Download to read offline

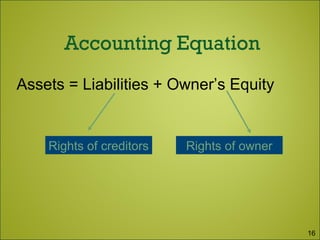

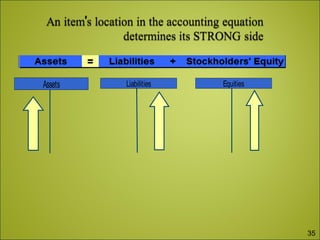

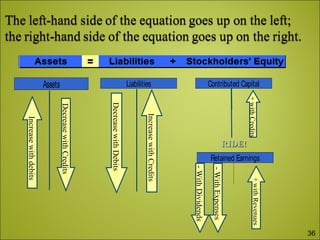

Financial accounting provides financial information to external parties such as creditors, investors and governmental agencies. It reports on the financial position and performance of a firm through financial statements. The key elements of financial accounting are assets, liabilities and shareholders' equity. Assets are items owned by a company, liabilities are amounts owed, and shareholders' equity represents the owners' claim on assets. The accounting equation states that assets must always equal liabilities plus shareholders' equity. Financial accounting uses double-entry bookkeeping to record transactions, ensuring the accounting equation stays in balance.