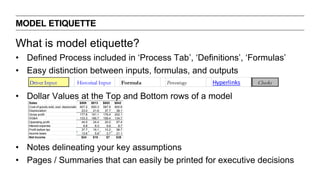

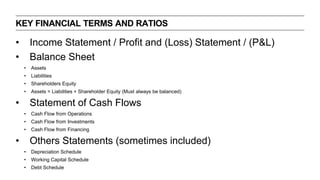

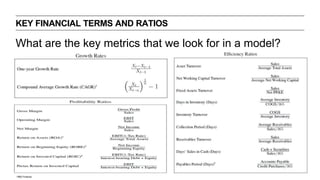

This document provides an introduction and agenda for a presentation on financial modeling. It discusses why financial models are used, who uses them, and what they can tell users. The agenda includes sections on model design and etiquette, key financial terms and ratios, an introduction to a case study, and building a basic financial model. It provides guidance on how to design models for accuracy, flexibility and usability. It also outlines important elements of model etiquette like clearly labeling inputs, formulas and outputs.