Downloaded 3,703 times

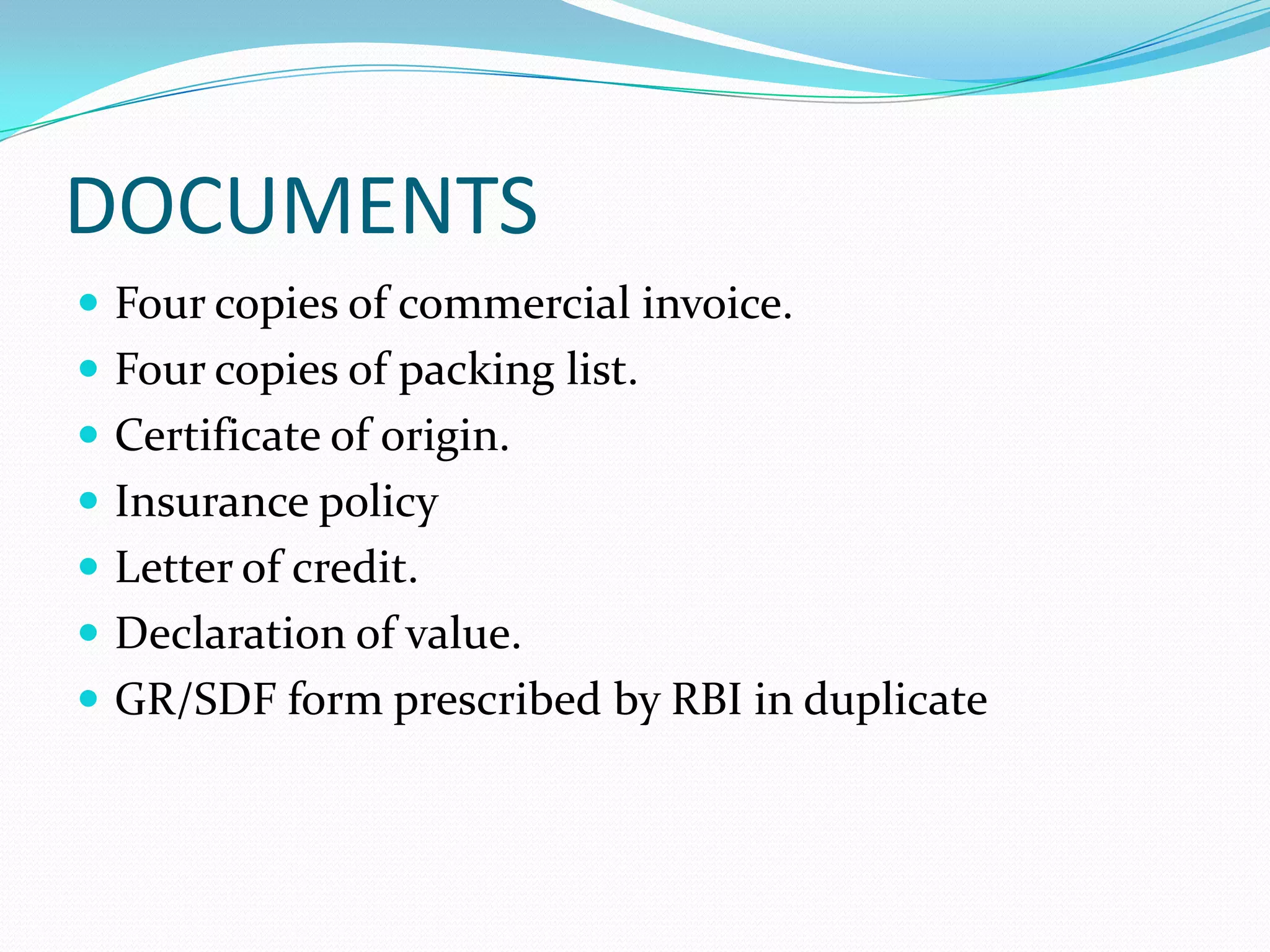

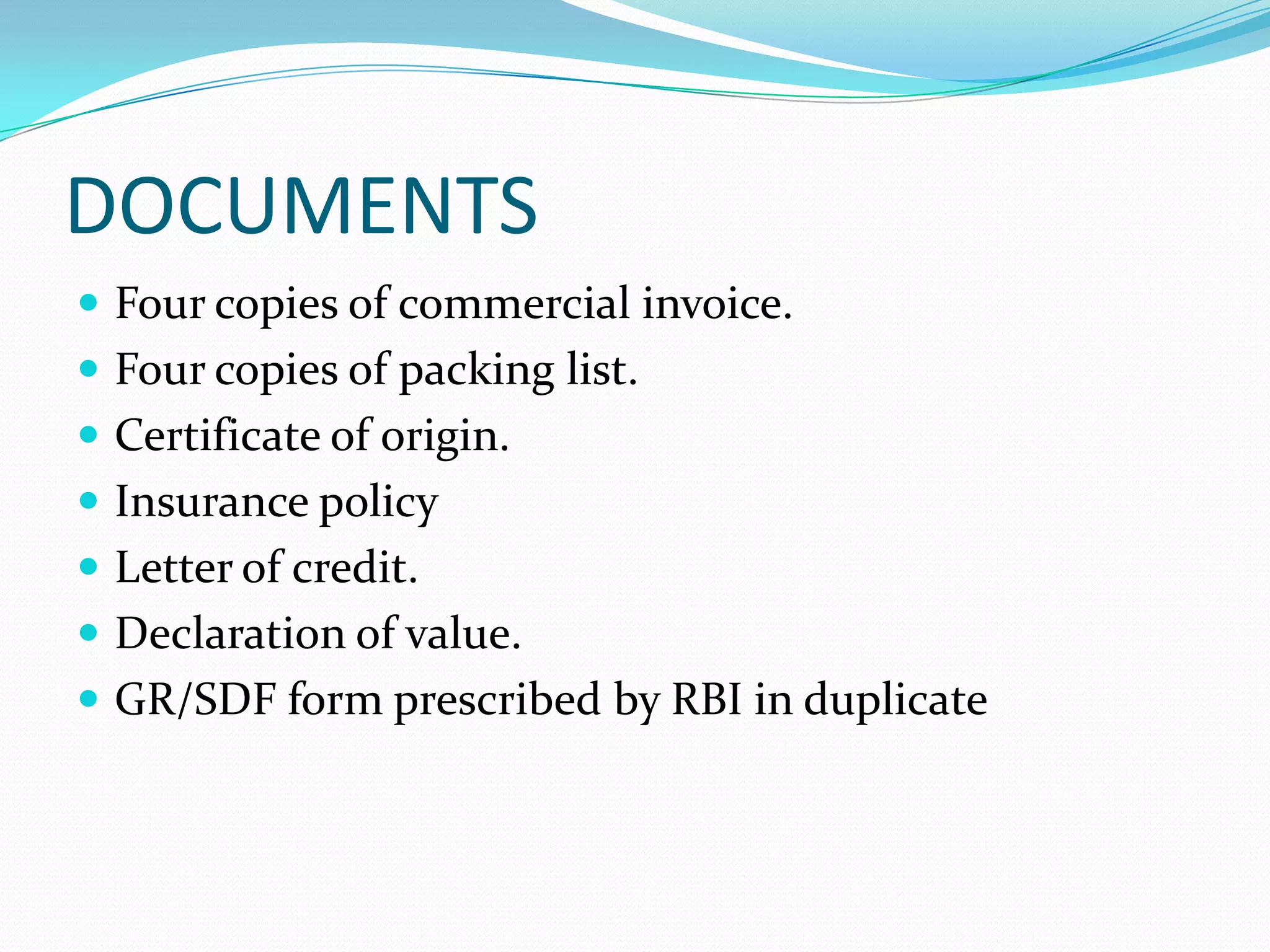

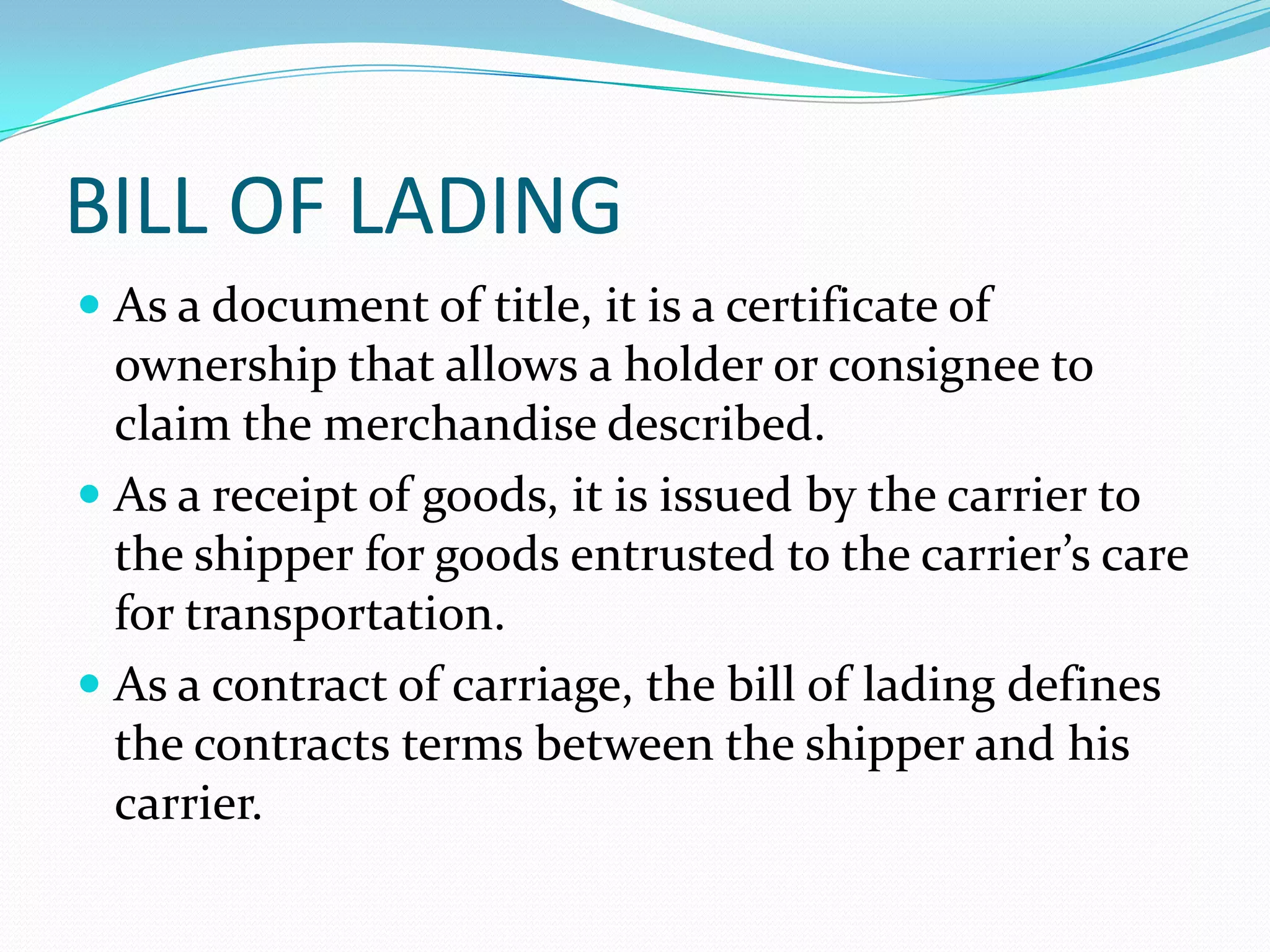

The document discusses procedures and documentation related to international trade. It defines key terms like exports, imports, and documents involved. For exports, it explains that an exporter must submit documents like a shipping bill, packing list, invoices, and export contract. It lists required export documents like commercial invoices, packing lists, certificates of origin, and more. For imports, it defines imports and restricted imports. It outlines the import process and important documents like import licenses, indents, letters of credit, bills of entry and lading. It also discusses terms for international trade like FOB, CIF, and documents involved in documentary collection.

Presentation by Ritesh Parmar. Definition of export includes ownership change, even without physical movement.

Presentation by Ritesh Parmar. Definition of export includes ownership change, even without physical movement.

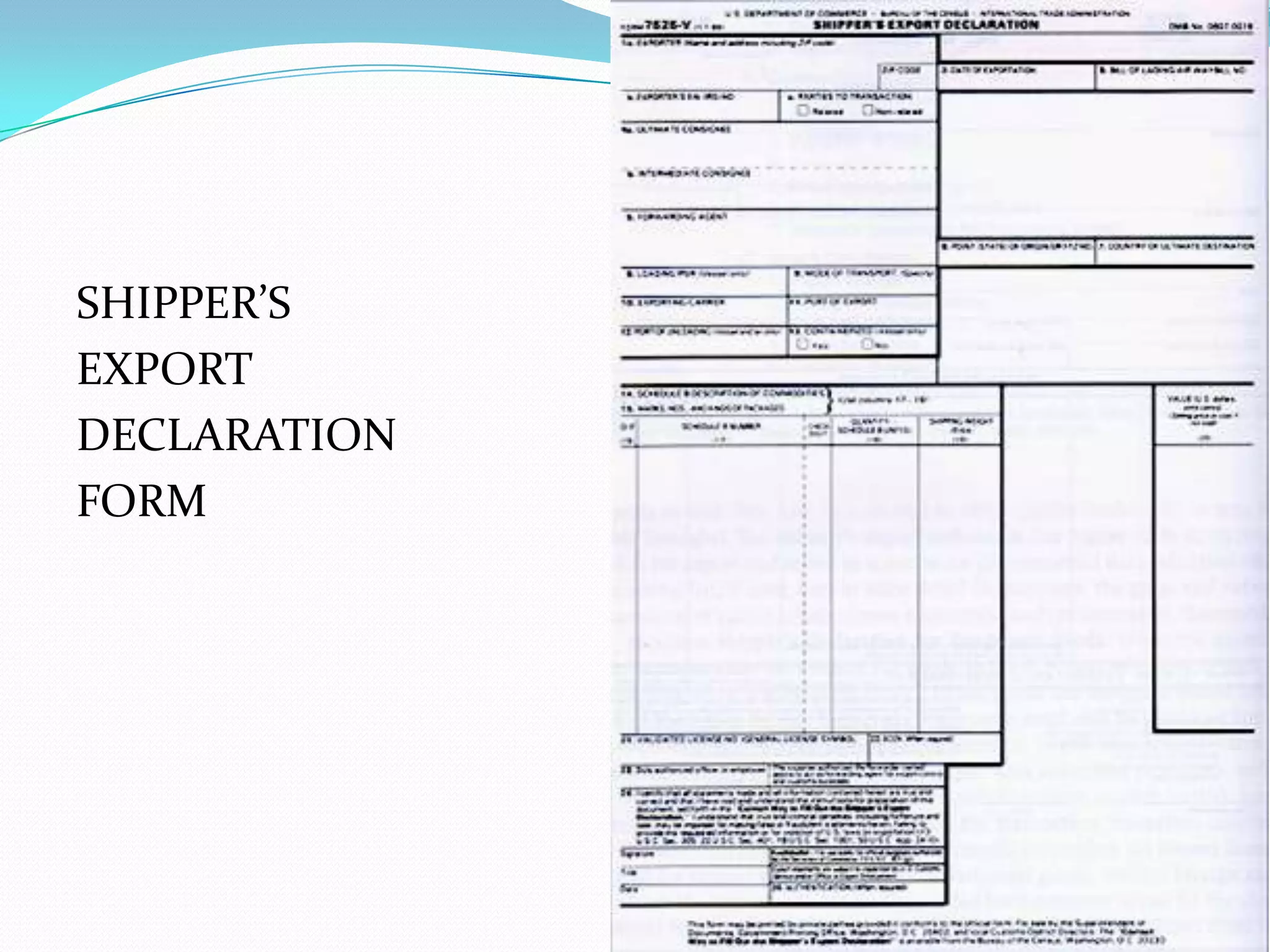

Step-by-step export process outlined, including shipping bills, declarations, and necessary documents like invoices and bills of lading.

Definitions of imports; restricted items mentioned; detailed procedures on obtaining necessary licenses and paying customs duties.

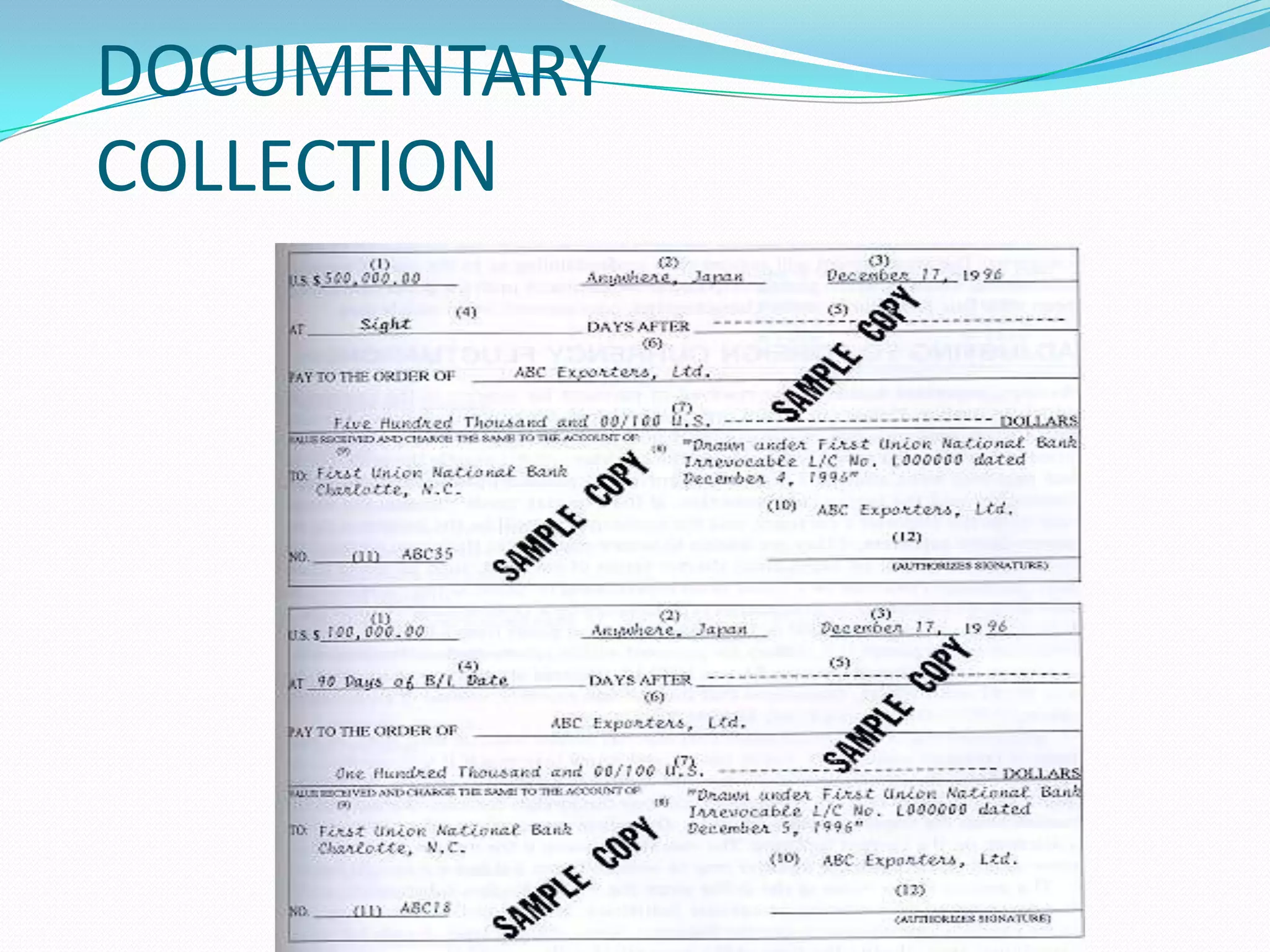

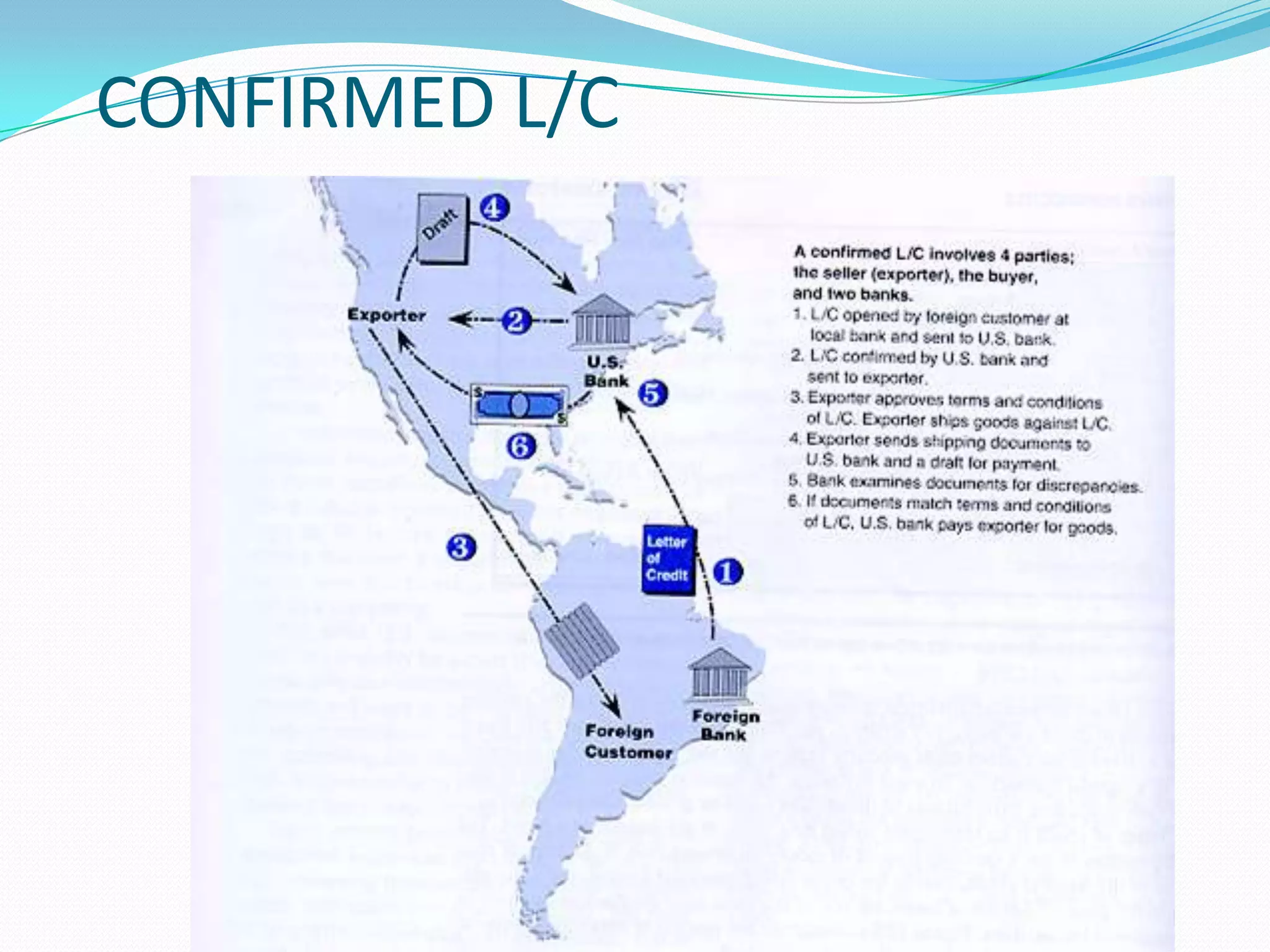

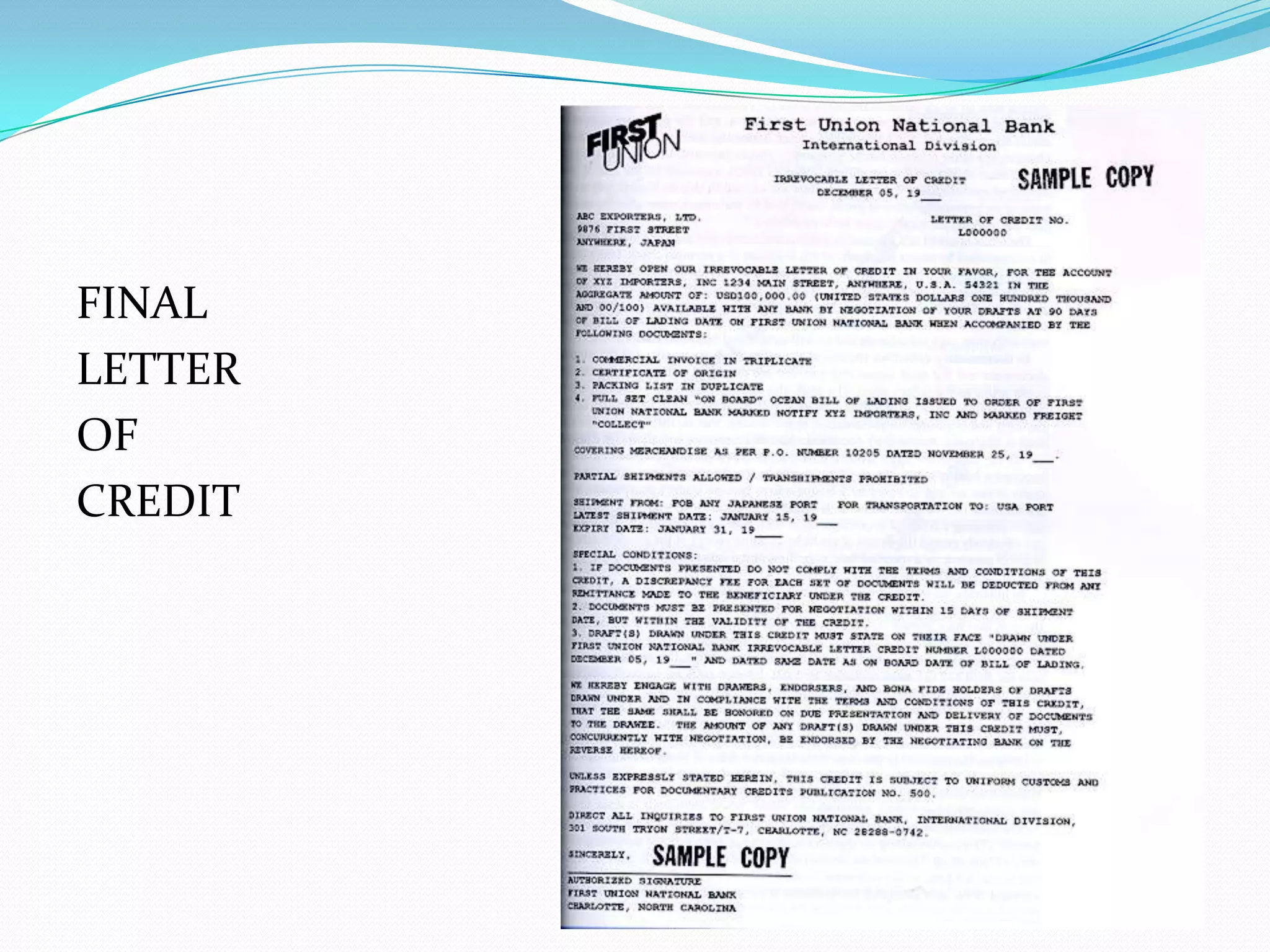

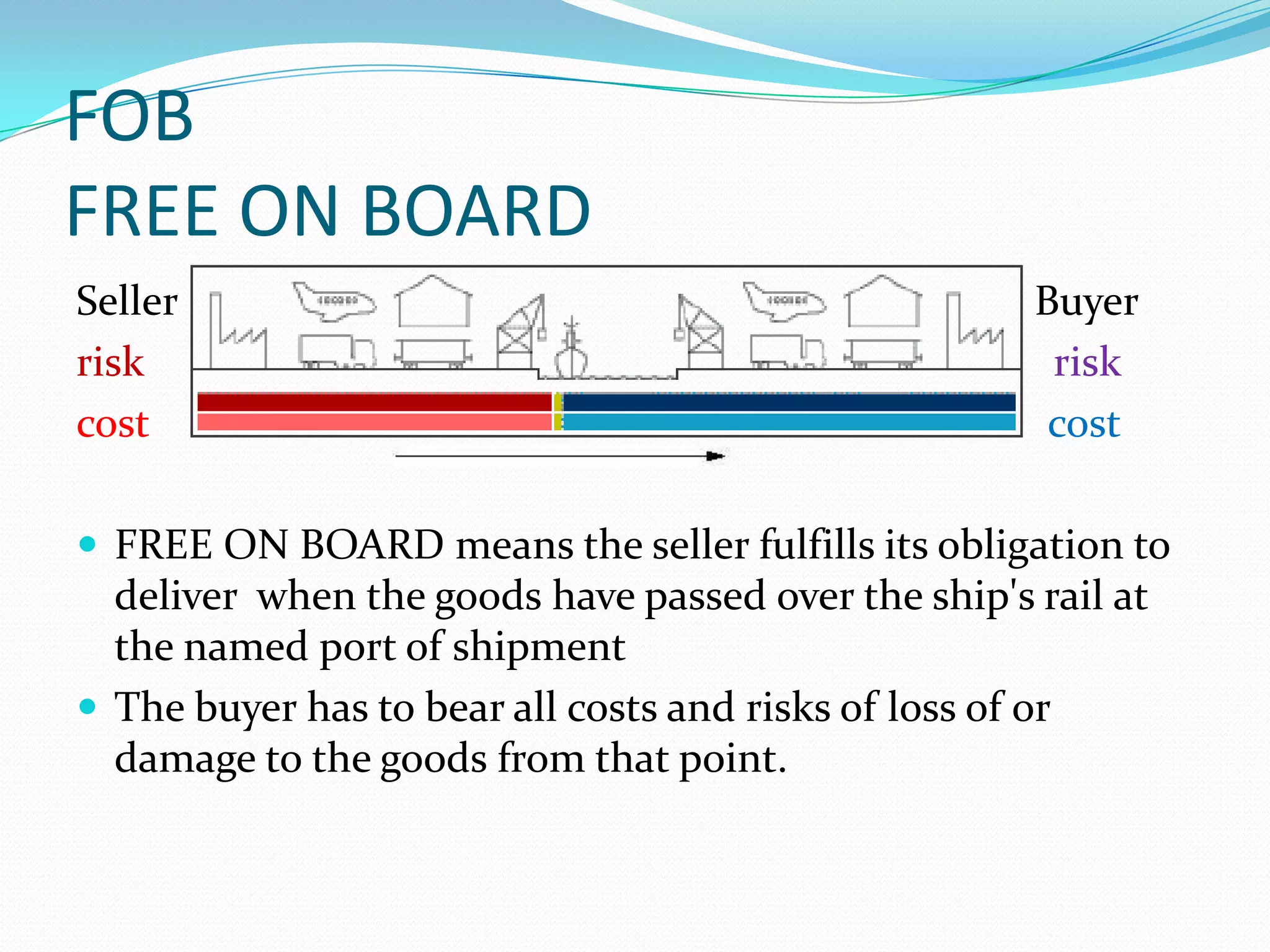

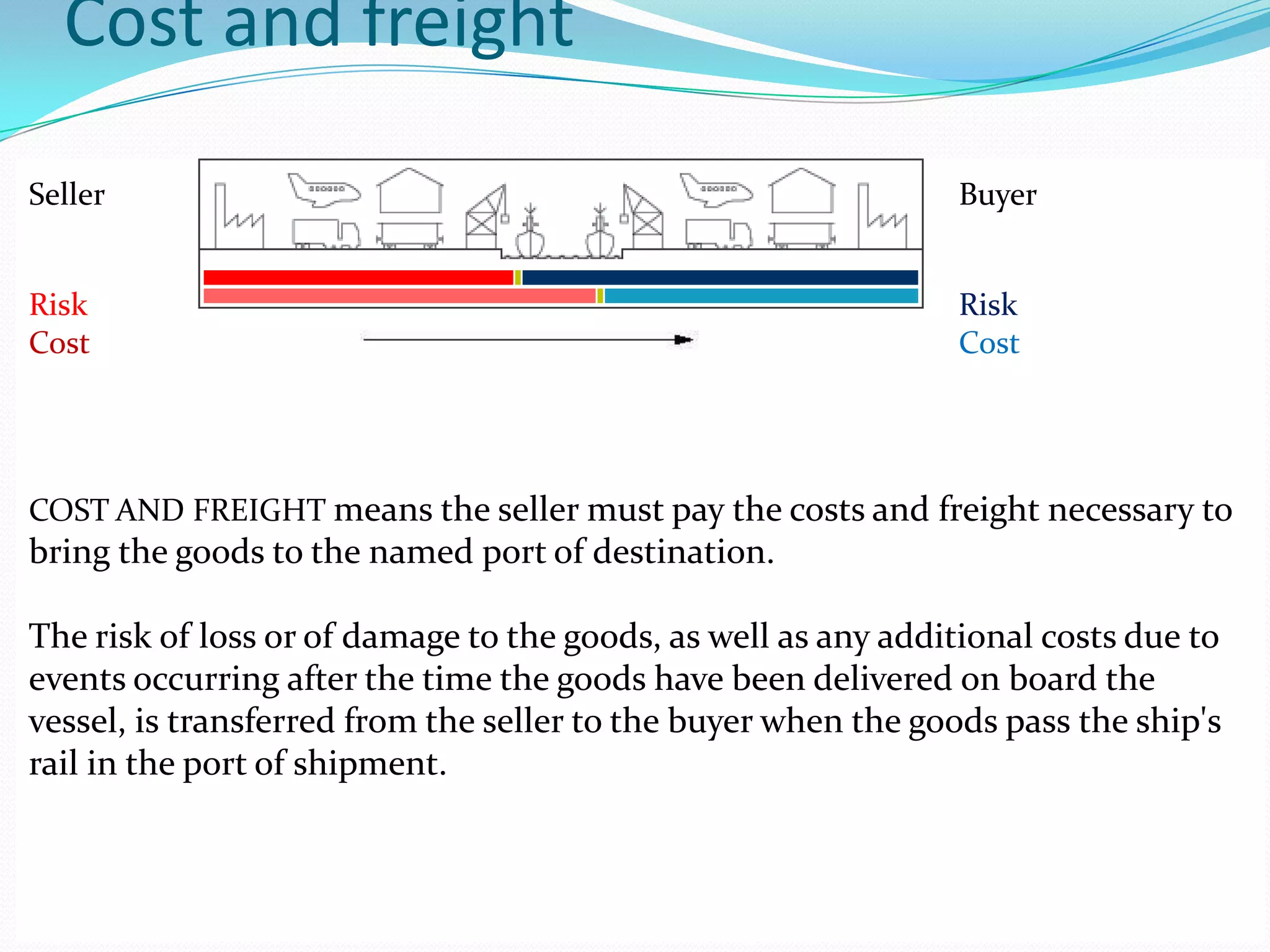

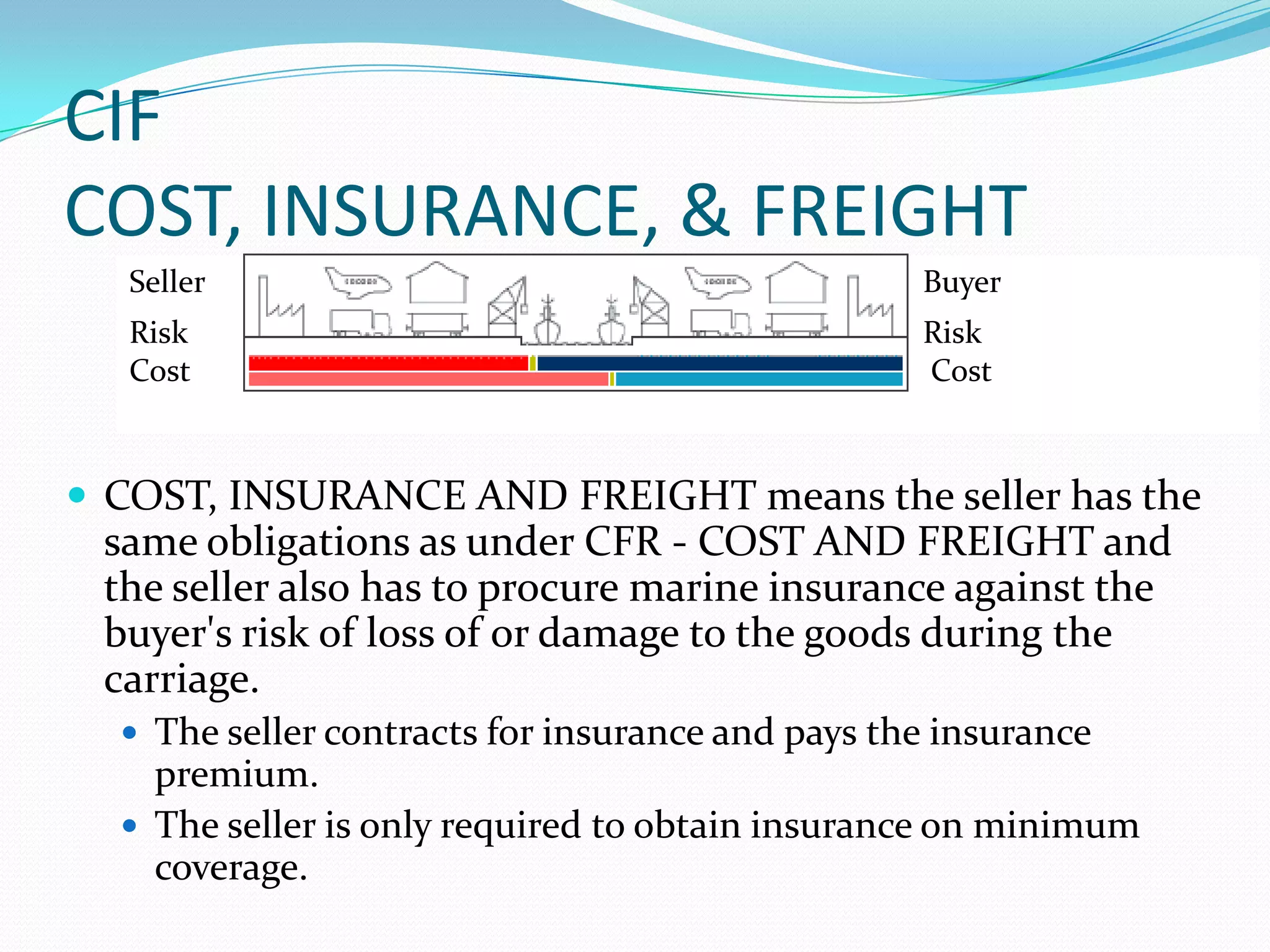

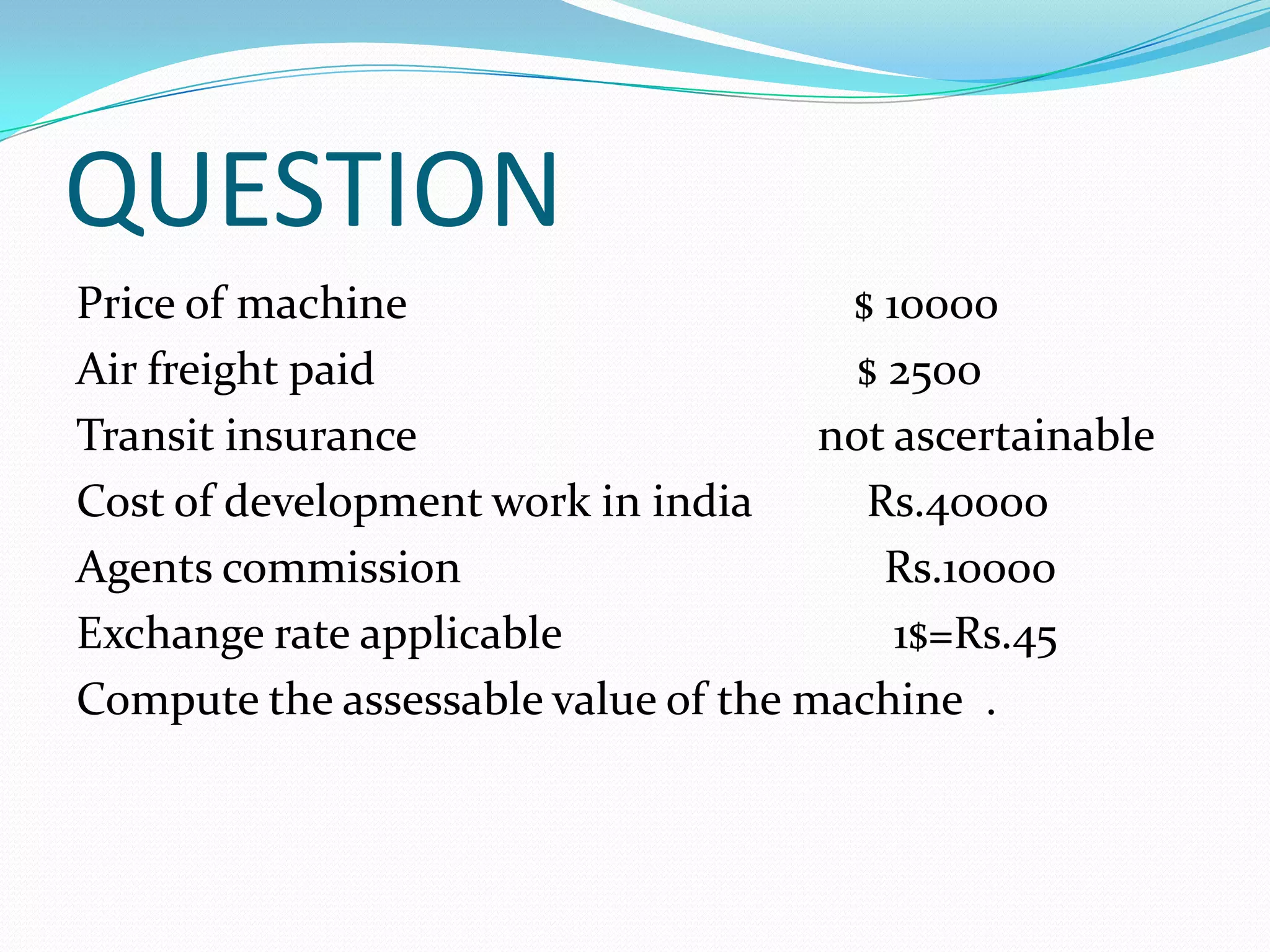

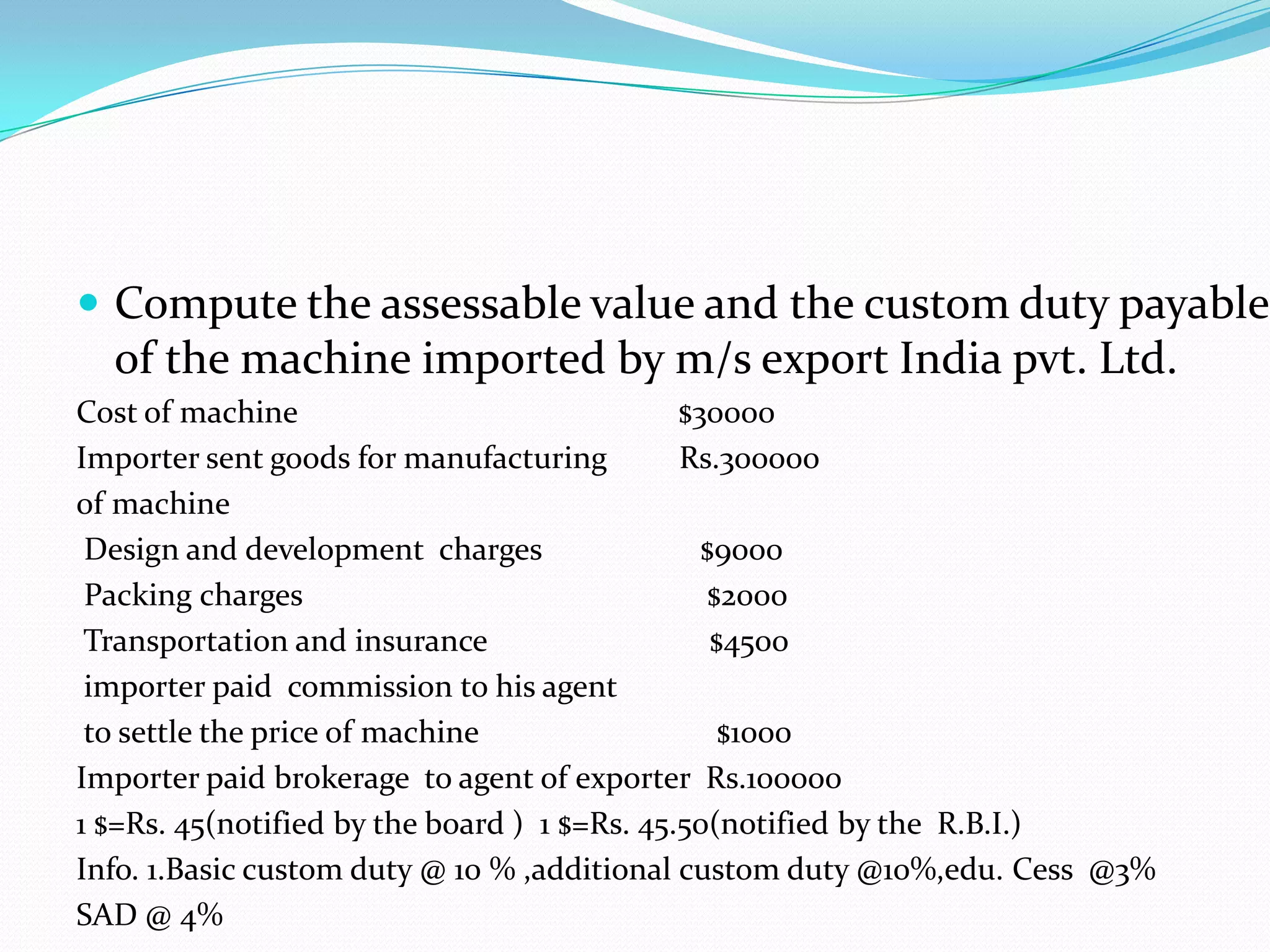

Importance of various letters of credit, obligations in shipping terms like FOB, CFR, CIF, and calculations for assessable value and customs duties.

Importance of various letters of credit, obligations in shipping terms like FOB, CFR, CIF, and calculations for assessable value and customs duties.

Importance of various letters of credit, obligations in shipping terms like FOB, CFR, CIF, and calculations for assessable value and customs duties.

Session closes with a Q&A opportunity and courtesy thanks from the presenter.

![Pre & post_shipment_finance[1]](https://cdn.slidesharecdn.com/ss_thumbnails/prepostshipmentfinance1-110906105407-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)