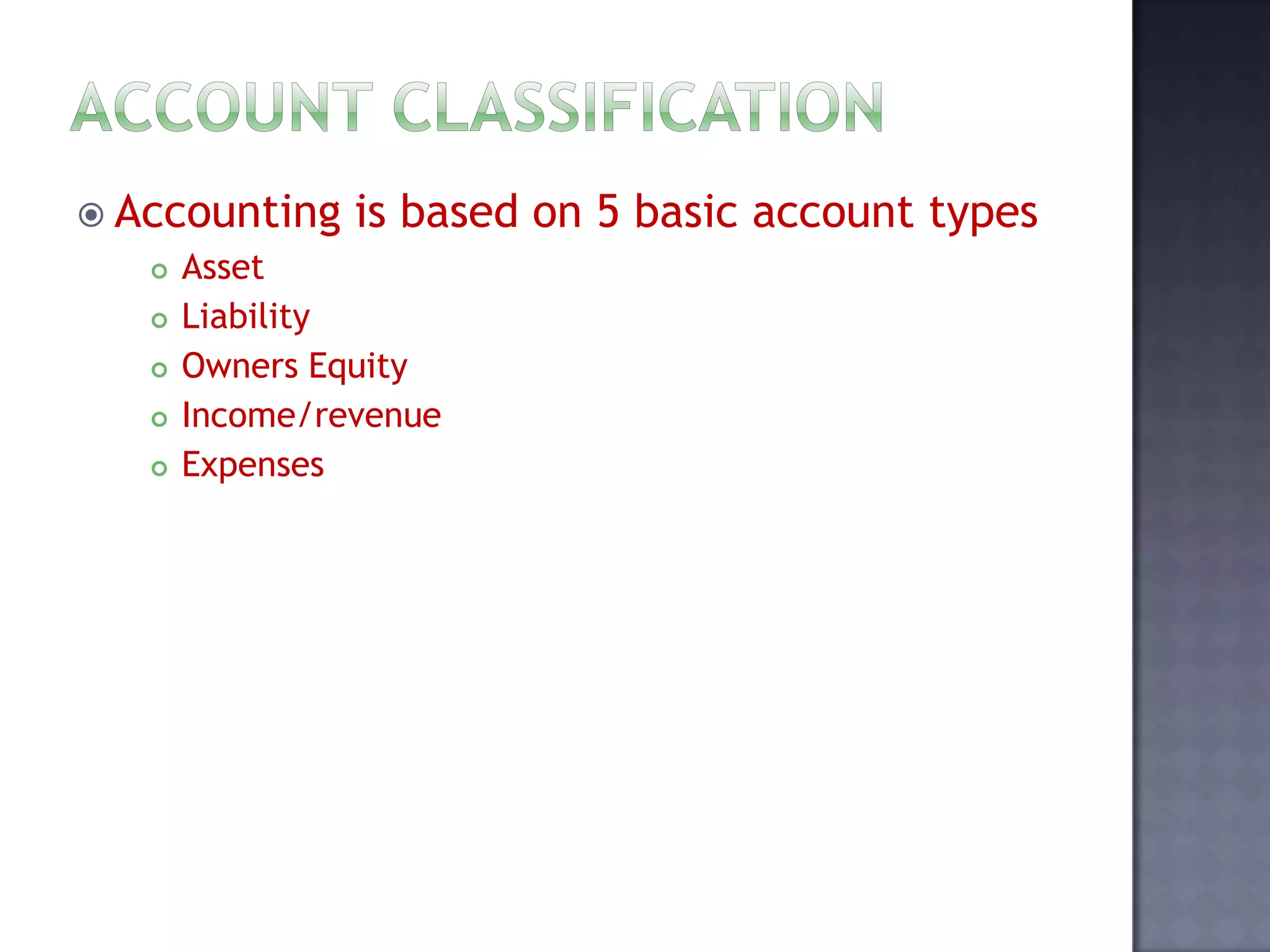

This document provides an overview of accounting concepts including the five basic account types (assets, liabilities, equity, income and expenses), the accounting equation, and who uses accounting information. Key points include:

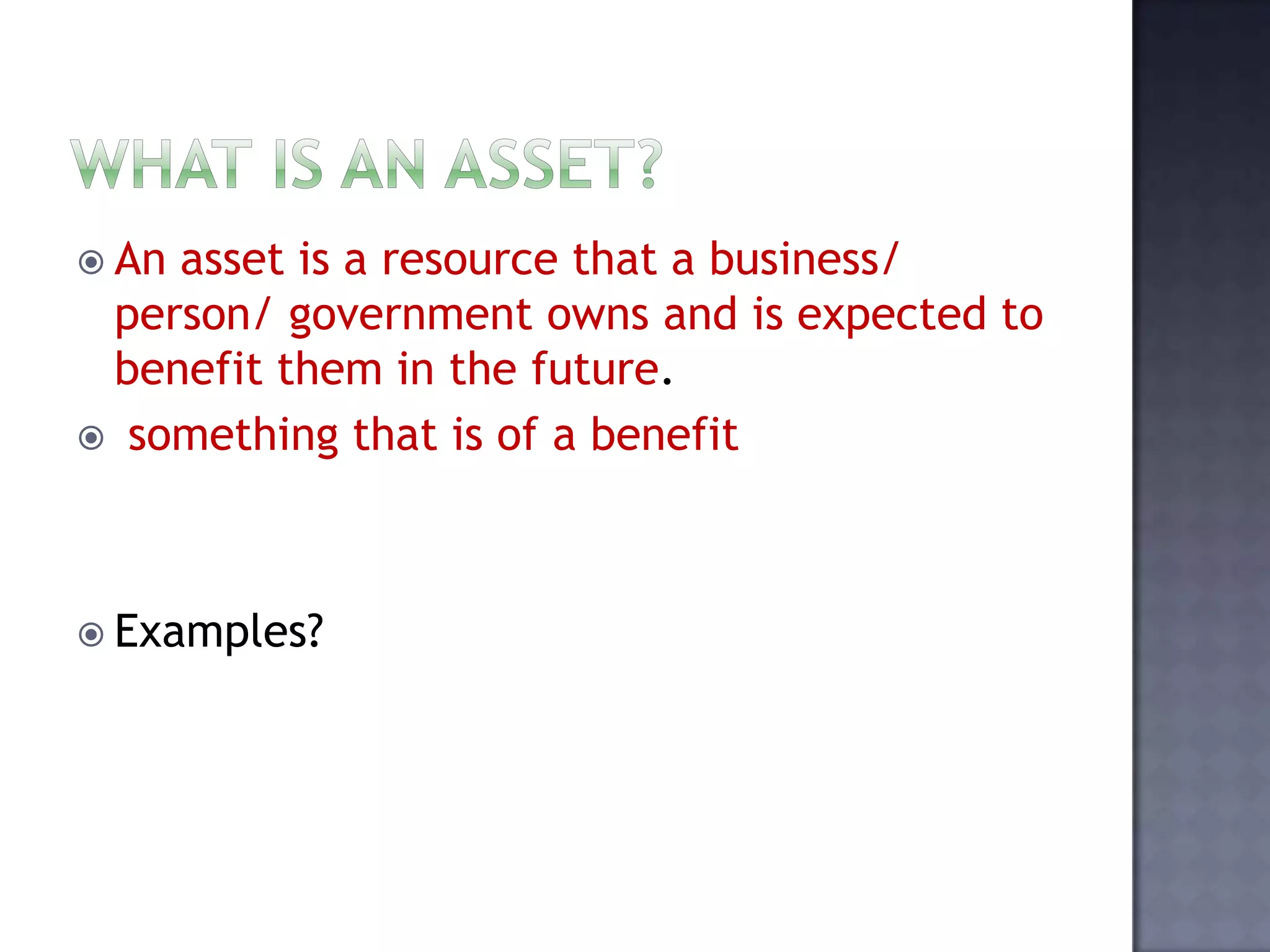

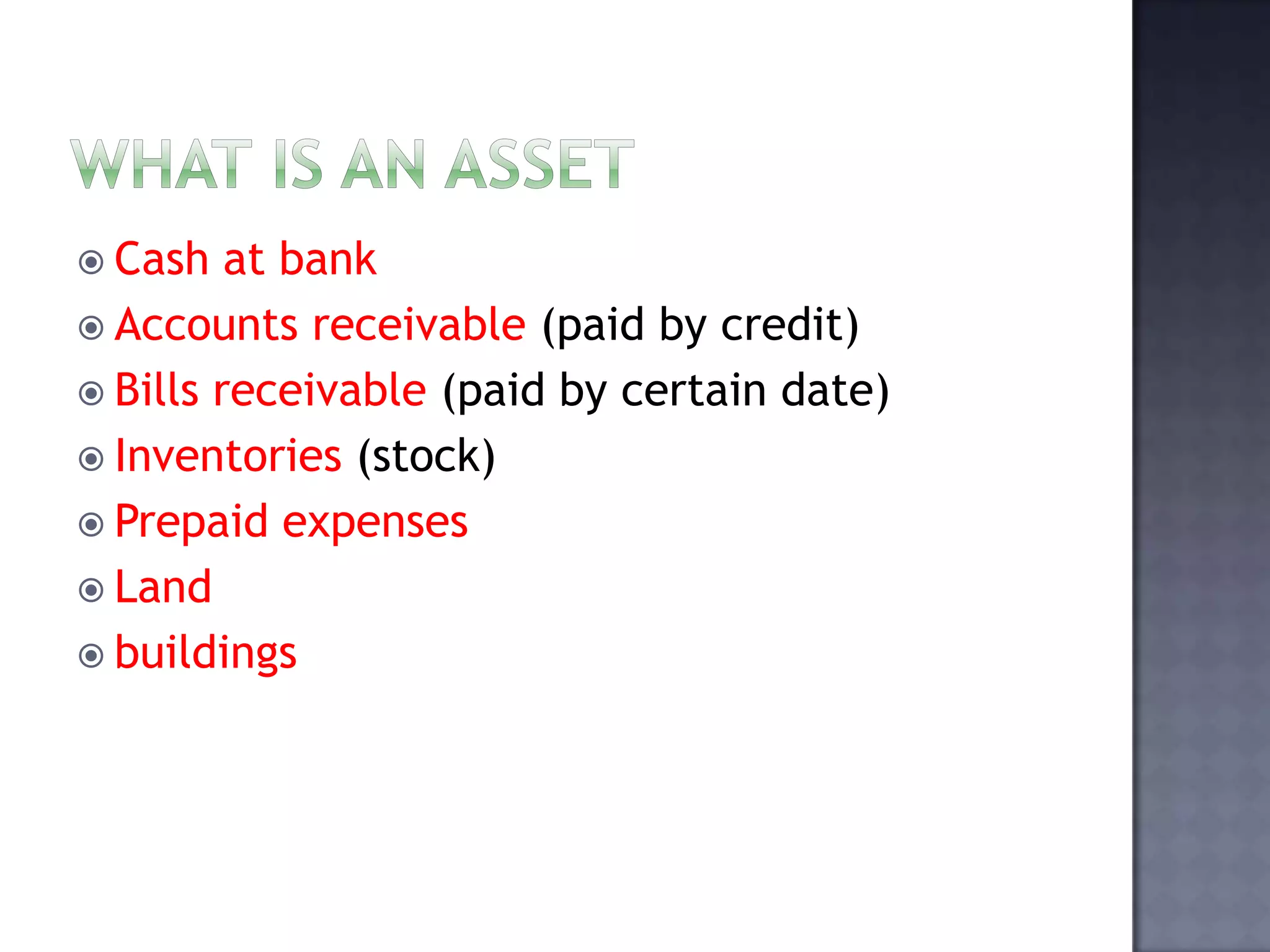

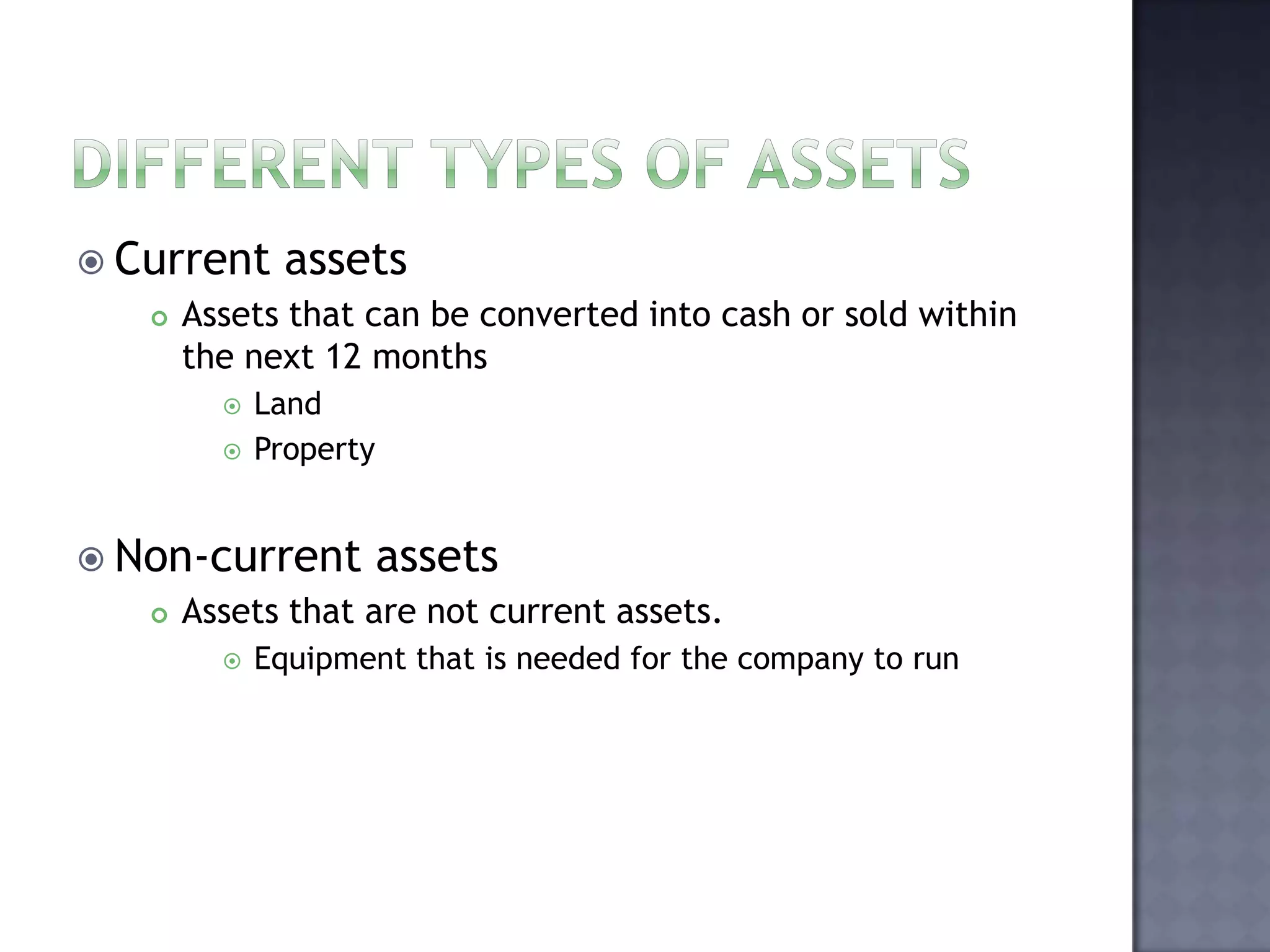

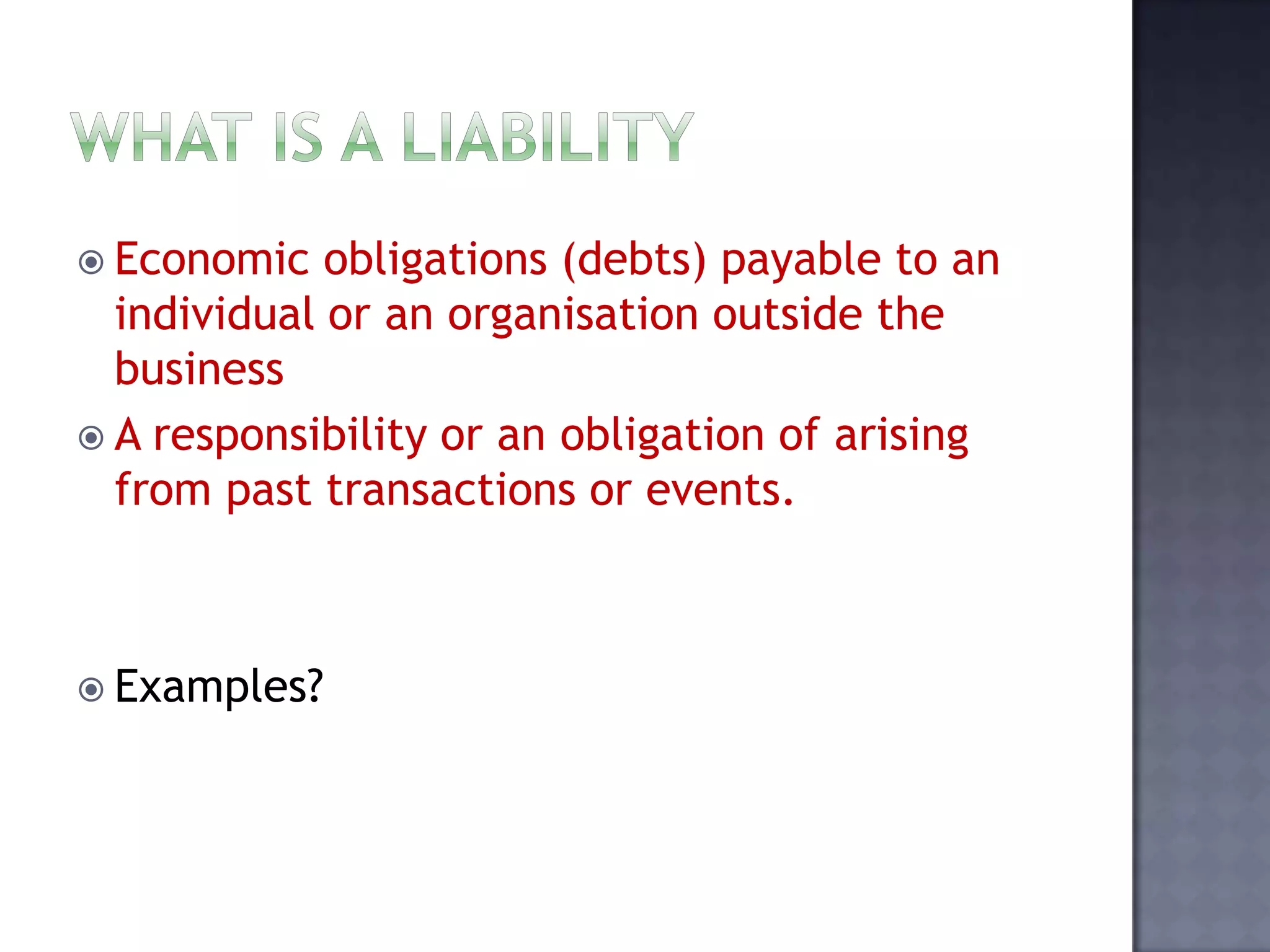

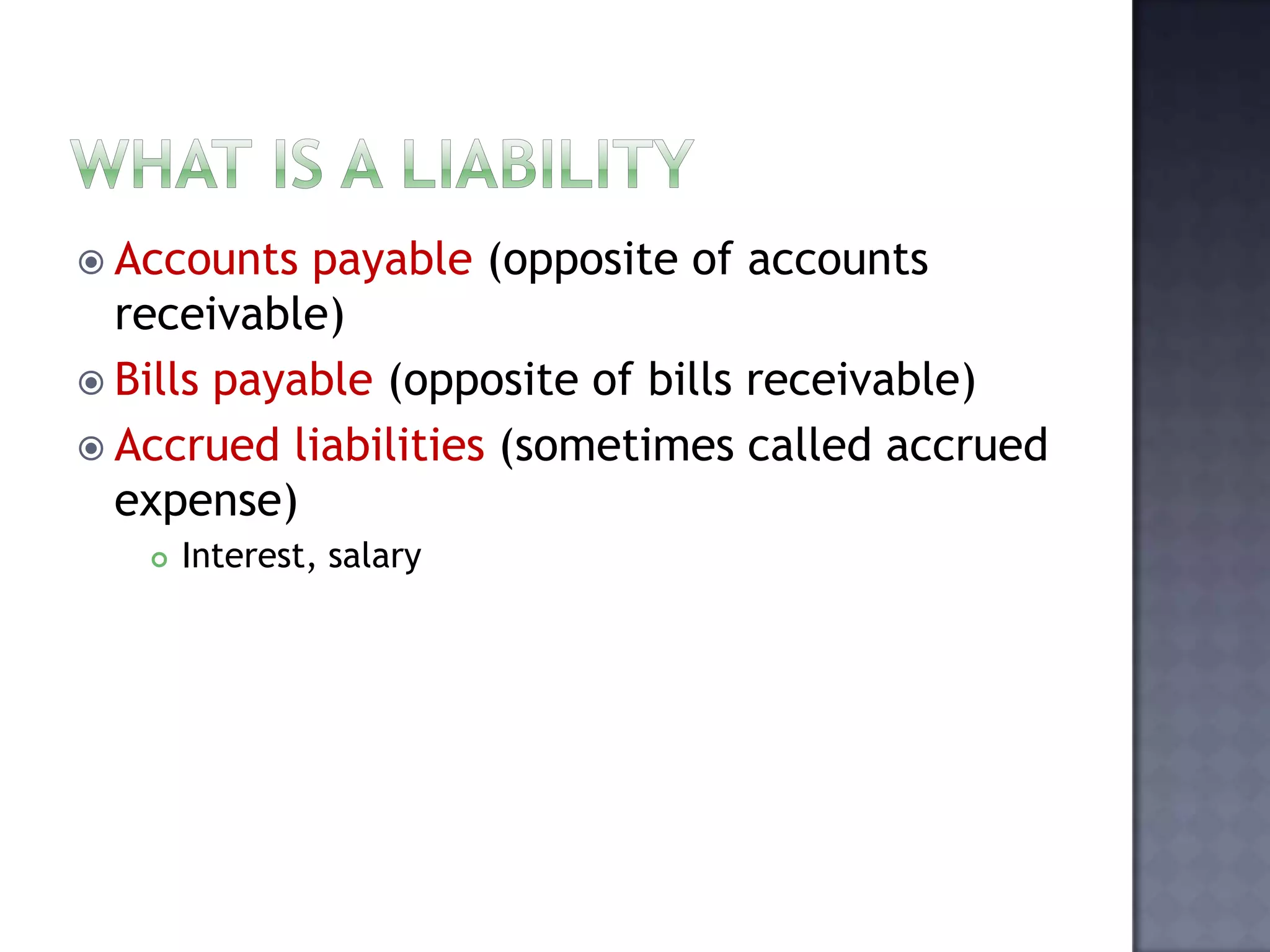

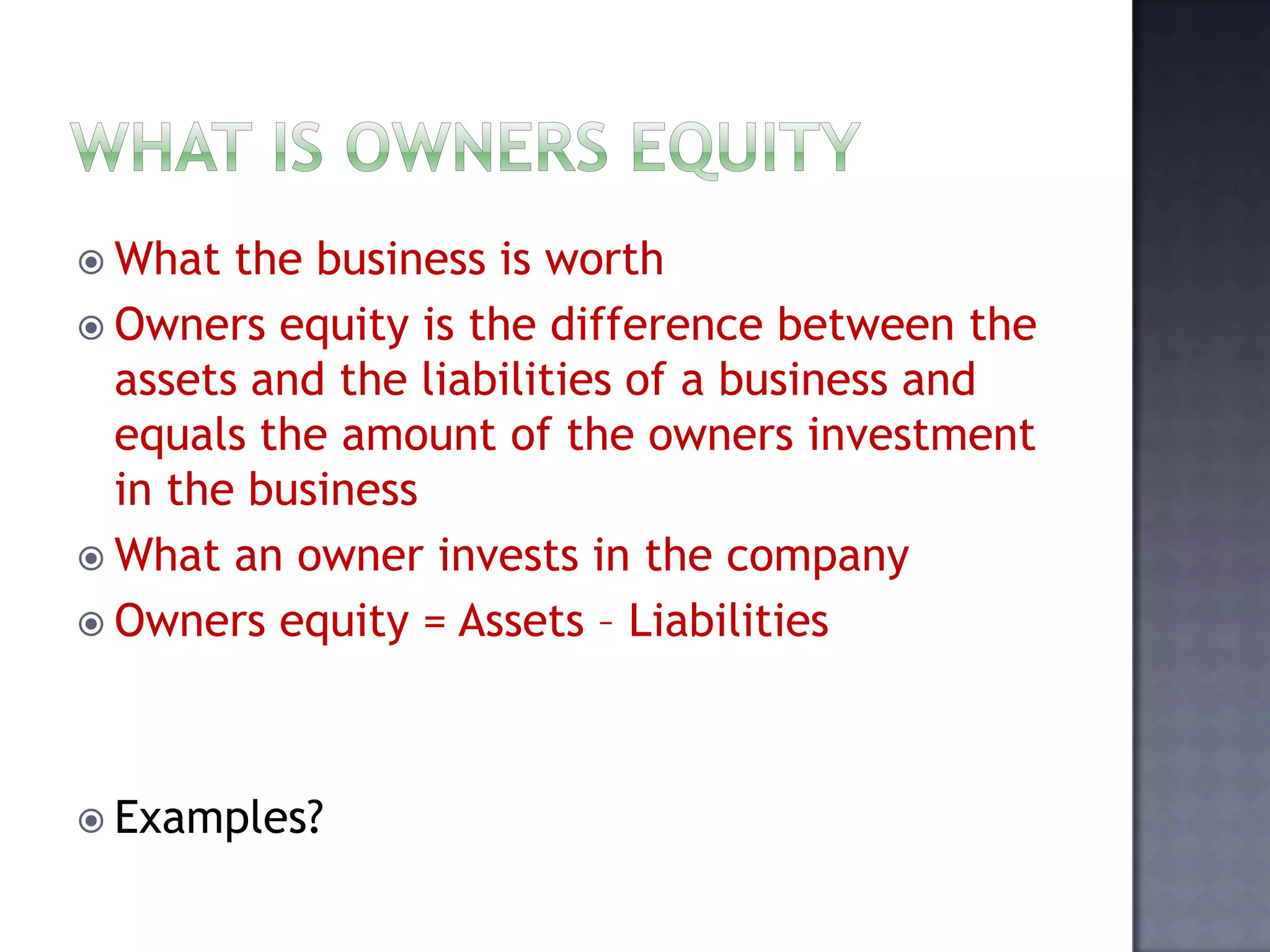

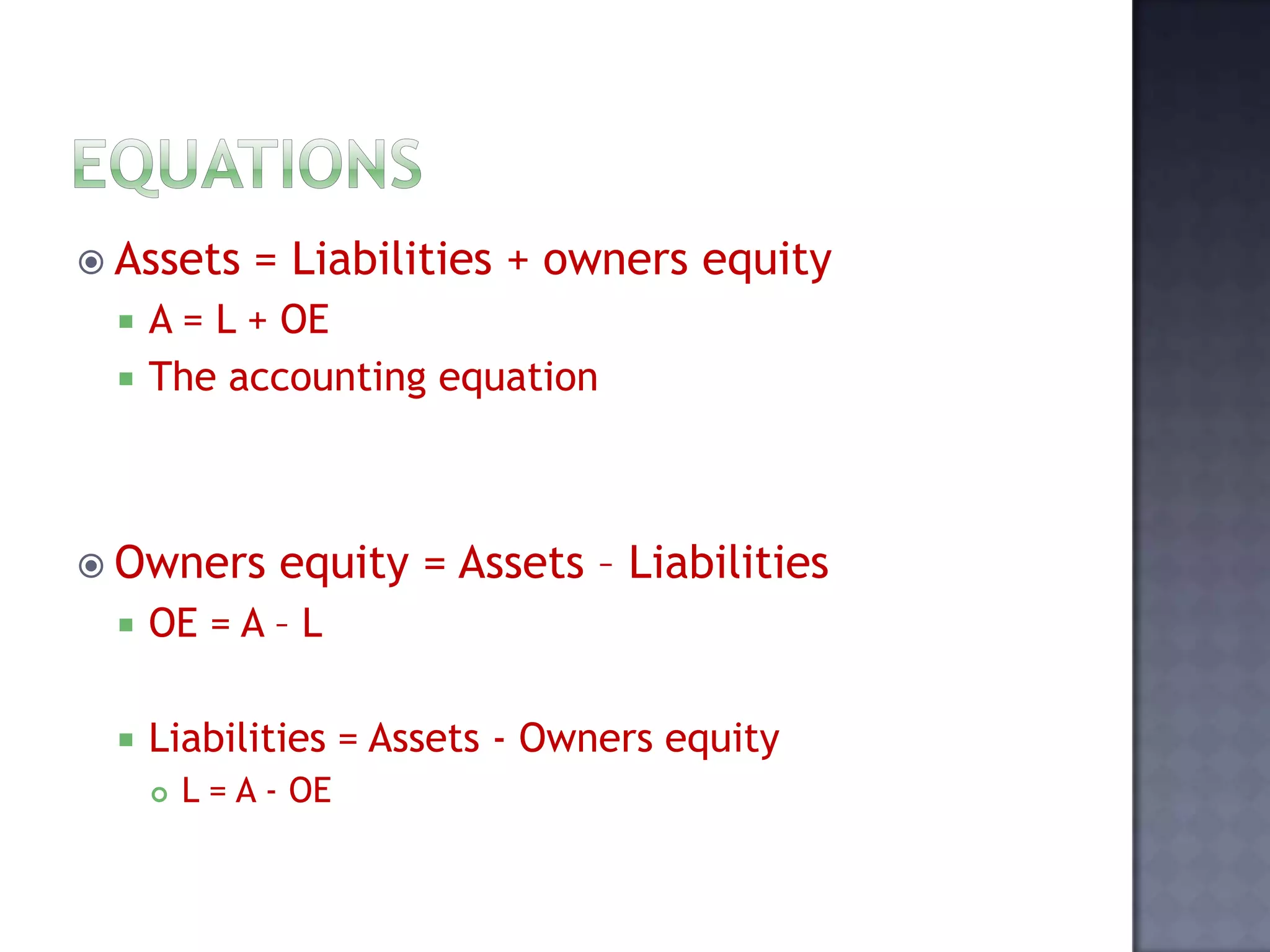

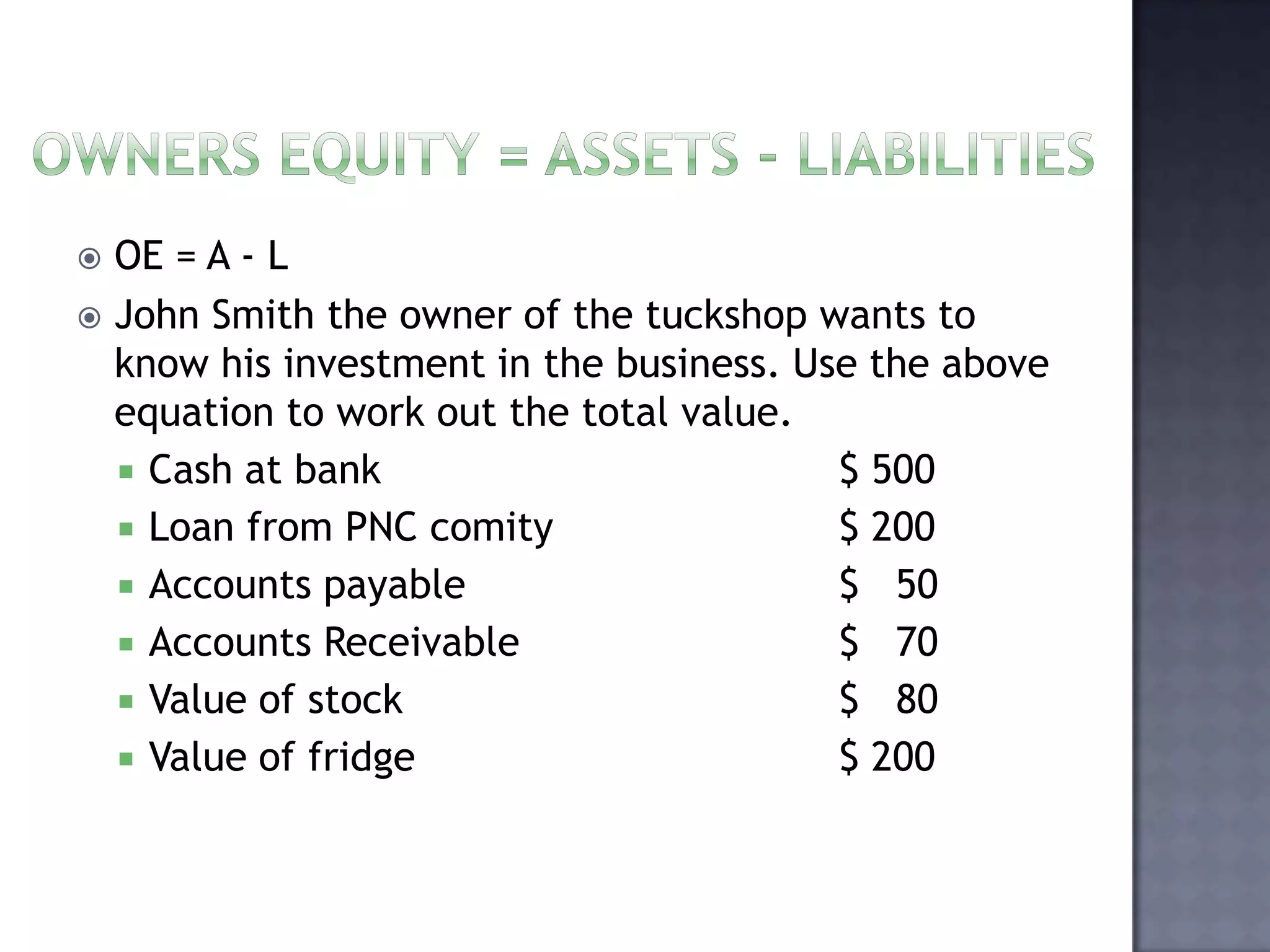

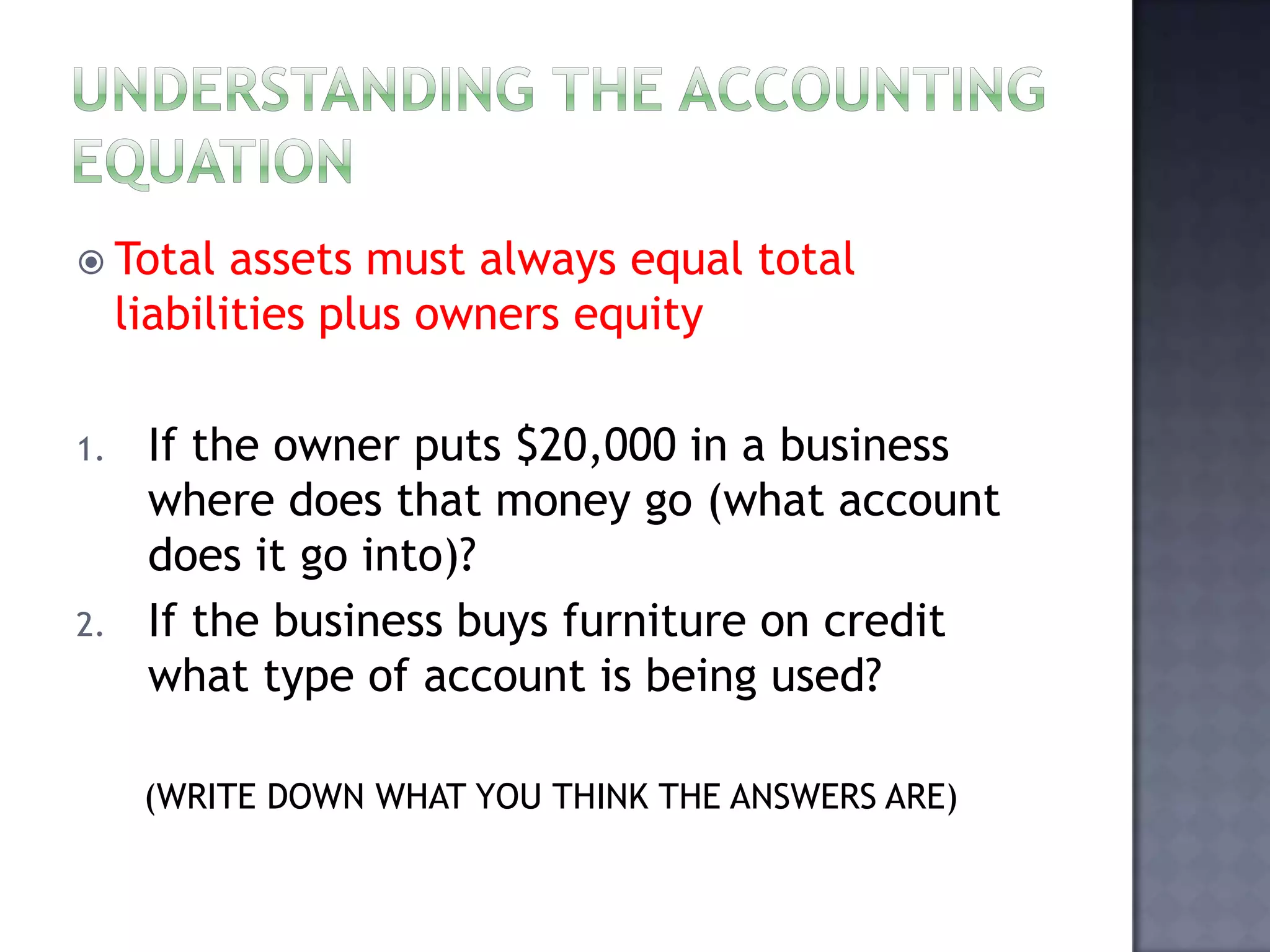

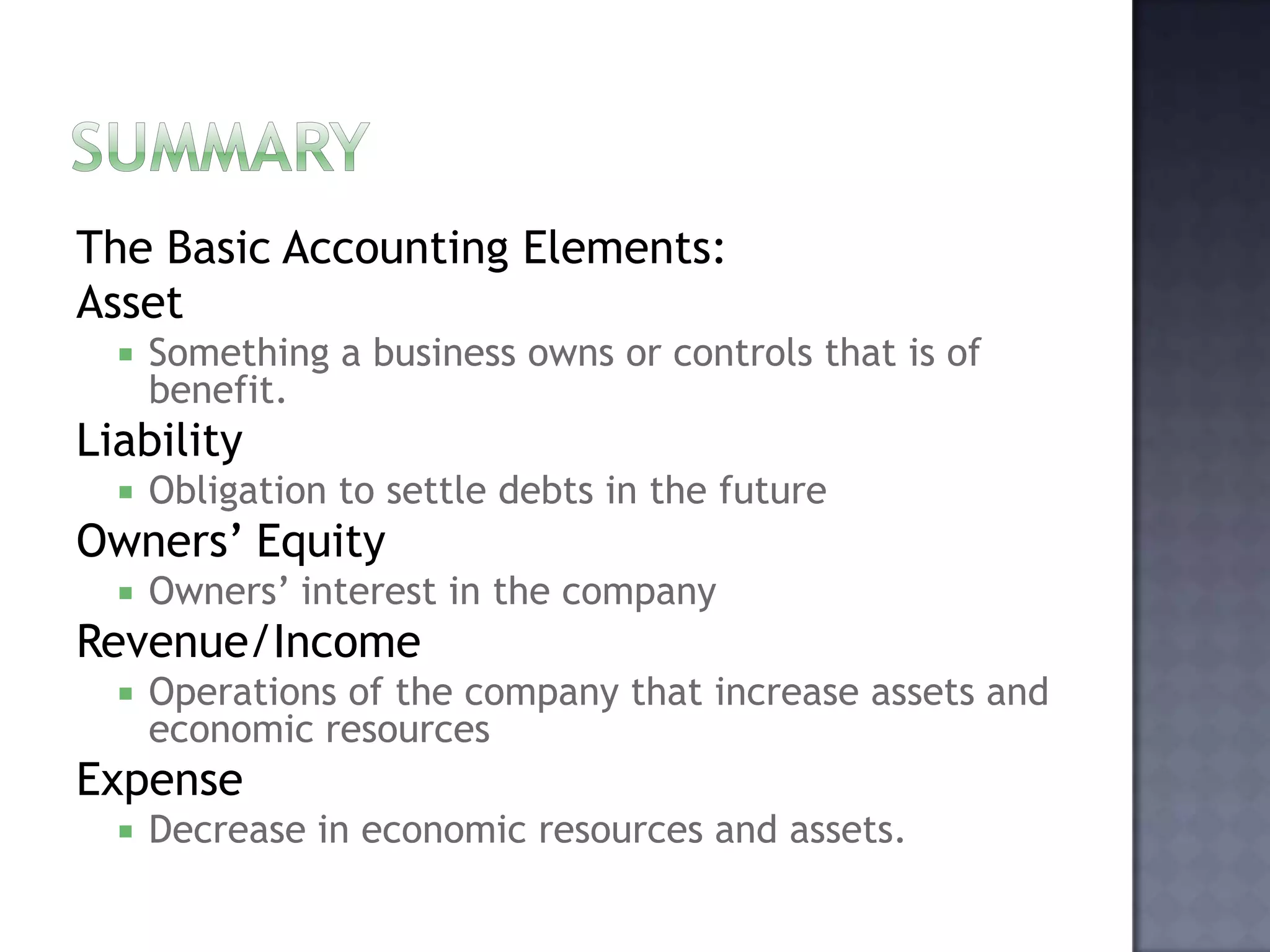

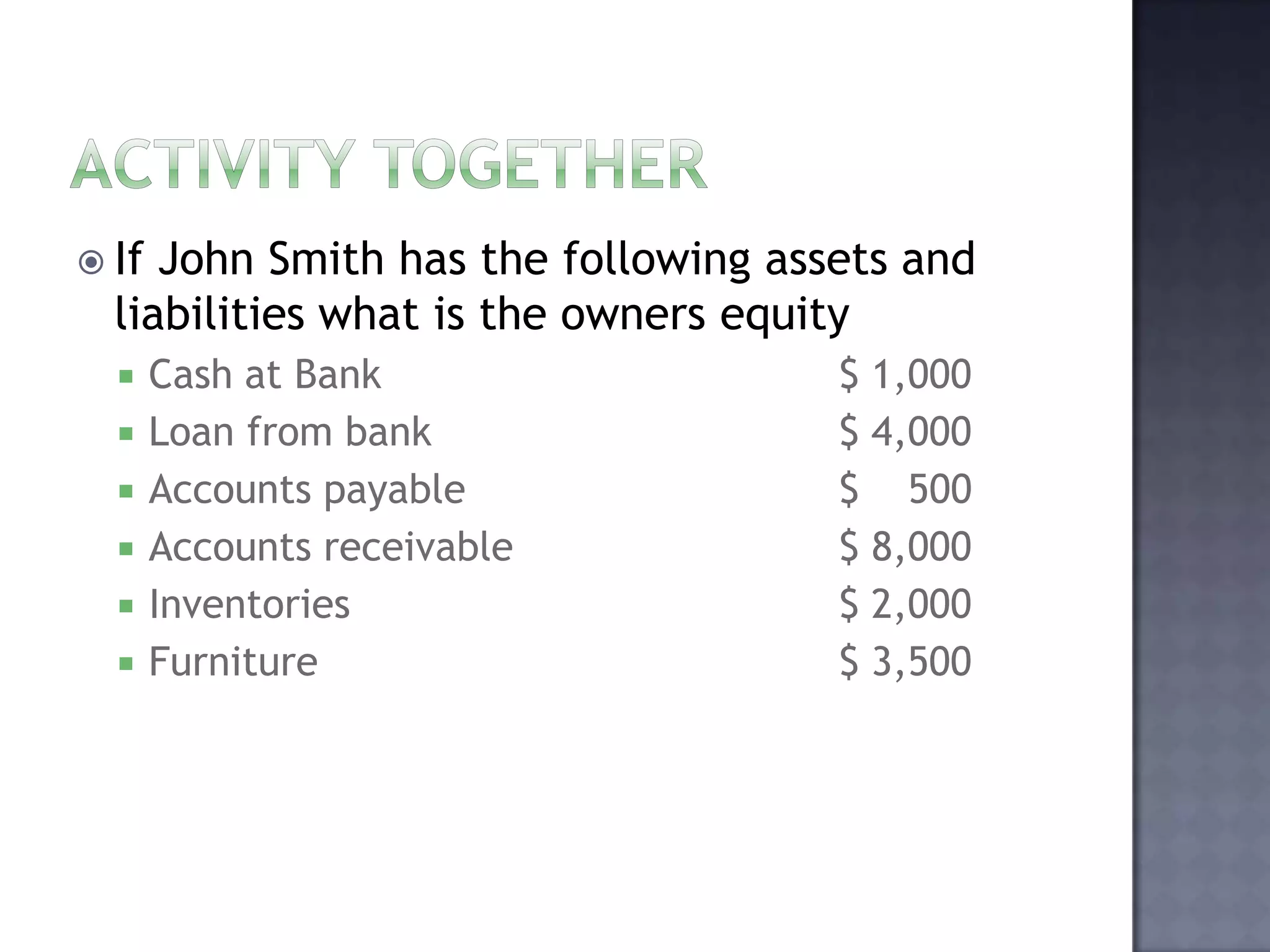

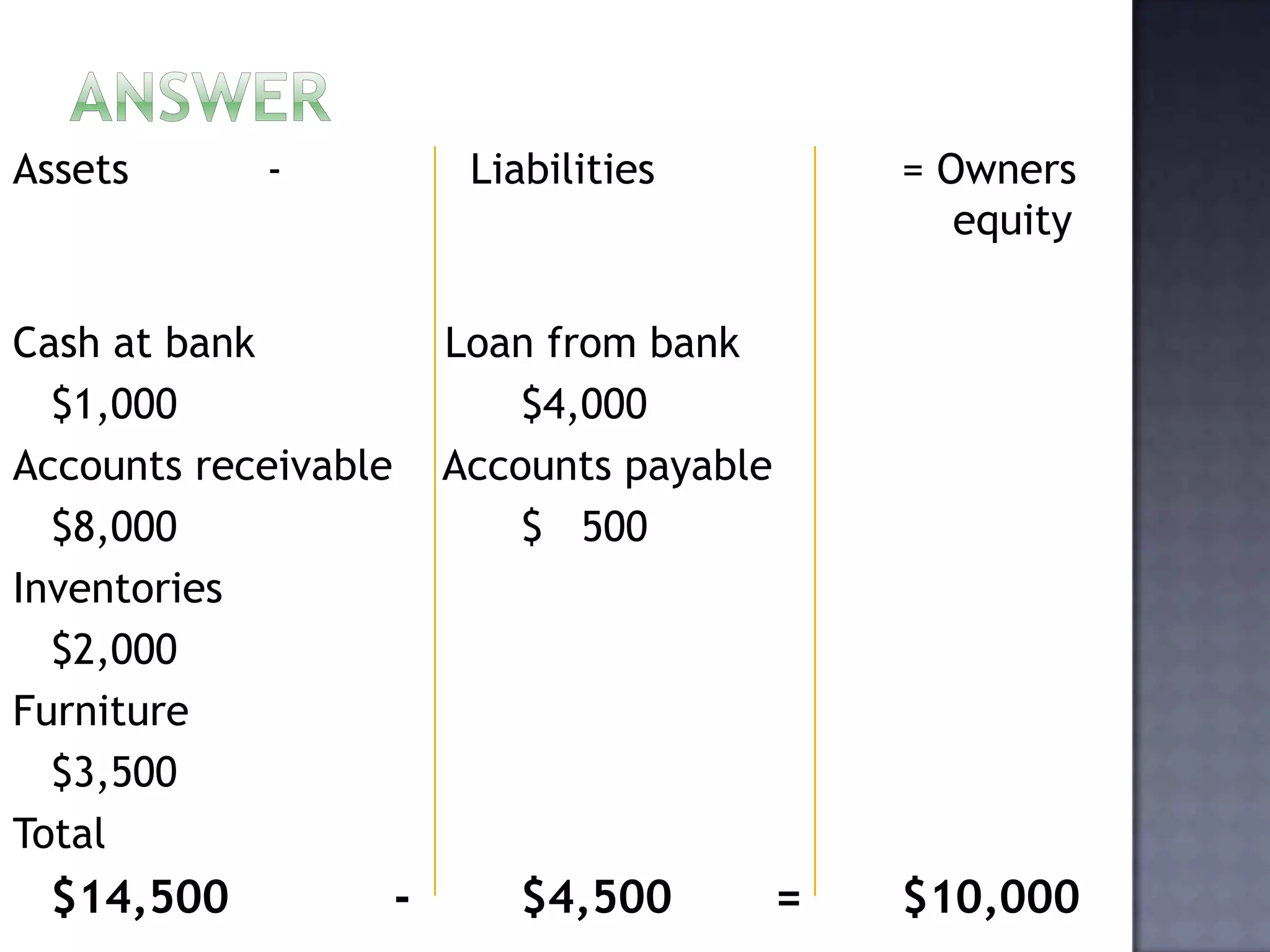

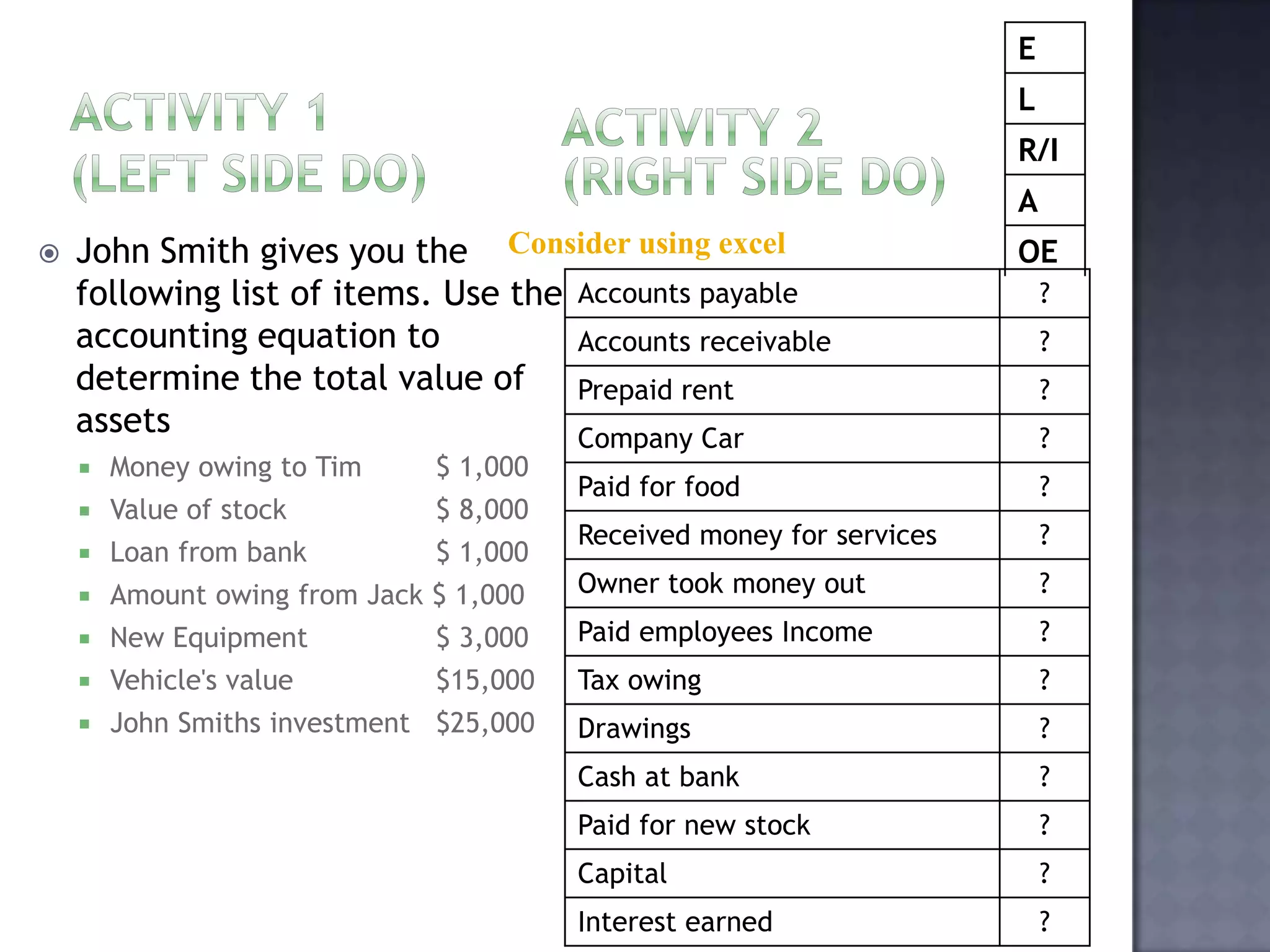

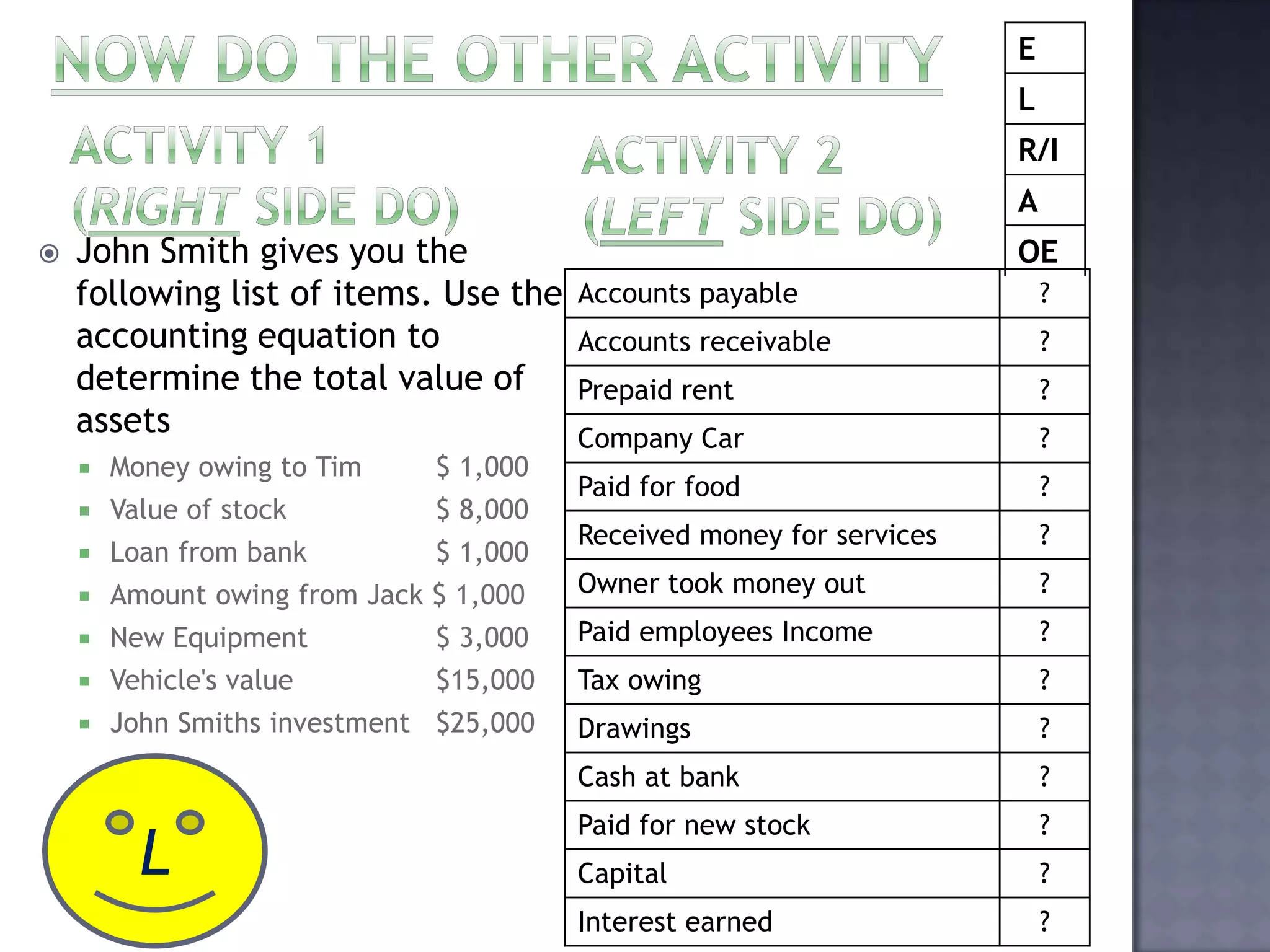

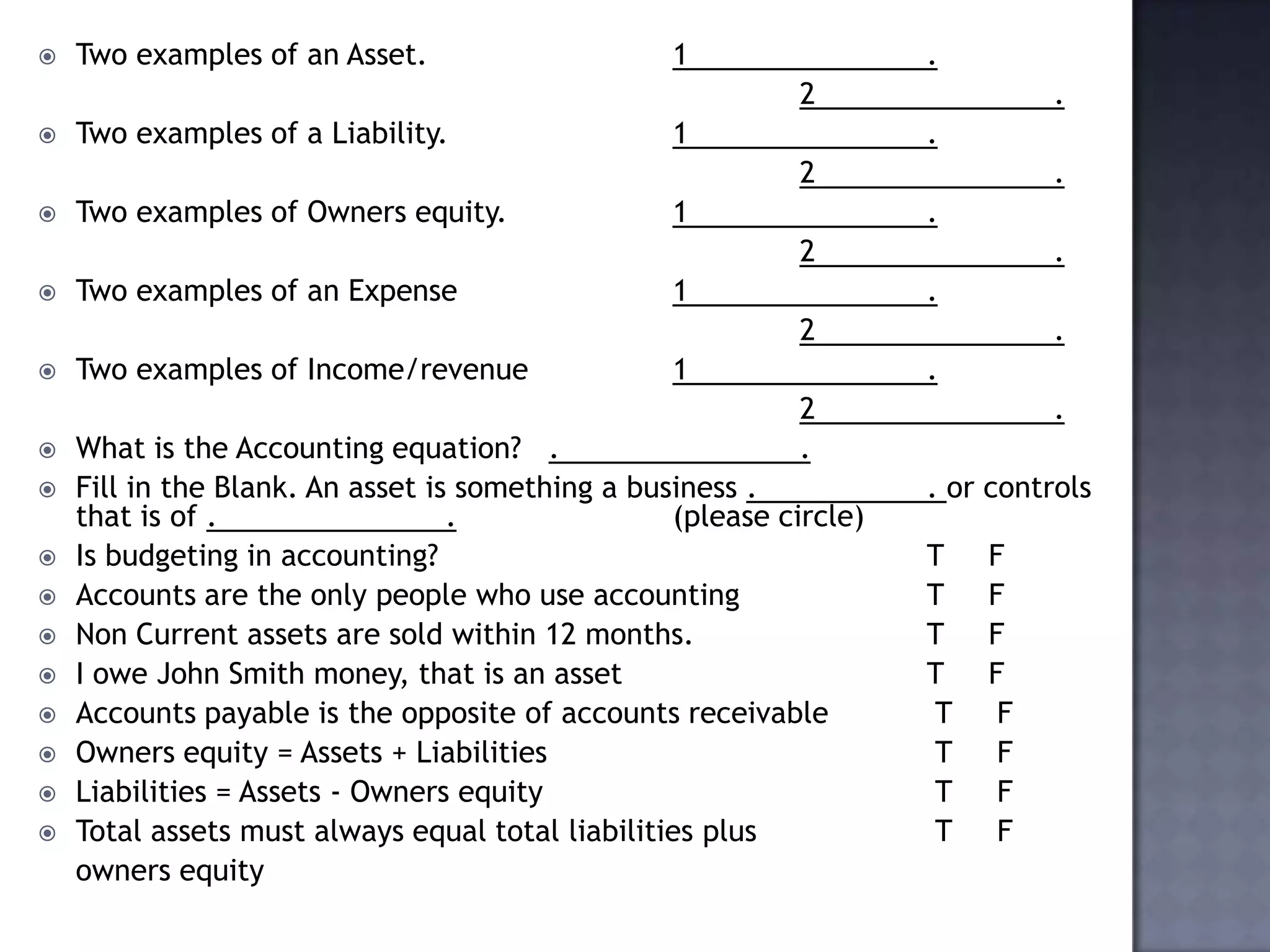

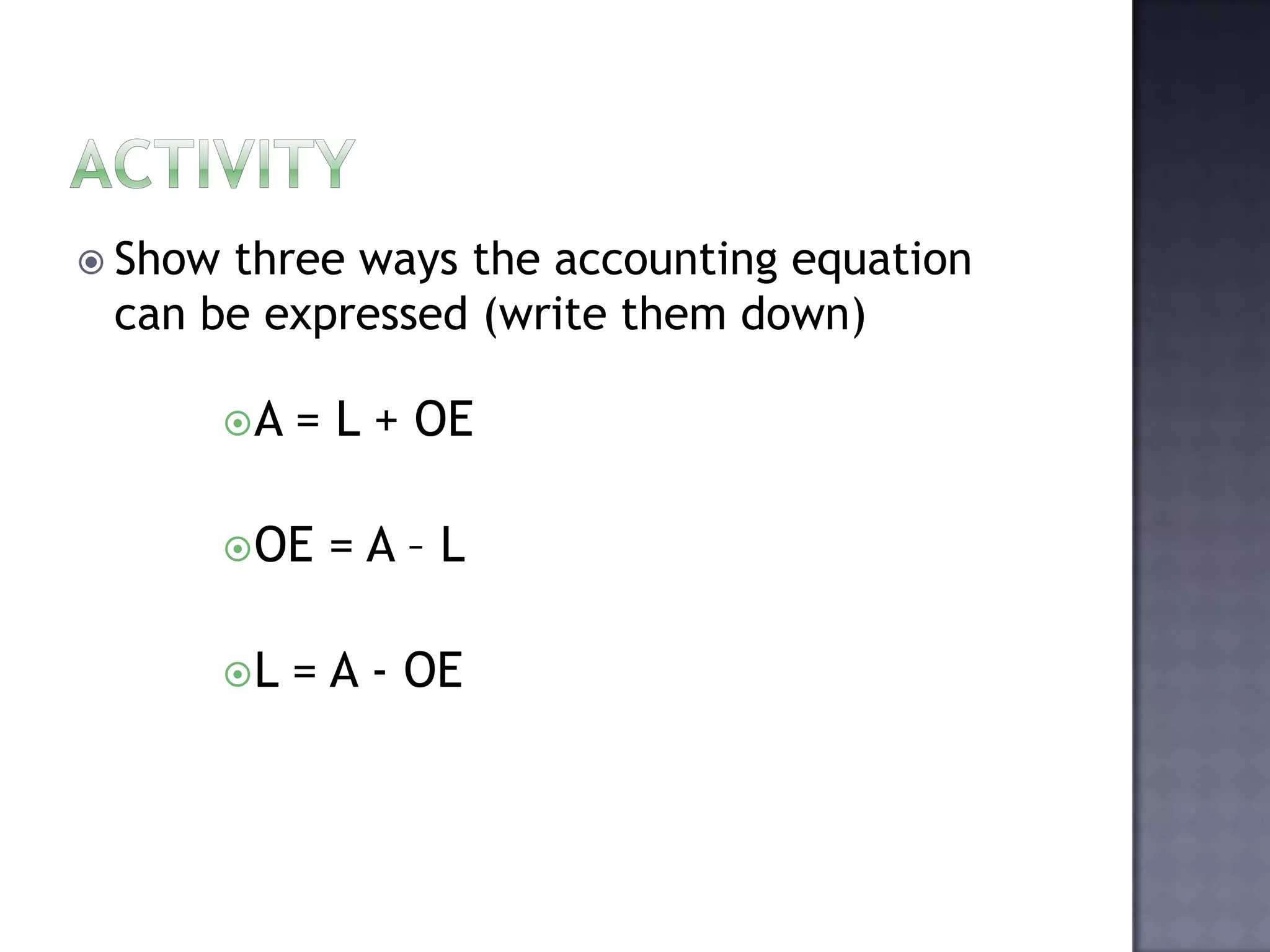

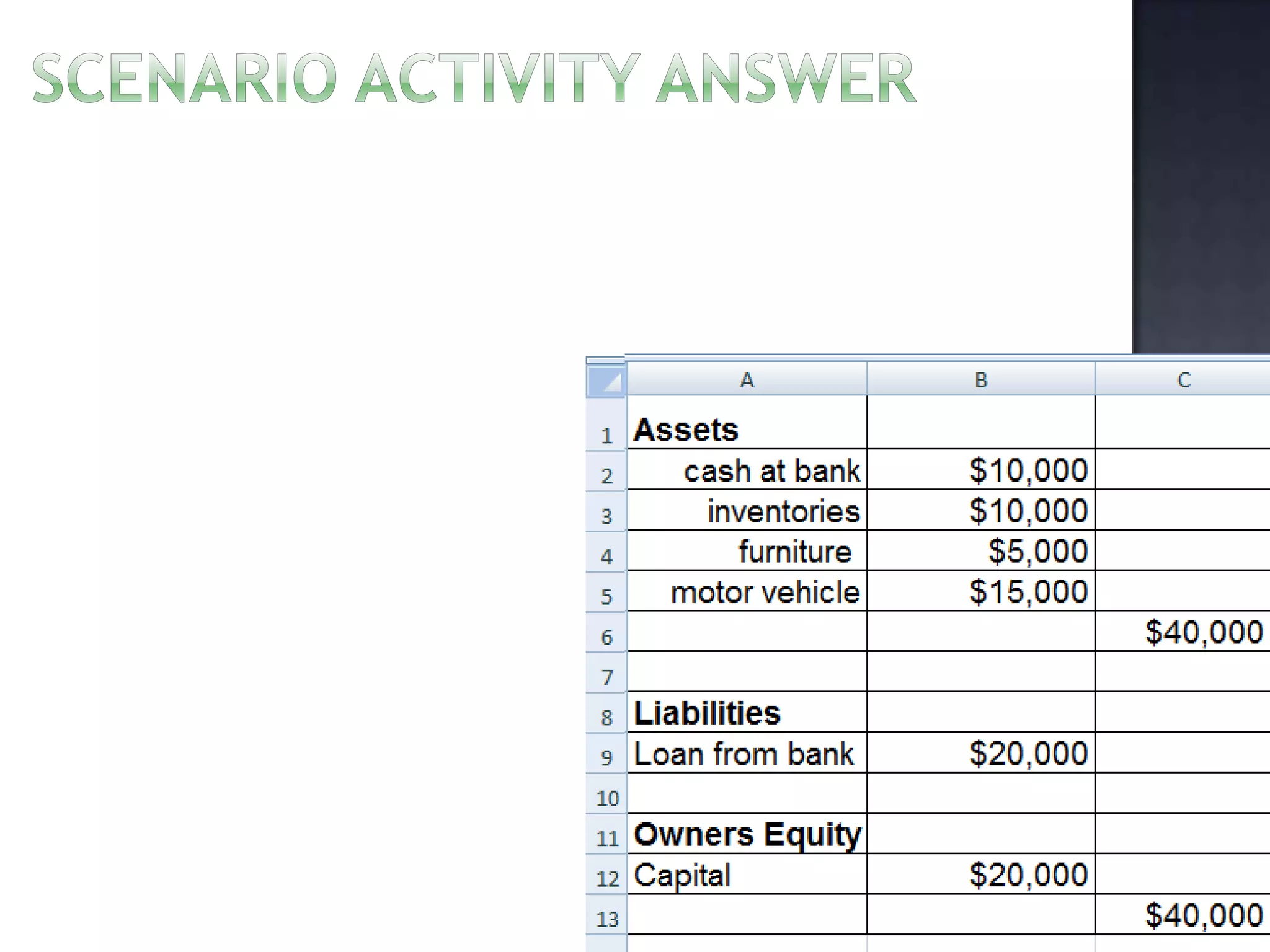

- Assets are resources owned that provide future benefits, liabilities are debts owed, and equity is the owners' claim on assets. The accounting equation is Assets = Liabilities + Equity.

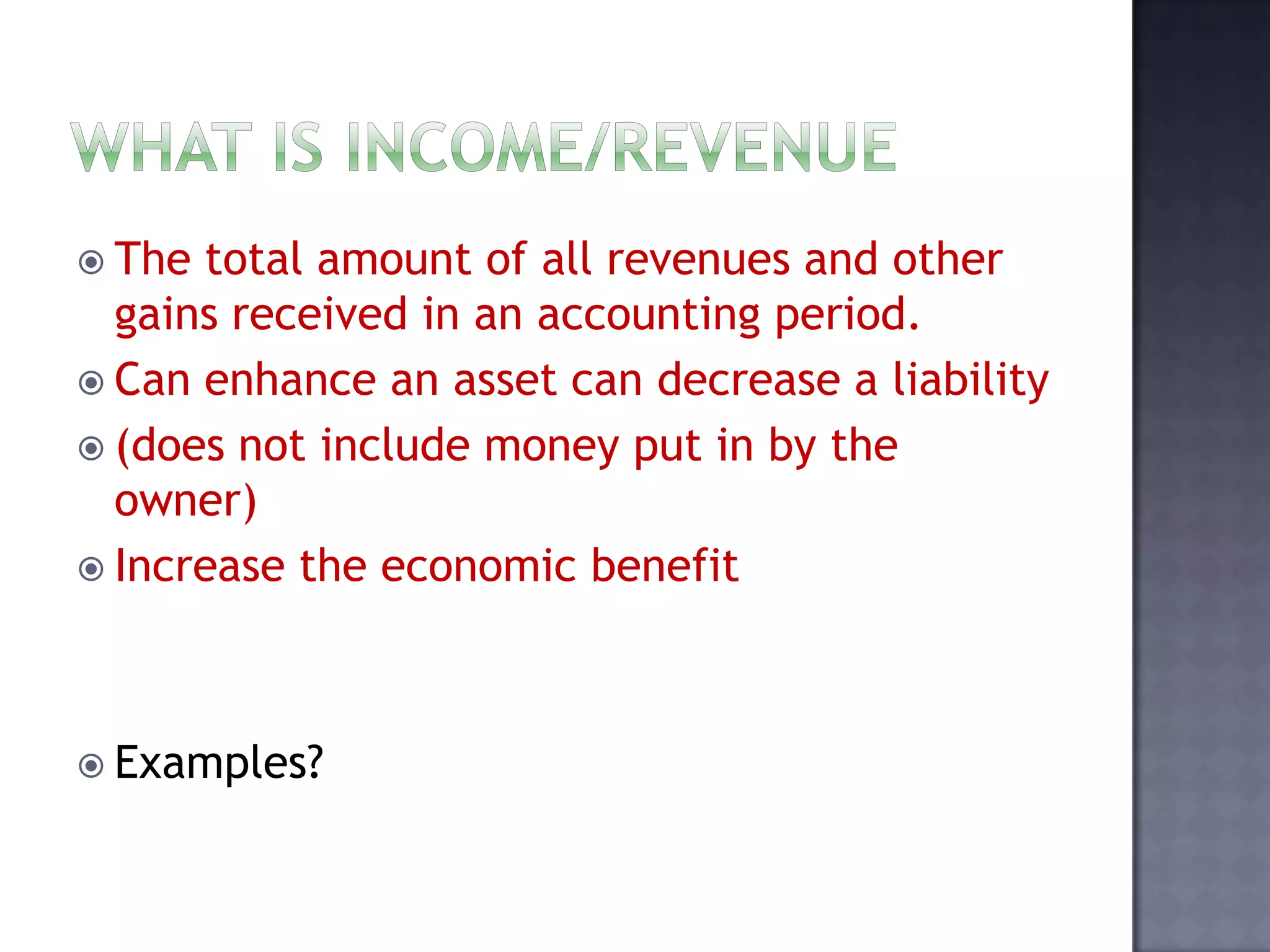

- Income increases assets and equity, expenses decrease assets. Common income examples are sales revenue and expenses include supplies and wages.

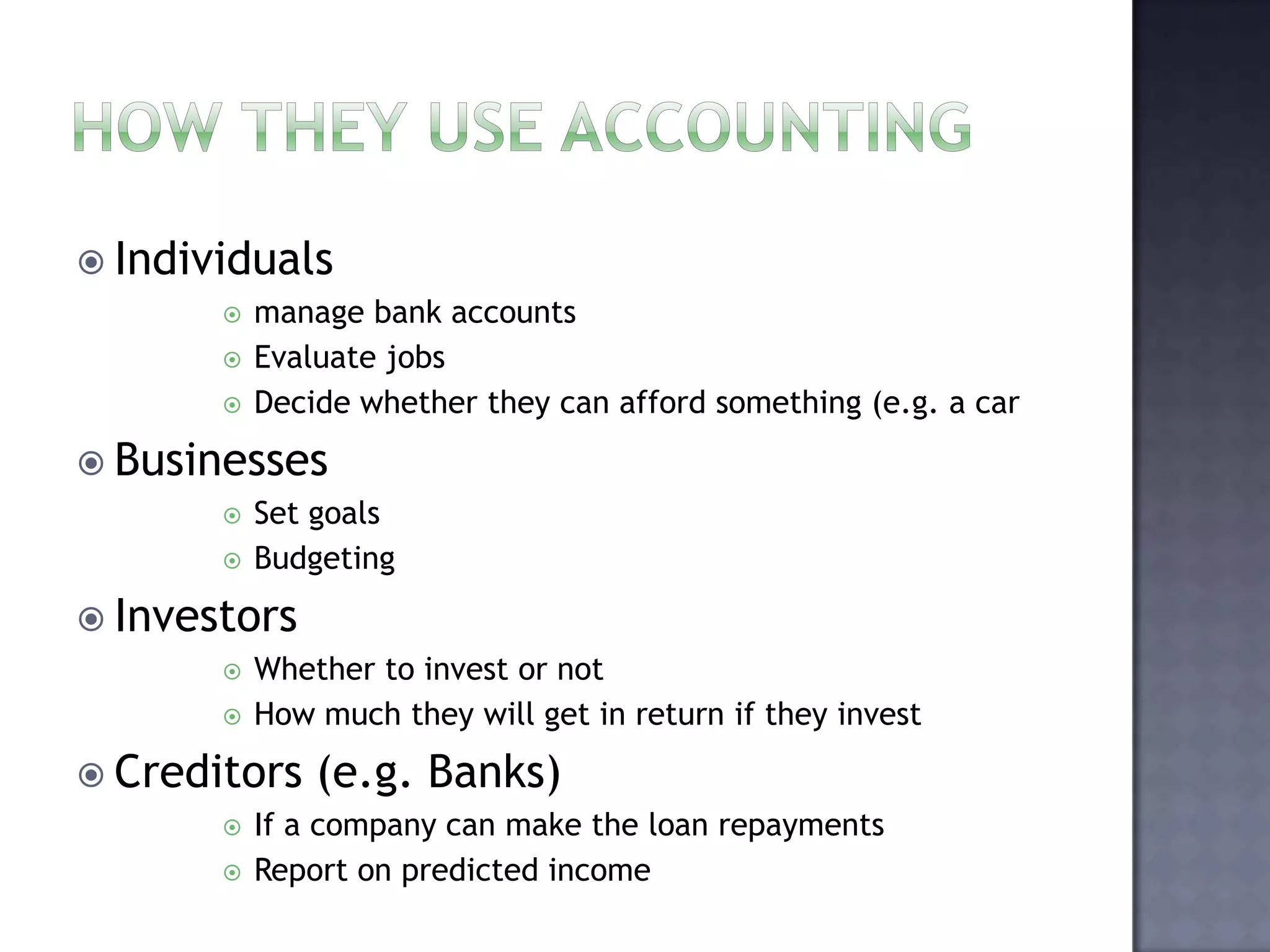

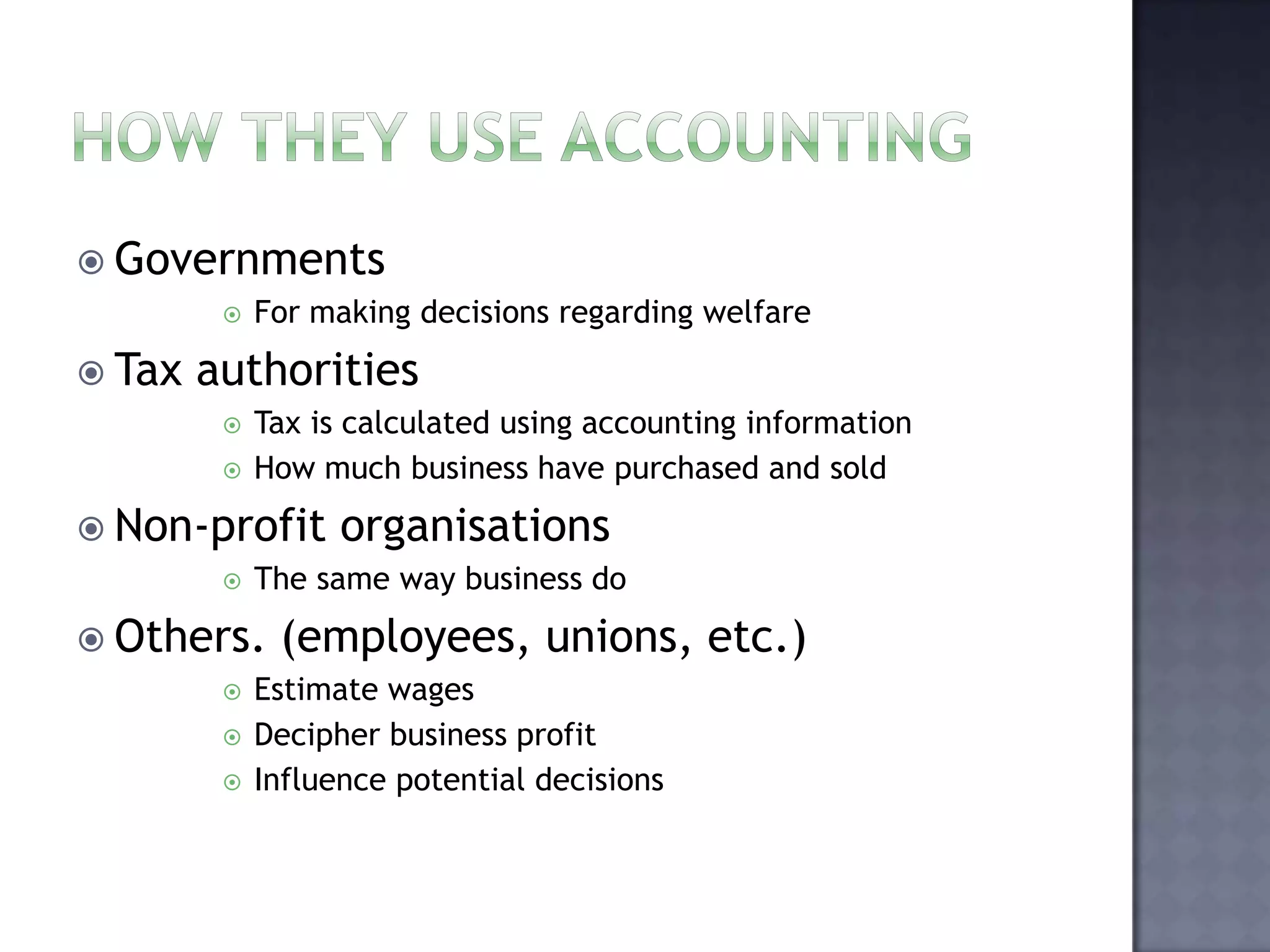

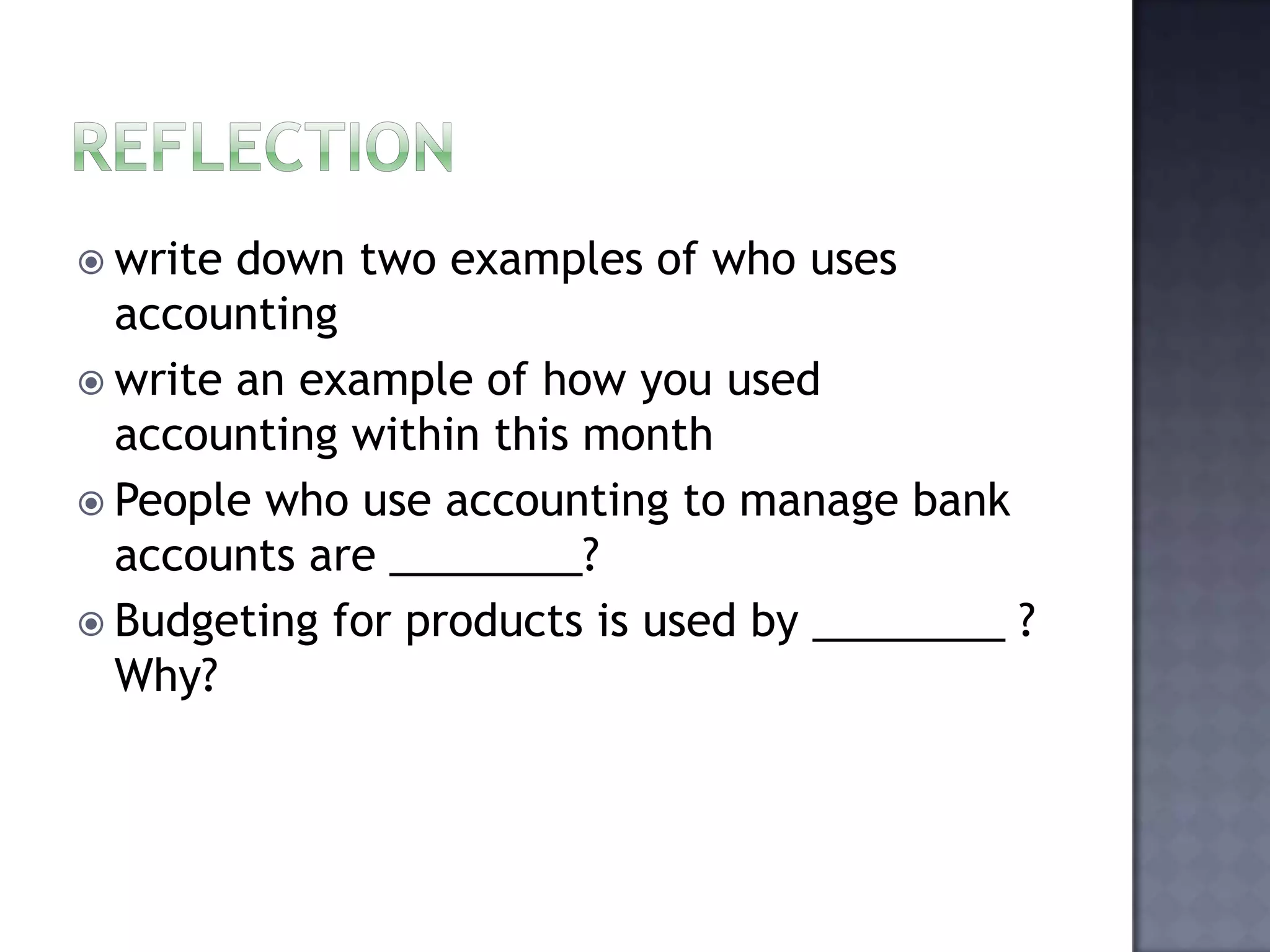

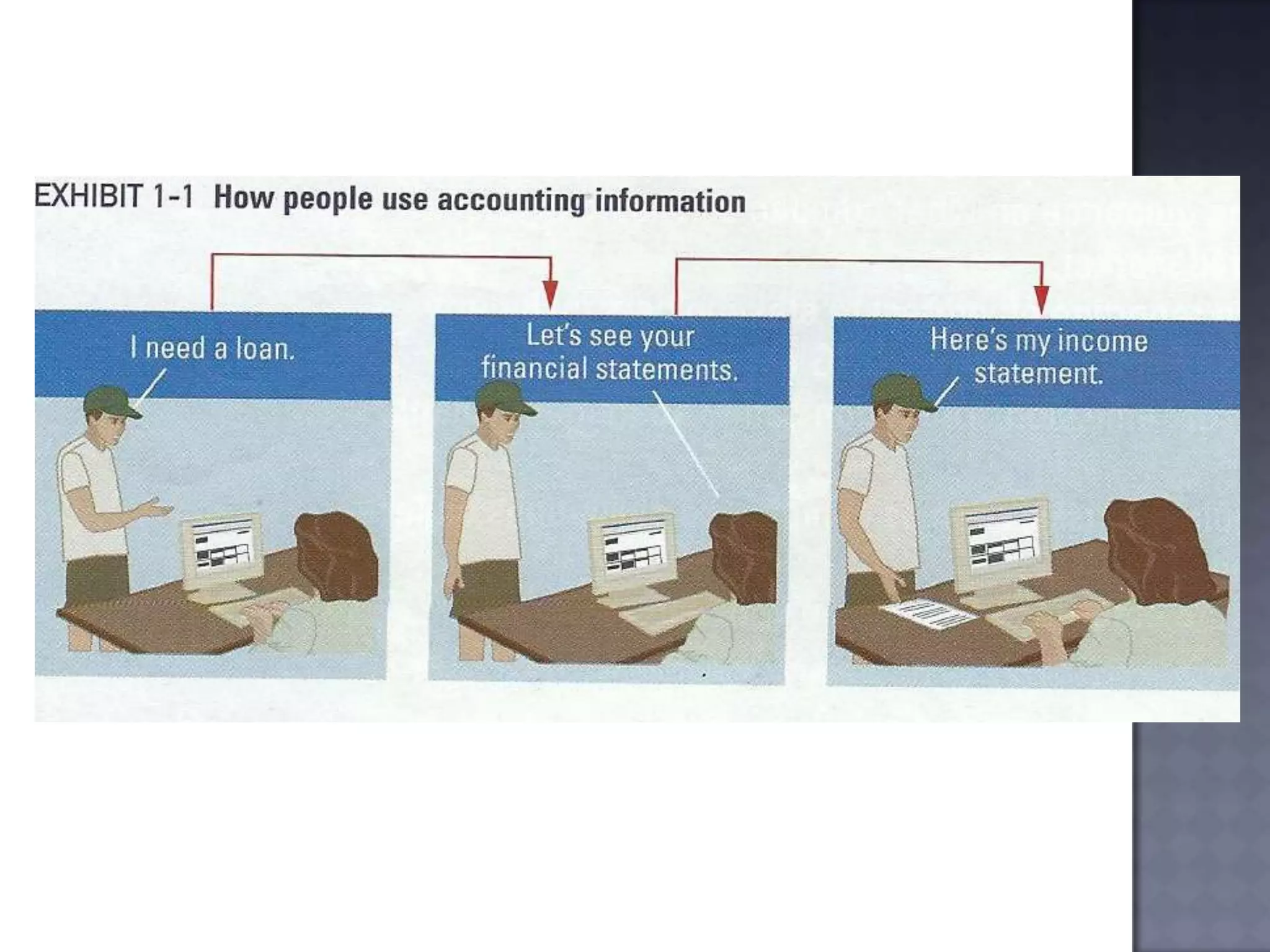

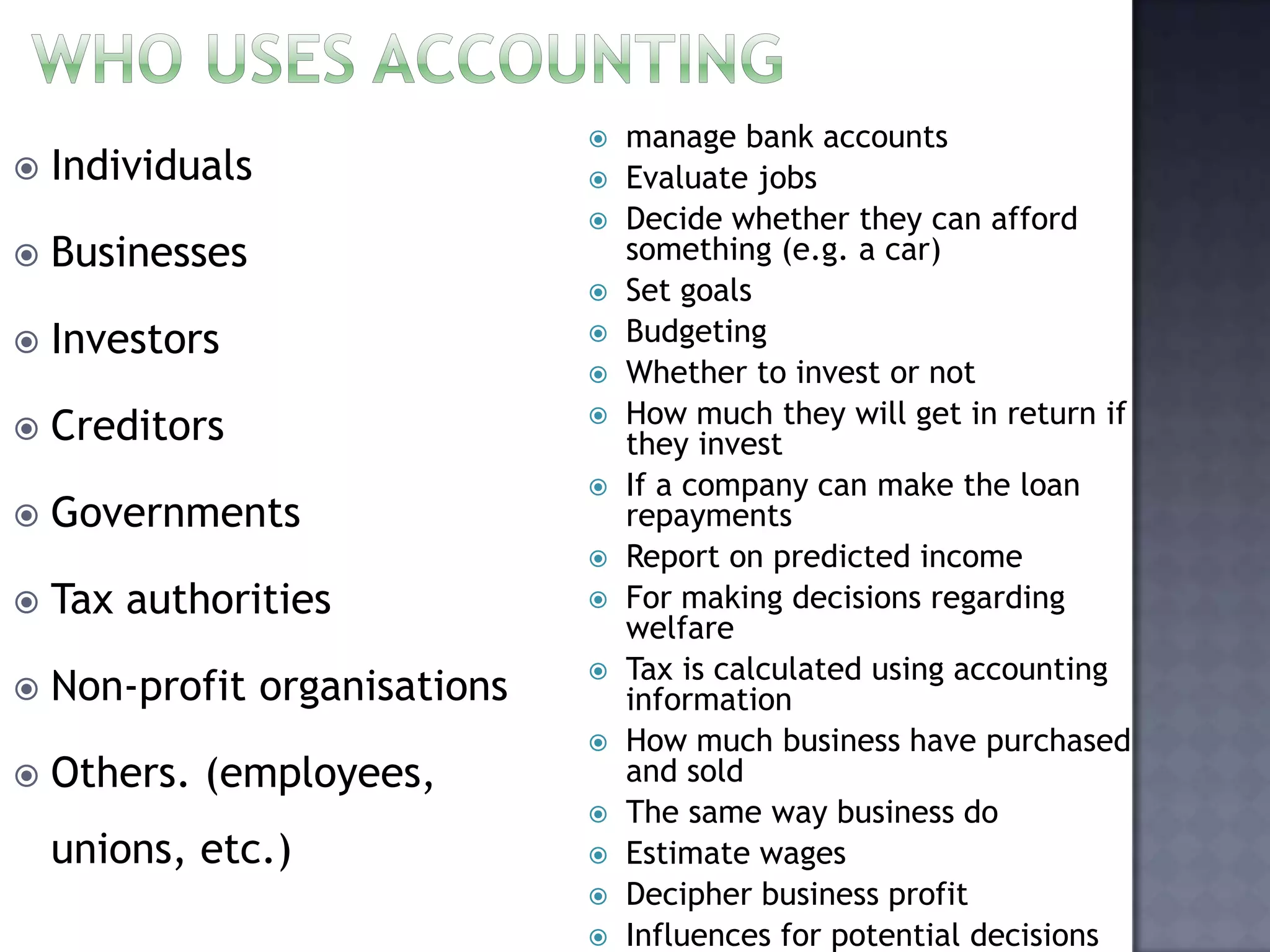

- Individuals, businesses, investors, creditors, governments and non-profits all use accounting information for purposes like managing finances, evaluating investments, and making decisions.