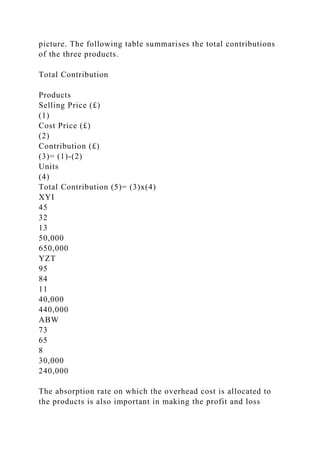

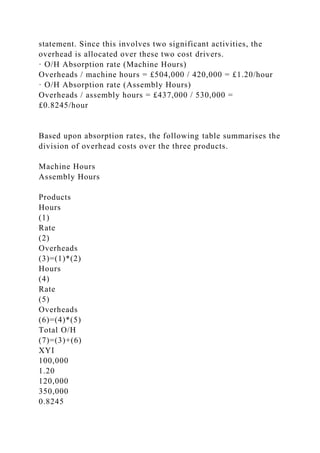

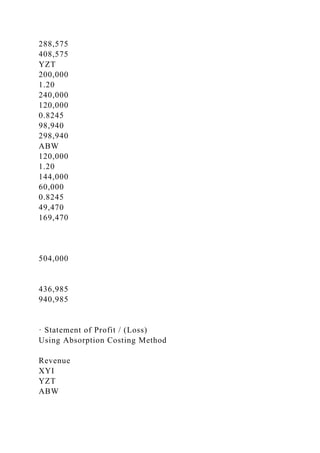

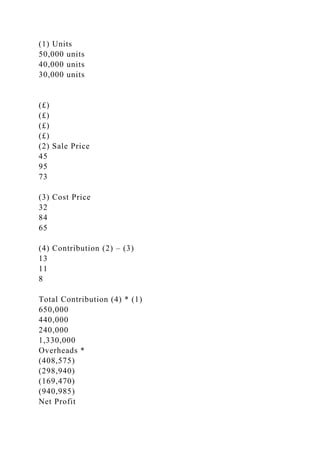

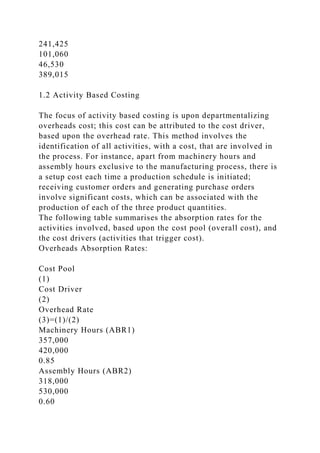

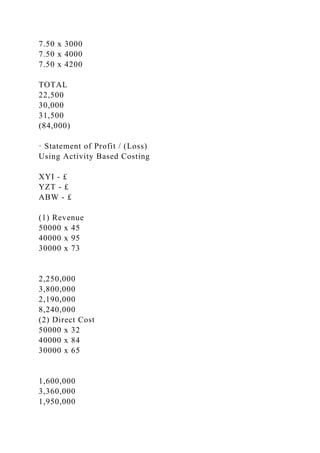

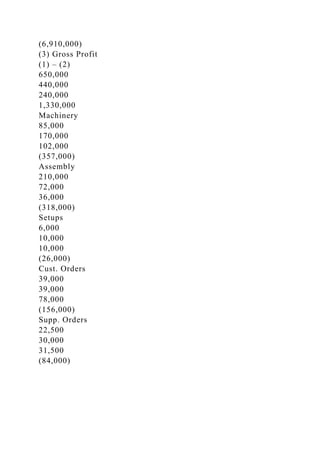

The document compares absorption costing and activity-based costing, detailing their methodologies and impacts on budgeted profit statements. It highlights that absorption costing allocates overheads uniformly, potentially obscuring product profitability, while activity-based costing provides clearer insights by linking costs to specific activities. The analysis reveals significant differences in profit contributions among products, with activity-based costing saving costs and highlighting previously unnoticed losses.