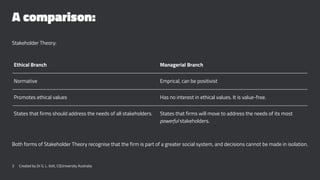

There are two branches of stakeholder theory - the ethical theory and the managerial theory. The document is primarily interested in the managerial theory. The managerial theory takes an empirical, potentially positivist approach and states that firms will address the needs of powerful stakeholders who control resources. In contrast, the ethical theory promotes ethical values and states firms should address all stakeholders' needs. The managerial theory is used to examine disclosure decisions around environmental and sustainable reporting.