This document discusses various exemptions from income tax for salary income in India. It summarizes provisions related to leave salary, gratuity, pension, allowances, perquisites, provident fund and other deductions from salary that are exempt from tax. Key points include leave salary being fully tax exempt for government employees but with a maximum exemption of average salary for 10 months or Rs. 300,000 for non-govt employees. Gratuity is also exempt up to Rs. 10 lakhs. Certain allowances and perquisites like housing, medical benefits and interest-free loans are partially or fully tax exempt.

![Page 3

Income Exempted from Tax

In computing the total income of a previous year of any person, any income,

falling within any of the following clause, shall not be included in computing the

total income of such person. However, in order to claim exemption under this

section, it is the duty of the assessee to prove that an item of receipt falls within the

exempted category.

Different Provision:

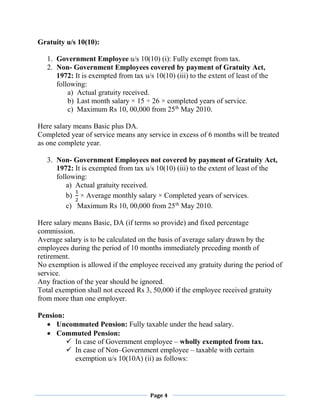

Leave Salary: Sec 10(AA)

1. In case of Government employees – Fully tax-free. But leave salary

received during tenure of service, full taxable.

2. In case of Non- Government employees – Taxable but assessee will get

exemption u/s 10(10AA) (ii) to the extent of least of the following:

a) Actual leave salary received.

b) Cash equivalent of leave to the credit of the employee at the time of

retirement.

c) 10 months average salary.

d) Maximum Rs 3,00,000

Here salary means Basic, DA (if terms of employment so provide) and fixed

percentage commission.

Average salary is to be calculated on the basis of average salary drawn by the

employee during the period of 10 months immediately preceding his retirement.

Cash Equivalent of Leave Salary = [Earned leave – Leave availed] × Average

Salary.

As per IT Rules employees shall get maximum 30 days earned leave for each

completed year of service (ignore any fraction of year).](https://image.slidesharecdn.com/incomeexemptedfromtax-140521105426-phpapp02/85/Income-Exempted-from-Tax-3-320.jpg)

![Page

11

Deduction from salaries u/s 16:

Standard deduction u/s 16(i)----Nil

Deduction for Entertainment Allowance [Government employee] 16(ii) -

least of the following:

a) Actual amount received.

b)

1

5

Of basic salary.

c) Rs 5,000

Deduction for Professional tax u/s 16(iii) – Actual amount paid.](https://image.slidesharecdn.com/incomeexemptedfromtax-140521105426-phpapp02/85/Income-Exempted-from-Tax-11-320.jpg)