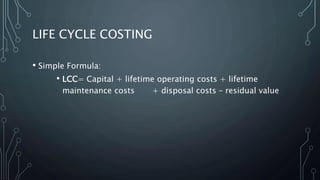

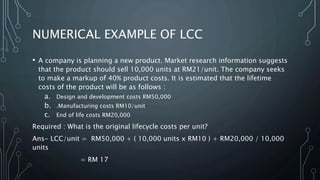

This document summarizes a student's report on life cycle costing. It defines life cycle costing as the total cost of owning an asset over its entire life, including costs of planning, design, acquisition, operation, support, and disposal. It outlines the objective to help management understand total product costs and identify areas for cost reduction. The stages of a product life cycle are defined as planning and design, manufacturing and sales, and service and abandonment. A numerical example is provided to demonstrate calculating the life cycle cost per unit for a new product.

![Presentation (13)[1] best ppt of good quality.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/presentation131-250117090038-d5d0e6fb-thumbnail.jpg?width=640&height=640&fit=bounds)