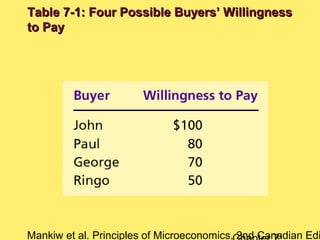

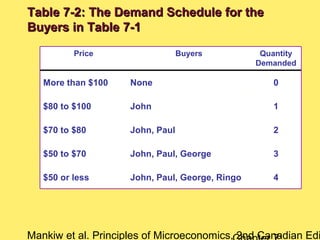

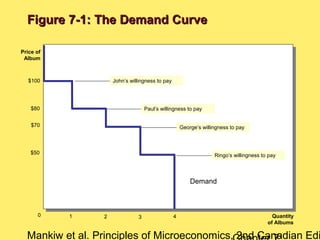

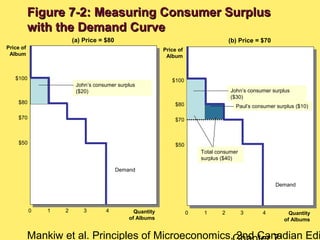

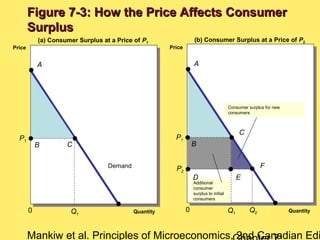

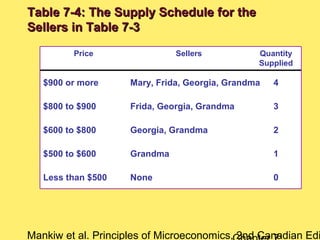

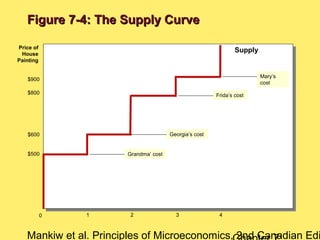

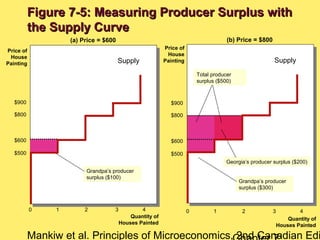

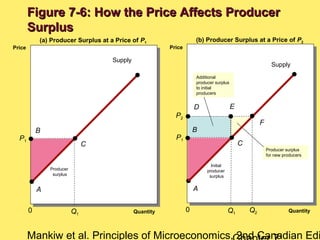

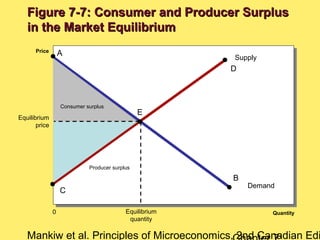

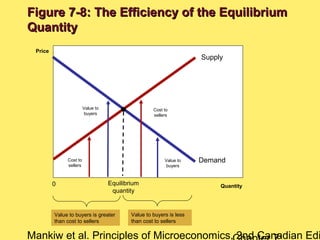

This chapter discusses consumer surplus, producer surplus, and market efficiency. It defines consumer surplus as the difference between what consumers are willing to pay and what they actually pay. Producer surplus is defined as the difference between what producers are paid and their costs. The market equilibrium maximizes the total surplus, which is the sum of consumer surplus and producer surplus. This allocation of resources through supply and demand is efficient because it maximizes the total benefits to both consumers and producers.