The document contains details of an individual's monthly income from April 2005 to March 2006. It lists sources of income like basic salary, house rent allowance, and other allowances. It also contains details for tax deductions that can be claimed under sections 80C, 80D, 80DD, and 80DDB of the Income Tax Act. The document is intended to help calculate the individual's tax liability for the financial year 2005-2006.

Taxation 101 basic rules and principles in philippine taxation by jr lopez go...JR Lopez Gonzales

This was the informative speech on the basic taxation principles in the Philippines. It was a thirty-minute speech on the basics of the Philippine Tax system presented to the students of the Mindanao State University - Iligan Institute of Technology on 8 August 2011 for the Political Science 2 Lecture Series. The document was uploaded by JR Lopez Gonzales of www.politikalon.blogspot.com.

Taxation 101 basic rules and principles in philippine taxation by jr lopez go...JR Lopez Gonzales

This was the informative speech on the basic taxation principles in the Philippines. It was a thirty-minute speech on the basics of the Philippine Tax system presented to the students of the Mindanao State University - Iligan Institute of Technology on 8 August 2011 for the Political Science 2 Lecture Series. The document was uploaded by JR Lopez Gonzales of www.politikalon.blogspot.com.

Computation of Income from salaries for assessment year 2015-16 . Based on Goa university Final yea B Com Syllabus of Accounting Major II - Income tax, service tax and Goa Value added tax

Presentation on computation of income from house property for the benefit of students of Income tax. Useful material for undergraduate students of commerce faculty. It covers most of the important section of Income tax act applicable for computation of Income from house Property.

This is a short presentation for beginners wanting to learn a bit about the Indian Income-tax Act. It gives a snapshot of some of the basic terms in the Indian income-tax law. Hard core tax practitioners may kindly stay away! It's only the common man.

Computation of Income from salaries for assessment year 2015-16 . Based on Goa university Final yea B Com Syllabus of Accounting Major II - Income tax, service tax and Goa Value added tax

Presentation on computation of income from house property for the benefit of students of Income tax. Useful material for undergraduate students of commerce faculty. It covers most of the important section of Income tax act applicable for computation of Income from house Property.

This is a short presentation for beginners wanting to learn a bit about the Indian Income-tax Act. It gives a snapshot of some of the basic terms in the Indian income-tax law. Hard core tax practitioners may kindly stay away! It's only the common man.

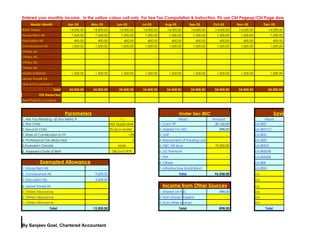

5. TAX COMPUATION for financial Year 2005-2006

Enter Your Name

Amount

Gross Salary Income 292,800.00

Less : Exempted Allowance U/s.10 13,200.00

Salary Income 279,600.00

Less : Professional Tax (U/s16(ii) -

Net Taxable Salary Income 279,600.00

Add : Income House Property -

Add : Income from other source 898.00

Gross Total Income 280,498.00

Less : Chapter VIA

U/s.80C 95,000.00

U/s.80D 15,000.00

U/s.80DD -

U/s.80DDB 60,000.00

U/s.80E -

U/s.80G - 170,000.00

Net Total Taxable Income 110,498.00

Net Total Taxable Income( Rounded to Rs.10) 110,500.00

Tax on Net Total Income 1,050.00

Add Surcharge ( 10% , if Total income exceeds Rs10 Lacs) -

Add Edu. Cess @ 2 % on IT + SC 21.00

Total Tax Payable 1,071.00

Less Tax Deducted at source -

Tax to be paid 1,071.00

Please read the instruction before acting upon this computation sheet

By Sanjeev Goel, Chartered Accountant

kgcdelhi@rediffmail.com

6. Tax Planner 2005-2006

By Sanjeev Goel, Chartered Accountant

kgcdelhi@rediffmail.com

This computation sheet is designed keeping in mind the general applicable incomes and allowances

applicable for salary class employees.

Heads of income and exemption not specified , may be entered in other allowances and exemption

there on in other exemption.

Taxable perquisites will be entered in other All. Head

Before turning to Tax Computation sheet, be sure that all relevant field in YELLOW coloured fields filled

properly

Medical Reimbursement to the extent Rs.15000/- or actual reimbursement which ever is less is

exempted

House Rent Allowance is exempted among least of the following 1. Actual HRA received. , 2. Rent Paid

- 10% of Basic., 3. 40 % or 50 % salary as the case may be.

Conveyance Allowance is exempted to the extent least of the followanceRs.800 or actual conveyance

allowance

Education Allowance is exempted to the extent Rs.100/Month in case school going child +

Rs.300/Month in case child in hostel up to 2 child

Leave Travel Allowance is exempted up to cost of 2 journy(only fare ) in a block of four calendar

period. Current blocks are 2002-2005 & 2006-2009 subject to 1st class rails or economy class air fare for

shortest route within any place in India

Conveyance Allowance is exempted up to Rs.800/- per month

Sec.80C ( Deduction inrespect of investment) Only individual or HUF can claim deduction under this

section for investment made upto Rs.100000/-

Sec.80D ( Midiclim Insurance) - The insurance premium paid or Rs.10000, whichever is lower is

deductable. However in case where any dependent or assessee attains 65 year or more during the

financial year the limit will be insurance premium paid or Rs.15000/- whichever is less.

Sec.80DD ( Maintenance & Medical teatment of handicaped dependent) - The maximum limit is

Rs.50000 or Rs.75000/- depending upon disability (Pl.Ref.Act)

Sec.80DDB ( Midical Treatment) - Actual expenses or Rs.60000/- which ever is less for medical treatment

of specified disease

Declaration : I, SANJEEV GOEL, no where responsible if any liability arises , by

acting upon this calculation sheet. This is merely designed to facilitate , to

compute tax liability arises from income , in particular for salary income group.

Tax Computation Sheet

Tax Computation Details Sheet