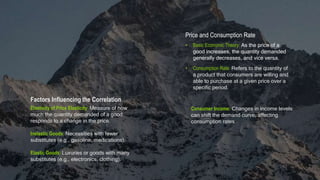

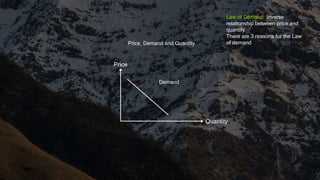

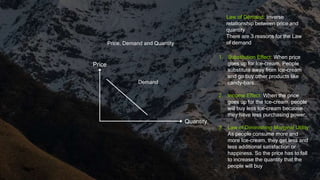

The document discusses the relationship between price and consumption rates, emphasizing the importance of correlation in understanding consumer behavior and economic forecasting. It covers factors influencing elasticity of demand, such as price changes, consumer income, and the distinction between necessities and luxuries. Additionally, it explains the law of demand, detailing the factors that can shift demand curves, including consumer preferences, number of buyers, prices of related goods, income, and expectations.

![Microeconomic_Basic_Concepts_&_Principals[1] - Read-Only](https://cdn.slidesharecdn.com/ss_thumbnails/microeconomicbasicconceptsprincipals1-read-only-240514160329-bf7b4dd3-thumbnail.jpg?width=640&height=640&fit=bounds)