Download to read offline

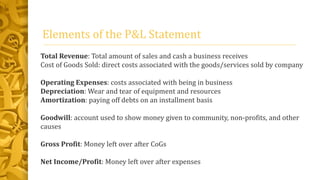

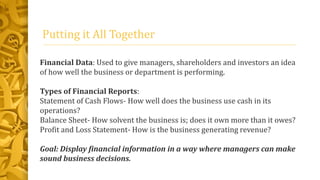

The document discusses cash flow statements, balance sheets, and income statements. It provides definitions and examples of key terms used in each type of financial statement. Cash flow statements track money in and out of the business. Balance sheets show a company's assets, liabilities, and equity at a point in time. Income statements summarize a company's revenues and expenses over a period of time. Financial statements together provide important information to managers and investors about a company's financial performance and health.