This document provides an overview of key concepts related to demand, including:

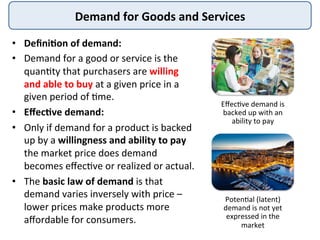

- The definition of demand as the quantity willing and able to be purchased at a given price.

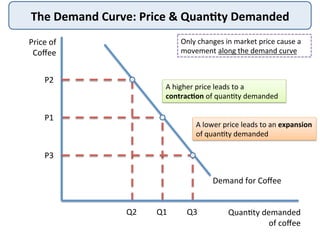

- How the demand curve illustrates the inverse relationship between price and quantity demanded.

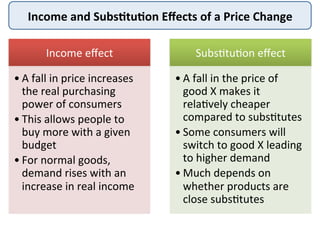

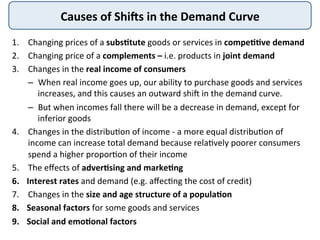

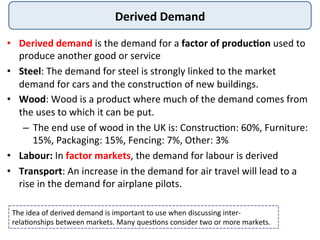

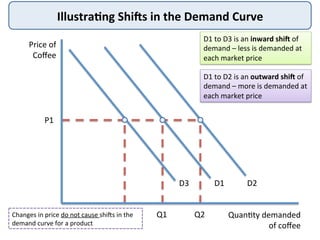

- Factors that can cause a shift in the demand curve, such as changes in income, prices of substitutes/complements, and non-economic factors.

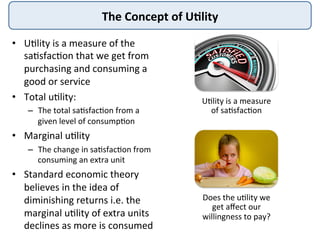

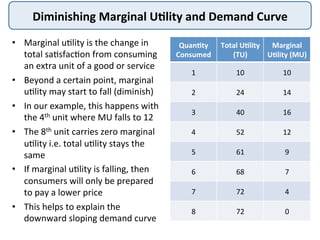

- The concept of utility and how the principle of diminishing marginal utility helps explain the downward slope of the demand curve.