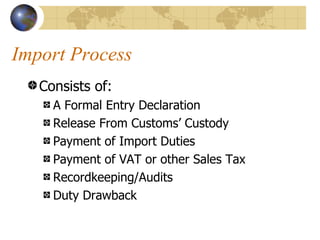

The import process consists of several key steps:

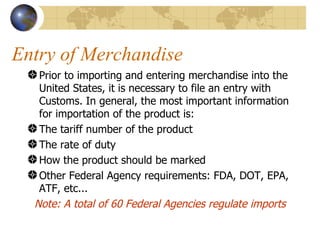

1) Filing an entry declaration with customs to import merchandise and pay any import duties or taxes. This requires providing information on the tariff classification, duty rate, and documentation of the right to import.

2) Releasing the merchandise from customs' custody by filing additional entry documents within 5 days of arrival, including commercial invoices, packing lists, and securing a bond.

3) Paying any value-added taxes (VAT) that are passed through each party in the supply chain until reaching the final consumer. Extensive recordkeeping and auditing is required for VAT.