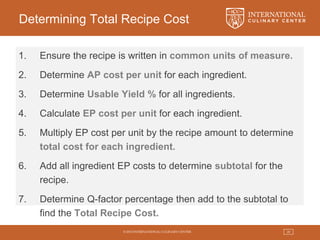

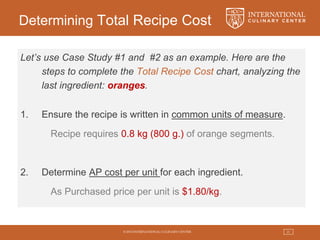

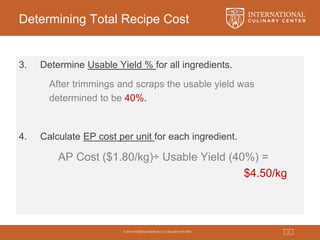

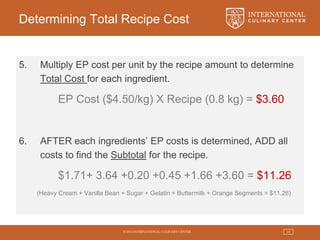

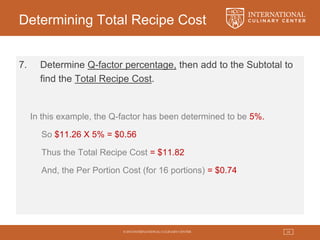

The document discusses key concepts in food costing and cost control for chefs. It explains how to perform basic food costing calculations to determine costs at various stages from purchase to finished dish. This includes determining the usable yield percentage, edible portion cost, and total recipe cost. The total recipe cost is used to estimate the minimum selling price required to meet the target food cost percentage. Standardizing recipes, tracking costs, and understanding yields and markups is important for financial management in the food business.