More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (11)

Similar to Rule of salary

Similar to Rule of salary (20)

Recently uploaded

Recently uploaded (14)

Rule of salary

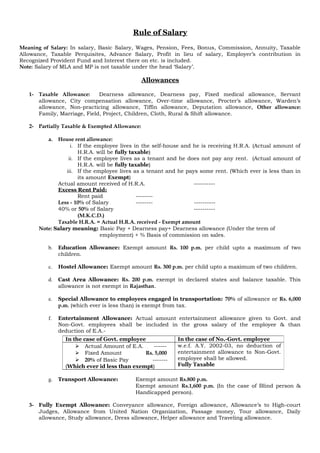

- 1. Rule of Salary Meaning of Salary: In salary, Basic Salary, Wages, Pension, Fees, Bonus, Commission, Annuity, Taxable Allowance, Taxable Perquisites, Advance Salary, Profit in lieu of salary, Employer’s contribution in Recognized Provident Fund and Interest there on etc. is included. Note: Salary of MLA and MP is not taxable under the head ‘Salary’. Allowances 1- Taxable Allowance: Dearness allowance, Dearness pay, Fixed medical allowance, Servant allowance, City compensation allowance, Over-time allowance, Procter’s allowance, Warden’s allowance, Non-practicing allowance, Tiffin allowance, Deputation allowance, Other allowance: Family, Marriage, Field, Project, Children, Cloth, Rural & Shift allowance. 2- Partially Taxable & Exempted Allowance: a. House rent allowance: i. If the employee lives in the self-house and he is receiving H.R.A. (Actual amount of H.R.A. will be fully taxable) ii. If the employee lives as a tenant and he does not pay any rent. (Actual amount of H.R.A. will be fully taxable) iii. If the employee lives as a tenant and he pays some rent. (Which ever is less than in its amount Exempt) Actual amount received of H.R.A. ---------- Excess Rent Paid: Rent paid -------- Less - 10% of Salary -------- ---------- 40% or 50% of Salary ---------- (M.K.C.D.) Taxable H.R.A. = Actual H.R.A. received - Exempt amount Note: Salary meaning: Basic Pay + Dearness pay+ Dearness allowance (Under the term of employment) + % Basis of commission on sales. b. Education Allowance: Exempt amount Rs. 100 p.m. per child upto a maximum of two children. c. Hostel Allowance: Exempt amount Rs. 300 p.m. per child upto a maximum of two children. d. Cast Area Allowance: Rs. 200 p.m. exempt in declared states and balance taxable. This allowance is not exempt in Rajasthan. e. Special Allowance to employees engaged in transportation: 70% of allowance or Rs. 6,000 p.m. (which ever is less than) is exempt from tax. f. Entertainment Allowance: Actual amount entertainment allowance given to Govt. and Non-Govt. employees shall be included in the gross salary of the employee & than deduction of E.A.- g. Transport Allowance: Exempt amount Rs.800 p.m. Exempt amount Rs.1,600 p.m. (In the case of Blind person & Handicapped person). 3- Fully Exempt Allowance: Conveyance allowance, Foreign allowance, Allowance’s to High-court Judges, Allowance from United Nation Organization, Passage money, Tour allowance, Daily allowance, Study allowance, Dress allowance, Helper allowance and Traveling allowance. In the case of Govt. employee In the case of No.-Govt. employee Actual Amount of E.A. ------ Fixed Amount Rs. 5,000 20% of Basic Pay ------- (Which ever id less than exempt) w.e.f. A.Y. 2002-03, no deduction of entertainment allowance to Non-Govt. employee shall be allowed. Fully Taxable

- 2. Valuation of Perquisites 1- Valuation of unfurnished residential house (Rent Free House) Govt. Employee Non-Govt. Employee If house is owned by employer If the house is hired or taken on rent by the employer In the case of Hotel Actual value as per Govt. Rule in any cities. All amounts will be Taxable. License Fees 7.5% of Salary if the population of the city upto 10 Lac or 10 Lac. or 10% of Salary if the population of the city is more than 10 Lac & less than 25 Lac. or 15% of Salary if the population of the city is more than 25 Lac. (i) Actual Rent paid by the employer. or (ii) 15% of Salary (Which ever is less than in its amount Taxable) Any city (i) Actual Charges paid by employer/ employee or (ii) 24% of Salary (Which ever is less than in its amount Taxable) Any city 2- Valuation of furnished house: Value of unfurnished house as above + 10% Cost of furniture or Actual rent of furniture (Ist preference for rent.) 3- Valuation of concessional unfurnished and furnished house: Calculated value in the case (1 & 2) as above -------- Less- Rent paid by the employee -------- or Rent deducted out of salary of employee -------- -------- Balance Amount Taxable -------- Note: Salary meaning: Basic pay (except advance & arrears of salary)+ Dearness pay + Dearness allowance (If it is under the term of employment) + Fees + Bonus + Commission on sales + All taxable allowance paid by the employer. 4- Payment of liabilities of employee by the employer: Specified actual amount paid by employer for all type of employees is Taxable. 5- Valuation of facilities of Gass, Electricity & Water: From own sources From outside sources All facilities supplies by the employer from its own sources. All actual amount fully Taxable. For only office use For only personal use For personal & office use Nill Actual amount paid by the employee (Taxable) Toal expenses-Paid expenses by the employee= Taxable 6- Valuation of Sweeper, Watchman, Gardner & Any other domestic servant: If servants are appointed by the employer facility of Sweeper, Gardner, Watchman & other domestic servant Fully amount of salary is Taxable (For specified employee) If servants are appointed by the Employees and payments are paid by the employer Actual amount paid to each servant is Taxable. (For specified or Non-specified employee)

- 3. 7- Valuation of Motor Car: If motor car is owned or hired by employer If motor car is used for official purpose Nil If motor car is used for official purpose exclusively for the private purpose Actual Amount of Exp. + Salary of driver + Normal wear and tear (Dep. @ 10%) or Hire Charges – Amount charged from employee for such use. If motor car is used for official purpose and Private & Personal Purpose For upto 16,00cc or 1,600cc Rs. 1,800 p.m. Or For more than 16,00cc Rs. 2,400 p.m. + Driver Salary Rs. 900 p.m If motor car is owned by employee and reimbursed by the employer If motor car is used for official purpose Nil If motor car is used for official purpose exclusively for the private purpose Actual amount paid by employer. All Amount Taxable (all category of employees) If motor car is used for official purpose and Private & Personal Purpose Actual amount Paid by employer – Amount Exempted by the previous rule. Provident Fund Particulars Statutory Provident Fund Recognized Provident Fund Unrecognized Provident Fund Employee contribution included in taxable salaries Exempt U/S – 89 Exempt Exempt Employer’s contribution Exempt Taxable amount excess 12% of salary Exempt Interest of P.F. Exempt Taxable amount excess 9.5% of interest amount. Exempt Lumpsum amount at the time of retirement U/S – 10 (11) Exempt Exempt because the employee has served 5 years & under 5 years. Only employer contribution portion is Taxable with interest Note: Salary Meaning – H.R.A. salary. Death-cum-retirement Gratuity Govt. Employee Non- Govt. Employee Payment under Gratuity Act, 1972 Payment under Not-covered Gratuity Act, 1972 Actual Amount of Gratuity Received Full Exempt 1. Actual amount received ------- 2. Fixed amount Rs. 10,00,000 3. Calculation of amount: Last month salary *15 days * Whole time of service / 26 days (Which ever is less than amount Exempt) Note: Basic pay + D.A. + D.P.. Full year consider more than 6 month or 6 month service. 1. Actual amount received ------- 2. Fixed amount Rs. 10,00,000 3. Calculation of amount: Average salary of Last 10 month *15 days * Whole time of service / 30 days (Which ever is less than amount Exempt) Note: H.R.A. salary Excluding part of last year service. Taxable Amount = Gratuity Received – Exempt Amount

- 4. Pension (i) Uncommuted Pension: Uncommuted Pension received monthly by a retired employee from his employer is included in salary. (ii) Commuted Pension: Govt. Employee Non- Govt. Employee If the employee will be Gratuity received If the employee will not be Gratuity received Actual amount of commuted pension will be Exempt. 1- Actual amount received ------ 2- Calculation of full amount of pension ------ 3- 1/3 Amount of full pension Exempt 1- Actual amount received ------ 2- Calculation of full amount of pension ------ 3- 1/2 Amount of full pension Exempt Taxable Amount = Actual Amount Received – Exempt Amount